This year will be remembered for many reasons, and optimism is one thing that’s been in short supply since the spring. We’re experiencing a global pandemic, social unrest, an economic downturn, and natural disasters, just to name a few. The challenges brought on by the health crisis have also forced many homeowners to reevaluate their space and what they need in a home going into 2021. So, experts are forecasting that next year is one in which we can be optimistic about real estate for three key reasons.

1. The Economy Is Expected to Continue Improving

Tim Duy from the University of Oregon puts it this way:

“There is nothing fundamentally ‘broken’ in the economy that needs to heal…there was no obvious financial bubble driving excessive activity in any one economic sector when the pandemic hit…With Covid-19 cases surging again, it is understandably hard to look optimistically to the other side of this winter…Don’t let the near-term challenges distract from the economic stage being set for next four years.”

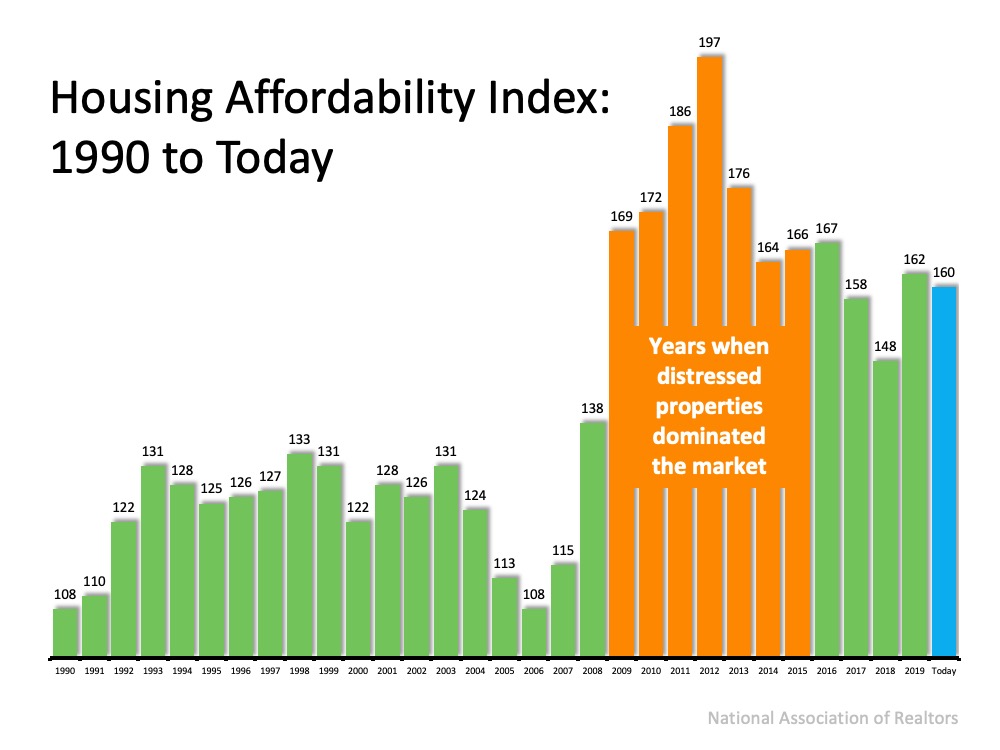

2. Interest Rates Are Projected to Stay Low

In the latest projections from Freddie Mac, interest rates for a 30-year fixed-rate mortgage are expected to remain at or near 3% next year. These low rates will continue to make homes more affordable, driving demand for housing in 2021.

3. Future Home Sales Are Forecasted to Grow

While the economy improves and interest rates remain low, homes are also expected to continue appreciating as more people buy in the coming year. Danielle Hale, Chief Economist at realtor.com, says:

“We expect home sales in 2021 to come in 7.0% above 2020 levels, following a more normal seasonal trend and building momentum through the spring and sustaining the pace in the second half of the year.”

Bottom Line

Experts forecast that buyers and sellers are going to be active in 2021. If you’ve thought about buying or selling your home this year but have held off, now may be the time to take advantage of this market. Let’s connect to take the first step toward your new home today.