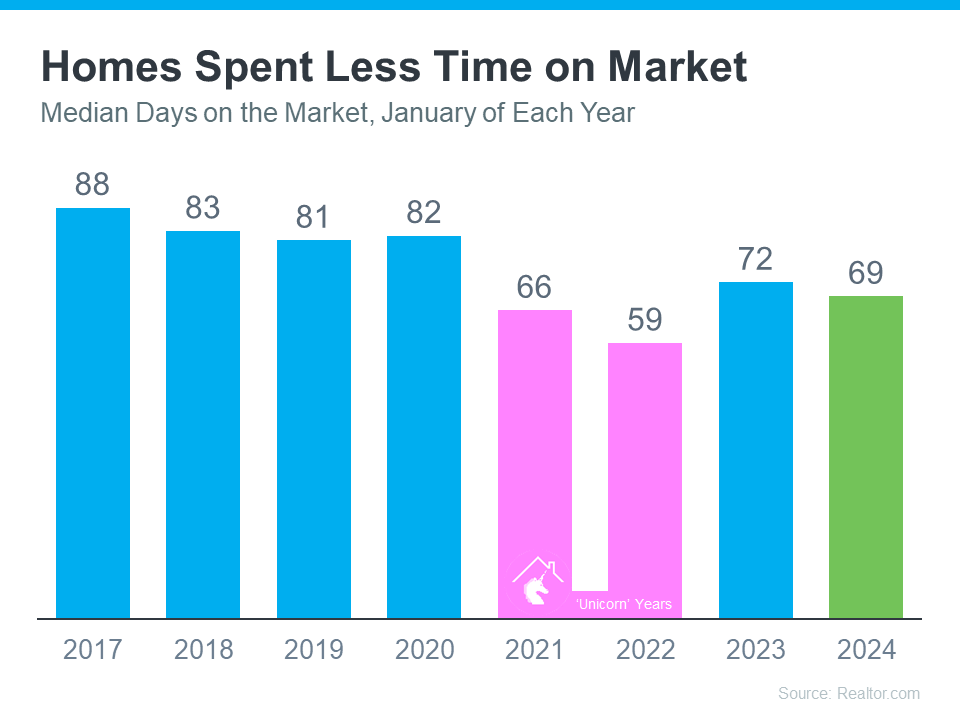

If you’re thinking of selling your house this spring, now is the perfect time to start getting it ready. With the market gearing up for its busiest time of year, it’ll be important to make sure your house shines bright among the competition.

Here are some valuable tips you can use to get your house market-ready.

Declutter and Organize

First impressions matter, and if your house is a mess, that can easily turn off potential buyers. Before listing, take the time to declutter and organize each room. Decluttering is about more than just tidying up – it’s about creating a sense of space and openness that allows potential buyers to envision themselves living in your home. According to Moving.com:

“Decluttering and organizing your space will go a long way in appealing to potential buyers. . . .decluttering will help the buyers see themselves living in your home. Less clutter inside a home also helps a place appear larger and cleaner, which should attract more buyers.”

Deep Clean Your Kitchen and Bathrooms

The kitchen and bathrooms are focal points for many buyers, and often influence their overall opinion of the house. Ensure these spaces dazzle by giving them a thorough deep cleaning. Pay attention to details like scrubbing grout lines, polishing fixtures, and decluttering countertops. A sparkling kitchen and bathroom can leave a lasting positive impression on potential buyers.

Maintain Your Yard

Your home’s exterior is the first thing potential buyers see, so it’s important to make a good impression from the moment they arrive. A well-maintained yard not only enhances curb appeal, but also shows buyers the home has been well taken care of.

Take the time to spruce up your yard by mowing the lawn, trimming bushes, and clearing away any debris or dead plants. Remember, the goal is to create a welcoming environment that entices buyers to step inside and imagine themselves living there. U.S. News says:

“A beautifully landscaped front yard can elevate an ordinary house into a charming home and will help homes sell faster and for more money.”

Find a Listing Agent

A skilled listing agent is your partner in minimizing stress when selling your home. Lean on your agent for advice on decluttering, staging, and enhancing your home’s appeal to potential buyers. Their insights into market trends and recommendations for reliable contractors and stagers are invaluable. As Realtor.com says:

“A good listing agent will help you price your home . . . recommend a photographer and stager to make it look its best, and put your home on the multiple listing service.”

Bottom Line

By decluttering, deep cleaning, and tidying up your house, you can create a welcoming environment that resonates with buyers and increases your chances of a successful sale. Connect with a trusted real estate agent for advice on what you need to do to get your house ready to sell this spring.