There are two crises in this country right now: a health crisis that has forced everyone into their homes and a financial crisis caused by our inability to move around as we normally would. Over 20 million people in the U.S. became instantly unemployed when it was determined that the only way to defeat this horrific virus was to shut down businesses across the nation. One second a person was gainfully employed, a switch was turned, and then the room went dark on their livelihood.

The financial pain so many families are facing right now is deep.

How deep will the pain cut?

Major institutions are forecasting unemployment rates last seen during the Great Depression. Here are a few projections:

Goldman Sachs – 15%

Merrill Lynch – 10.6%

Wells Fargo – 7.3%

How long will the pain last?

As horrific as those numbers are, there is some good news. The pain will be deep, but it won’t last as long as it did after previous crises. Taking the direst projection from Goldman Sachs, we can see that 15% unemployment quickly drops to 6-8% as we head into next year, continues to drop, and then returns to about 4% in 2023.

When we compare that to the length of time it took to get back to work during both the Great Recession (9 years long) and the Great Depression (12 years long), we can see how the current timetable is much more favorable.

Bottom Line

It’s devastating to think about how the financial heartache families are going through right now is adding to the uncertainty surrounding their health as well. Hopefully, we will soon have the virus contained and then we will, slowly and safely, return to work.

The uncertainty the world faces today due to the COVID-19 pandemic is causing so many things to change. The way we interact, the way we do business, even the way we buy and sell real estate is changing. This is a moment in time that’s even sparking some buyers to search for a better deal on a home. Sellers, however, aren’t offering a discount these days; they’re holding steady on price.

According to the most recent NAR Flash Survey (a survey of real estate agents from across the country), agents were asked the following two questions:

1. “Have any of your sellers recently reduced their price to attract buyers?”

Their answer: 72% said their sellers have not lowered prices to attract buyers during this health crisis.

2. “Are home buyers expecting lower prices now?”

Their answer: 63% of agents said their buyers were looking for a price reduction of at least 5%.

What We Do Know

In today’s market, with everything changing and ongoing questions around when the economy will bounce back, it’s interesting to note that some buyers see this time as an opportunity to win big in the housing market. On the other hand, sellers are much more confident that they will not need to reduce their prices in order to sell their homes. Clearly, there are two different perspectives at play.

Bottom Line

If you’re a buyer in today’s market, you might not see many sellers lowering their prices. If you’re a seller and don’t want to lower your price, you’re not alone. If you have questions on how to price your home, let’s connect today to discuss your real estate needs and next steps.

With all of the unanswered questions caused by COVID-19 and the economic slowdown we’re experiencing across the country today, many are asking if the housing market is in trouble. For those who remember 2008, it’s logical to ask that question.

Many of us experienced financial hardships, lost homes, and were out of work during the Great Recession – the recession that started with a housing and mortgage crisis. Today, we face a very different challenge: an external health crisis that has caused a pause in much of the economy and a major shutdown of many parts of the country.

Let’s look at five things we know about today’s housing market that were different in 2008.

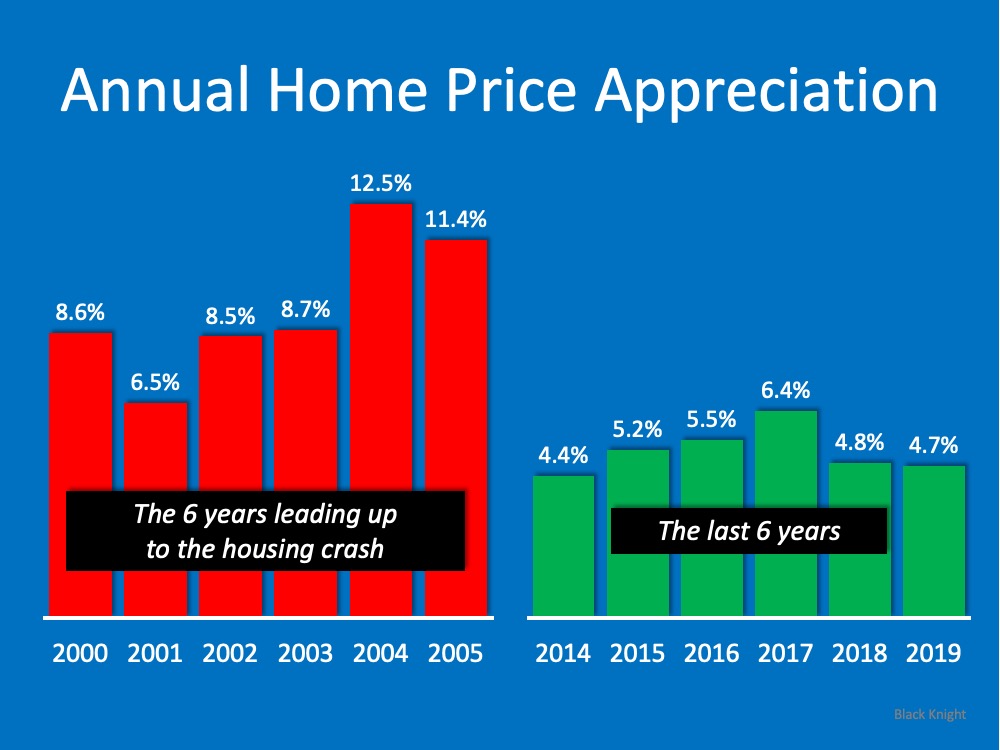

1. Appreciation

When we look at appreciation in the visual below, there’s a big difference between the 6 years prior to the housing crash and the most recent 6-year period of time. Leading up to the crash, we had much higher appreciation in this country than we see today. In fact, the highest level of appreciation most recently is below the lowest level we saw leading up to the crash. Prices have been rising lately, but not at the rate they were climbing back when we had runaway appreciation.

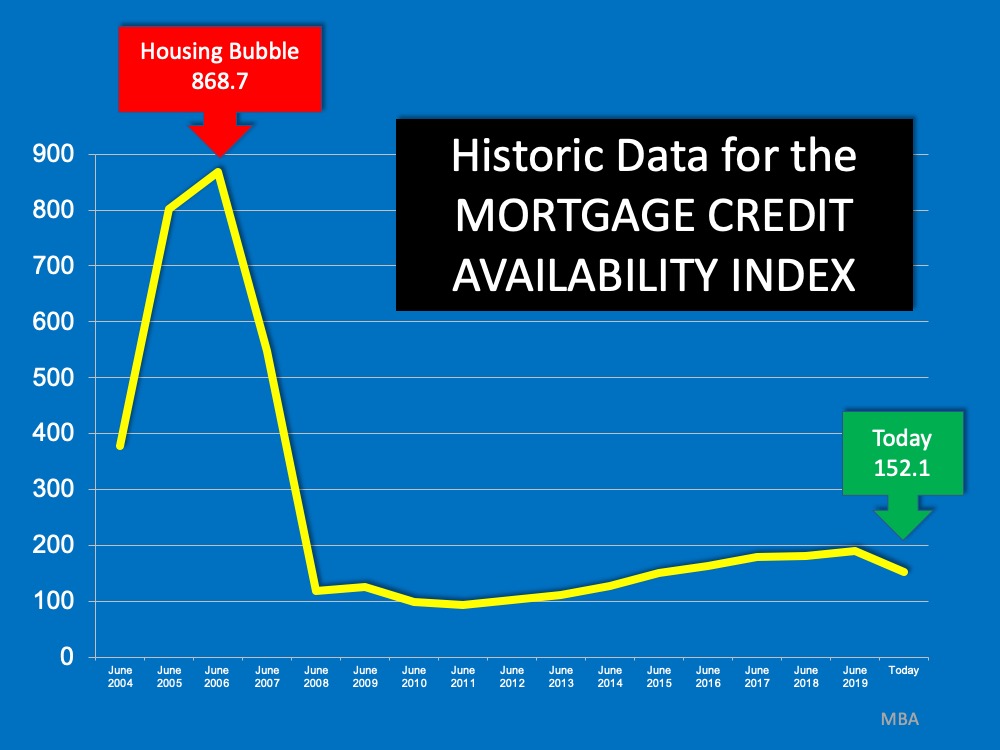

2. Mortgage Credit

The Mortgage Credit Availability Index is a monthly measure by the Mortgage Bankers Association that gauges the level of difficulty to secure a loan. The higher the index, the easier it is to get a loan; the lower the index, the harder. Today we’re nowhere near the levels seen before the housing crash when it was very easy to get approved for a mortgage. After the crash, however, lending standards tightened and have remained that way leading up to today.

3. Number of Homes for Sale

One of the causes of the housing crash in 2008 was an oversupply of homes for sale. Today, as shown in the next image, we see a much different picture. We don’t have enough homes on the market for the number of people who want to buy them. Across the country, we have less than 6 months of inventory, an undersupply of homes available for interested buyers.

4. Use of Home Equity

The chart below shows the difference in how people are accessing the equity in their homes today as compared to 2008. In 2008, consumers were harvesting equity from their homes (through cash-out refinances) and using it to finance their lifestyles. Today, consumers are treating the equity in their homes much more cautiously.

5. Home Equity Today

Today, 53.8% of homes across the country have at least 50% equity. In 2008, homeowners walked away when they owed more than what their homes were worth. With the equity homeowners have now, they’re much less likely to walk away from their homes.

Bottom Line

The COVID-19 crisis is causing different challenges across the country than the ones we faced in 2008. Back then, we had a housing crisis; today, we face a health crisis. What we know now is that housing is in a much stronger position today than it was in 2008. It is no longer the center of the economic slowdown. Rather, it could be just what helps pull us out of the downturn.

Every day that passes, people have a need to buy and sell homes. That doesn’t stop during the current pandemic. If you’ve had a major life change recently, whether with your job or your family situation, you may be in a position where you need to sell your home – and fast. While you probably feel like timing with the current pandemic isn’t on your side, making a move is still possible. Rest assured, with technology at your side and fewer sellers on the market in most areas, you can list your house and make it happen safely and effectively, especially when following the current COVID-19 guidelines set forth by the National Association of Realtors (NAR) and the Centers for Disease Control and Prevention (CDC).

You may have a new baby, a new employment situation, a parent who moved in with you, you just built a home that’s finally ready to move into, or some other major part of your life that has changed in recent weeks. Buyers have those needs too, so rest assured that someone is likely looking for a home just like yours.

According to the NAR Flash Survey: Economic Pulse taken April 5 – 6, real estate agents indicate, not surprisingly, that there’s a noticeable decline in current homebuyer interest. That said, 10% of agents said in the same survey that they saw no change or even an increase in buyer activity. So, while buyer interest is low compared to normal spring markets, there are still buyers in the market. Don’t forget, you only need one buyer – the right one for your home.

Here’s the other thing – people are spending a lot of time on the Internet right now, given the stay-at-home orders implemented across the country. Buyers are actively looking at homes for sale online. Some of them are reaching out to real estate professionals for virtual tours and getting ready to make offers too. Homes are being sold in many markets.

There Is Less Competition Right Now

The same survey indicates that 56% of NAR members said sellers are removing their homes from the market right now. This can definitely work in your favor. If other sellers are removing their listings, your home has a better chance of rising to the top of a buyer’s search list and being seen. Keep in mind, listings will pick up again soon, as 57% of the respondents note that sellers are only planning to delay the process by a couple of months. If you need to sell right now, don’t wait for the competition to get back into the market again.

This year, delayed listings from the typically busy spring season will push into the summer months, so more competition will be coming to the market as the pandemic passes. Getting ahead of that wave now might be your biggest opportunity.

Your Trusted Real Estate Advisor Can Help

Real estate agents are working hard every single day under untraditional circumstances, utilizing technology to help both buyers and sellers who need to continue with their plans. We’re using virtual tours to show homes currently on the market, staying connected with the buyers and sellers through video chats, and leveraging resources to complete transactions electronically. We’re making sure the families we support remain safe and can keep their real estate needs on track, especially as life is changing so rapidly.

Bottom Line

Homes are still being bought and sold in the midst of this pandemic. If you need to sell your house and would like to know the current status in our local market, let’s work together to create a safe and effective plan that works for you and your family.

With over 90% of Americans now under a shelter-in-place order, many experts are warning that the American economy is heading toward a recession, if it’s not in one already. What does that mean to the residential real estate market?

“A recession is a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales.”

COVID-19 hit the pause button on the American economy in the middle of March. Goldman Sachs, JP Morgan, and Morgan Stanley are all calling for a deep dive in the economy in the second quarter of this year. Though we may not yet be in a recession by the technical definition of the word today, most believe history will show we were in one from April to June.

Does that mean we’re headed for another housing crash?

Many fear a recession will mean a repeat of the housing crash that occurred during the Great Recession of 2006-2008. The past, however, shows us that most recessions do not adversely impact home values. Doug Brien, CEO of Mynd Property Management,explains:

“With the exception of two recessions, the Great Recession from 2007-2009, & the Gulf War recession from 1990-1991, no other recessions have impacted the U.S. housing market, according to Freddie Mac Home Price Index data collected from 1975 to 2018.”

CoreLogic, in a second study of the last five recessions, found the same. Here’s a graph of their findings:

What are the experts saying this time?

This is what three economic leaders are saying about the housing connection to this recession:

“The housing sector enters this recession underbuilt rather than overbuilt…That means as the economy rebounds – which it will at some stage – housing is set to help lead the way out.”

“Last time housing led the recession…This time it’s poised to bring us out. This is the Great Recession for leisure, hospitality, trade and transportation in that this recession will feel as bad as the Great Recession did to housing.”

John Burns, founder of John Burns Consulting, also revealed that his firm’s research concluded that recessions caused by a pandemic usually do not significantly impact home values:

“Historical analysis showed us that pandemics are usually V-shaped (sharp recessions that recover quickly enough to provide little damage to home prices).”

Bottom Line

If we’re not in a recession yet, we’re about to be in one. This time, however, housing will be the sector that leads the economic recovery.

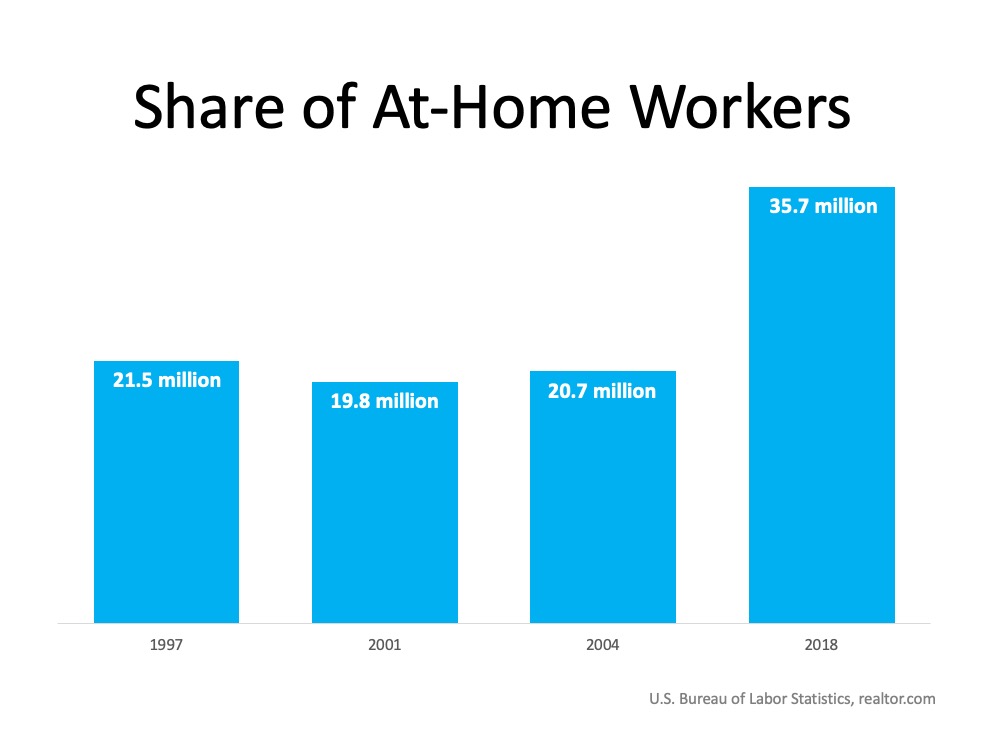

For years, we’ve all heard about the most desirable home features buyers are looking for, from upgraded kitchens to remodeled bathrooms, master suites, and more. The latest on the hotlist, however, might surprise you: home offices.

In a recent article by George Ratiu, Senior Economist with realtor.com, he notes how listings with an office are selling quickly:

“As more companies have been embracing remote work, buyers are driving demand for houses with home offices higher. Homes featuring the term ‘office’ are selling 9 days faster than the overall housing inventory.”

Today, more and more people are working remotely, and that’s not just because the current pandemic is prompting businesses to operate virtually. According to the same piece and the most recent data available, the number of employees working at home was fairly steady from 1997 – 2004 but has been climbing ever since (see graph below):Clearly, the work-from-home population is growing, and technology is making it possible. Just last month, according to an article on Think Google, searches for telecommuting hit an all-time high, and that’s certainly no surprise given our current situation.

People all over the U.S. are looking for answers on how to be most effective at home, and it’s making the ideal workspace more and more desirable. In fact, best practices from seasoned work-from-home professionals, like Chris Anderson, Senior Account Executive at HousingWire, tout that having a dedicated space is a must for productivity.

With today’s increasing demand for home offices, it’s a great feature to highlight within your listing if you’re selling a house that may meet this growing need. From bright natural light with large windows to built-in bookshelves or a quiet and secluded atmosphere, whatever makes your office space shine is worth mentioning to buyers when you’re ready to list your house.

Ratiu concludes:

“For housing, the continued increase in the share of remote workers implies that demand for homes with offices or dedicated work spaces will continue to increase. The current coronavirus pandemic offers a dramatic indication of the fact that companies and employees will have to develop plans and clearer policies for remote work beyond the current crisis.”

Bottom Line

Remote work may become more widely accepted as this current crisis teaches businesses throughout the country what it takes to function virtually. So, what seems like a business challenge today may be more of the norm tomorrow. With that in mind, if you have a home office, your house may be more desirable to buyers than you think.

Today’s everyday reality is pretty different than it looked just a few weeks ago. We’re learning how to do a lot of things in new ways, from how we work remotely to how we engage with our friends and neighbors. Almost everything right now is shifting to a virtual format. One of the big changes we’re adapting to is the revisions to the common real estate transaction, which all vary by state and locality. Technology, however, is making it possible for many of us to continue on the quest for homeownership, an essential need for all.

Here’s a look at some of the elements of the process that are changing (at least in the near-term), due to stay-at-home orders and social distancing, and what you may need to know about each one if you’re thinking of buying or selling a home sooner rather than later.

1. Virtual Consultations – Instead of heading into an office, you can meet with real estate and lending professionals through video chat. Whether it’s your first initial needs analysis as a buyer or your listing appointment as a seller, you can still get the process started remotely and create a plan together. Your trusted advisor is still on your side.

2. Home Searches & Virtual Showings – According to theNational Association of Realtors (NAR), the Internet is one of the three most popular information sources buyers use when searching for homes. Your real estate agent can send you listing information and help you request a virtual showing when you’re ready to start looking. This means you can virtually walk through the homes on your wish list while keeping your family safe. As a seller, you can still have virtual open houses and virtual tours too, so as not to miss those buyers looking to find a home right now.

3. Document Signing – Although this is another area that varies by state, today more portions of the transaction are being done digitally. In many areas, your agent or loan officer can set up an account where you can upload all of the required documents and sign electronically right from your computer.

4. Sending Money – Whether you need to pay for an appraisal or submit closing costs, there are options available. Depending on the transaction and local regulations, you may be able to pay by credit card, and most banks will also allow you to wire funds from your account. Sometimes you can send a check by mail, and in some states, a mobile escrow agent will pick up a check from your home.

5. Closing Process – Again, depending on your area, a mobile notary may be able to bring the required documents to your home before the closing. If your state requires an attorney to be present, check with your legal counsel to see what options are available. Also, depending on the title company, some are allowing drive-thru closings, which is similar to doing a transaction at a bank window.

Although these virtual processes are starting to become more widely accepted, it does not mean that this is the way things are going to get done from now on. Under the current circumstances, however, technology is making it possible to continue much of the real estate transaction today.

Bottom Line

If you need to move today, technology can help make it happen; there are options available. Let’s touch base today to discuss your situation and our local regulations, so you don’t have to put your real estate plans on hold.

There’s a ton of real estate information available in the news today and on the Internet. It can be extremely confusing, especially in times of uncertainty like we’re facing right now.

If you’re thinking of buying or selling this year, you need an agent who can help you:

Make sense of this rapidly evolving housing market

Navigate everything from virtual showings to new online marketing strategies

Price your home correctly at the beginning of the selling process

Determine what to offer on your dream home without paying too much or offending the seller

Dave Ramsey, a financial guru, advises:

“When getting help with money, whether it’s insurance, real estate or investments, you should always look for someone with the heart of a teacher, not the heart of a salesman.”

Hiring an agent who has a finger on the pulse of the current market will make your buying or selling experience so much easier.

So, how do you identify who truly understands what’s happening right now? How do you know who will take the time to simply and effectively explain what today’s market conditions mean to you and your family?

Check out the agent on social media. What are they posting on Instagram, Facebook, Twitter, and more? Are they using their social media platforms to share relevant, helpful information, or are they just posting memes and recipes? The best agents are committed to educating the consumer so they can feel confident when buying or selling a home.

Bottom Line

What agents are posting online will help you determine who meets the criteria Dave Ramsey suggested you look for: someone withthe heart of a teacher. Let’s connect today, so you can work with a true trusted real estate professional.

Ten million Americans lost their jobs over the last two weeks. The next announced unemployment rate on May 8th is expected to be in the double digits. Because the health crisis brought the economy to a screeching halt, many are feeling a personal financial crisis. James Bullard, President of the Federal Reserve Bank of St. Louis, explained that the government is trying to find ways to assist those who have lost their jobs and the companies which were forced to close (think: your neighborhood restaurant). In a recent interview he said:

“This is a planned, organized partial shutdown of the U.S. economy in the second quarter. The overall goal is to keep everyone, households and businesses, whole.”

That’s promising, but we’re still uncertain as to when the recently unemployed will be able to return to work.

Another concern: how badly will the U.S. economy be damaged if people can’t buy homes?

A new concern is whether the high number of unemployed Americans will cause the residential real estate market to crash, putting a greater strain on the economy and leading to even more job losses. The housing industry is a major piece of the overall economy in this country.

Chris Herbert, Managing Director of the Joint Center for Housing Studies of Harvard University, in a post titled Responding to the Covid-19 Pandemic, addressed the toll this crisis will have on our nation, explaining:

“Housing is a foundational element of every person’s well-being. And with nearly a fifth of US gross domestic product rooted in housing-related expenditures, it is also critical to the well-being of our broader economy.”

How has the unemployment rate affected home sales in the past?

It’s logical to think there would be a direct correlation between the unemployment rate and home sales: as the unemployment rate went up, home sales would go down, and when the unemployment rate went down, home sales would go up.

However, research reviewing the last thirty years doesn’t show that direct relationship, as noted in the graph below. The blue and grey bars represent home sales, while the yellow line is the unemployment rate. Take a look at numbers 1 through 4:

The unemployment rate was rising between 1992-1993, yet home sales increased.

The unemployment rate was rising between 2001-2003, and home sales increased.

The unemployment rate was rising between 2007-2010, and home sales significantly decreased.

The unemployment rate was falling continuously between 2015-2019, and home sales remained relatively flat.

The impact of the unemployment rate on home sales doesn’t seem to be as strong as we may have thought.

Isn’t this time different?

Yes. There is no doubt the country hasn’t seen job losses this quickly in almost one hundred years. How bad could it get? Goldman Sachs projects the unemployment rate to be 15% in the third quarter of 2020, flattening to single digits by the fourth quarter of this year, and then just over 6% percent by the fourth quarter of 2021. Not ideal for the housing industry, but manageable.

How does this compare to the other financial crises?

Some believe this is going to be reminiscent of The Great Depression. From the standpoint of unemployment rates alone (the only thing this article addresses), it does not compare. Here are the unemployment rates during the Great Depression, the Great Recession, and the projected rates moving forward:

Bottom Line

We’ve given you the facts as we know them. The housing market will have challenges this year. However, with the help being given to those who have lost their jobs and the fact that we’re looking at a quick recovery for the economy after we address the health problem, the housing industry should be fine in the long term. Stay safe.

As our lives, our businesses, and the world we live in change day by day, we’re all left wondering how long this will last. How long will we feel the effects of the coronavirus? How deep will the impact go? The human toll may forever change families, but the economic impact will rebound with a cycle of downturn followed by economic expansion like we’ve seen play out in the U.S. economy many times over.

Here’s a look at what leading experts and current research indicate about the economic impact we’ll likely see as a result of the coronavirus. It starts with a forecast of U.S. Gross Domestic Product (GDP).

“Gross Domestic Product (GDP) is the total monetary or market value of all the finished goods and services produced within a country’s borders in a specific time period. As a broad measure of overall domestic production, it functions as a comprehensive scorecard of the country’s economic health.”

When looking at GDP (the measure of our country’s economic health), a survey of three leading financial institutions shows a projected sharp decline followed by a steep rebound in the second half of this year:A recent study from John Burns Consulting also notes that past pandemics have also created V-Shaped Economic Recoveries like the ones noted above, and they had minimal impact on housing prices. This certainly gives hope and optimism for what is to come as the crisis passes.

With this historical analysis in mind, many business owners are also optimistic for a bright economic return. A recent PricewaterhouseCoopers survey shows this confidence, noting 66% of surveyed business owners feel their companies will return to normal business rhythms within a month of the pandemic passing, and 90% feel they should be back to normal operation 1 to 3 months after:From expert financial institutions to business leaders across the country, we can clearly see that the anticipation of a quick return to normal once the current crisis subsides is not too far away. In essence, this won’t last forever, and we will get back to growth-mode. We’ve got this.

Bottom Line

Lives and businesses are being impacted by the coronavirus, but experts do see a light at the end of the tunnel. As the economy slows down due to the health crisis, we can take guidance and advice from experts that this too will pass.

My name is John Bendele and these are words to live by.

“What is the biggest challenge you are facing in life right now and how can I help?”

I believe when you are able to help others in their struggles, it will always bring a since of joy and accomplishment that is like no other. I enjoy bringing opportunities to people in real estate and in life. To be a lifting hand and a beacon of knowledge. It brings me great joy to guide and support others when making exciting and difficult choices. I have been a licensed realtor for over 7 years in Minnesota. Coming from a construction background, I will provide a wealth of knowledge about homes. Knowing homes allows me to a better negotiator with facts and details some may not. I enjoy working with sellers, investors and buyers.

I grew up in Southwest Texas and moved to Minnesota in 2015. I have lived in the White Bear Lake area until making a move over the lake to Willernie, MN where I now reside. I love spending quality time with my teenage boys who nicknamed me “JoJo”. My favorite things to do are being outdoors on or in the water, BBQing (TX style) and going on any adventure.

I want to bring knowledge, growth, excitement and wealth to the clients I encounter through being a realtor. I look forward to assisting you in your amazing journey in real estate.

Thank you,

John A Bendele

Meet Brittany

Brittany is a mama of three kiddos, a wife of a firefighter and added more love to her home with three dogs and two cats. Outside of the fun she has as an agent and her roles at home she enjoys doing any DIY projects she can get her hands on!

Brittany fell in love with the Real Estate gig in 2019. She grew up in Apple Valley, and now owns her childhood home. I guess you could say she is a south metro pro!

You!

Hey! If you’re looking for your next role as an agent let us know! This could be you!

Meet Shea Amundson

Hey, I’m Shea and I love helping people find a beautiful home that sets their soul on fire!

Meet Katie

Katie comes from the busy world of entertainment and being a Traveling Operations Manager. She transitioned to Real Estate back in 2018 and has been hooked ever since! Katie thrives on training, developing new systems, and helping agents grow! Katie joins Voila with the determination to help every agent and client make their dream a reality whether it be building their business or finding that dream home!

When Katie isn’t working, she is a full-time student at Metropolitan University. She enjoys cooking foods from all over the world, traveling, and has a habit of getting a new tattoo wherever she goes. She is huge into animal conservation and spending time with her dog Sawyer who often joins her on travels!

Meet Sarah Beth Lindstrom

Sarah wants to live in a world filled with innovative businesses daring enough to break the mold…monthly auto-shipments of Laffy Taffy’s, and lots and lots of laughter!!!

Having been in the real estate industry since 2005, her go to role has always been supporting her teams in any way that she can! She has gone from Listing and Transaction Management, to Team Manager, and now Director of Support! She is an ‘introverted extrovert’ that finds the, ‘behind the scenes’ with a hint of showing homes – to be a perfect blend.

When she’s not supporting her Voila Family, she is out getting one more rep in at the gym, finding new healthy recipes to attempt (and then trick her teenager into eating somehow), and enjoying quick road trips to…well, anywhere! She also plays on a competitive volleyball team in the winter, sand volleyball in the summer and softball in the spring and fall.

“Two things define you. The patience you have when you have nothing and the attitude when you have everything.”

Meet Jessi Andersen

In June of 2020 Jessi joined team of Voila…and…it’s that easy!

Ha! No really, it did all begin in June. New to this side of Real Estate, Jessi joined in hopes to take her chatty, outgoing self and bring some good of it! Her natural tendencies of networking and love of growth and goals, have been set in direction – expanding Voila!

Where is Jess when she isn’t nurturing the growth of Voila? Adventuring with her family outside in nature. Or perhaps baking up a new recipe while dancing the day away – and of course cheering for her little athletes at home, as well as the MN Vikings/Twins!

“In the end it is not the years in your life that count. It’s the life in your years” ~ Abe Lincoln

Meet Wyatt Lemon

Wyatt is a Real Estate Extraordinaire, and a Loving Husband, and a Lover of Life and a PAW-rent to 3 awesome dogs. Huge believer in the idea that life is what you make of it, so with that being said I guess you could say the glass is half full! Things I enjoy outside of work are Yoga, being a big time Foodie, and spending time with my family. I grew up in Hugo MN and have been a local resident my whole life. I studied Marketing at Century College as well as St. Cloud State University. I got into Real Estate in October of 2018 and have loved every minute of it!

Meet James Andersen

James Andersen is a human being who believes that the best in others is a reflection of the energy we bring.

Magnanimous behavior is the standard not the exception.

10+ years Army Career

5+ years Married

5+ years Father of Calendar Crushers

5+ years Real Estate Career

30+ years Life Experience

Let’s learn and grow together.

Meet Joey Torkildson

You are writing your own story in life! Is what you are doing right now supposed to be in that story? I hope so!

That’s why my goal is to always sign up, get uncomfortable, inspire through doing, shoot, then aim. We don’t have enough time on this planet to stay mundane and there are too many experiences to be doing one thing for too long! It’s all about the short term experiments!

Quick background: 19+ year US Army Master Sergeant vet; 10+ year transformer of lives through ownership (AKA: Realtor) ; 2+ year CEO of an Expansion Team with Hergenrother Realty Group ; Director of Agent Training with that same organization; Self employed for 12+ years; starting in late 2019 CoFounded a new disruptive real estate brokerage, Voila; Contagiously energetic teacher who loves helping people discover they can accomplish anything; Dad of two extremely crazy and loving boys; Husband of an amazingly supportive and ultimate gardener wife.

Let’s be curious explorers together! I love connecting with people and helping them achieve their goals and I’m a firm believer in the fact that you are one introduction away from your entire life changing!

Two quotes I live by: Amazing things rarely happen in your comfort zone and only those who attempt the absurd achieve the impossible!