One of the biggest hurdles buyers have faced over the past few years has been a lack of homes available for sale.

Auto Added by WPeMatico

One of the biggest hurdles buyers have faced over the past few years has been a lack of homes available for sale.

In today’s housing market, more and more single women are becoming homeowners.

Before making the decision to buy a home, it’s important to plan for all the costs you’ll be responsible for.

Going into 2023, there was a lot of talk about a possible recession that would cause the housing market to crash.

If you’ve been thinking about buying a home, mortgage rates are probably top of mind for you.

If you’re trying to buy a home and are having a hard time finding one you can afford, it may be time to consider a fixer-upper.

No matter how you slice it, buying or selling a home is a big decision. And when you’re going through any change in your life and you need some guidance, what do you do? You get advice from people who know what they’re talking about.

Moving is no exception. You need insights from the pros to help you feel confident in your decision. Freddie Mac explains it like this:

“As you set out to find the right home for your family, be sure to select experienced, trusted professionals who will help you make informed decisions and avoid pitfalls.”

And while perfect advice isn’t possible – not even from the experts, what you can get is the very best advice out there.

For example, let’s say you need an attorney. You start off by finding an expert in the type of law required for your case. Once you do, they won’t immediately tell you how the case is going to end, or how the judge or jury will rule. But what a good attorney can do is walk you through the most effective strategies based on their experience and help you put a plan together. They’ll even use their knowledge to adjust that plan as new information becomes available.

The job of a real estate agent is similar. Just like you can’t find a lawyer to give you perfect advice, you won’t find a real estate professional who can either. That’s because it’s impossible to know everything that’s going to happen throughout your transaction. Their role is to give you the best advice they can.

To do that, an agent will draw on their experience, industry knowledge, and market data. They know the latest trends, the ins and outs of the homebuying and selling processes, and what’s worked for other people in the same situation as you.

With that expertise, a real estate advisor can anticipate what could happen next and work with you to put together a solid plan. Then, they’ll guide you through the process, helping you make decisions along the way. That’s the very definition of getting the best – not perfect – advice. And that’s the power of working with a real estate advisor.

If you’re looking to buy or sell a home, you want an expert on your side to help you each step of the way. Connect with a real estate professional so you have advice you can count on.

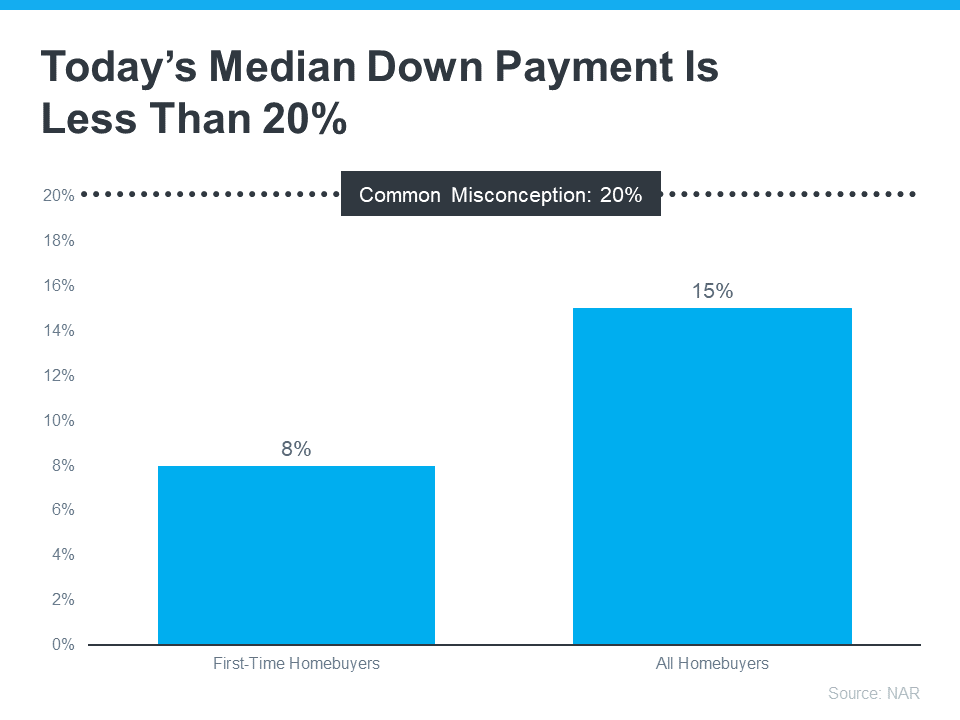

If you’re planning to buy your first home, saving up for all the costs involved can feel daunting, especially when it comes to the down payment. That might be because you’ve heard you need to save 20% of the home’s price to put down. Well, that isn’t necessarily the case.

Unless specified by your loan type or lender, it’s typically not required to put 20% down. That means you could be closer to your homebuying dream than you realize.

As The Mortgage Reports says:

“Although putting down 20% to avoid mortgage insurance is wise if affordable, it’s a myth that this is always necessary. In fact, most people opt for a much lower down payment.”

According to the National Association of Realtors (NAR), the median down payment hasn’t been over 20% since 2005. In fact, for all homebuyers today it’s only 15%. And it’s even lower for first-time homebuyers at just 8% (see graph below):

The big takeaway? You may not need to save as much as you originally thought.

According to Down Payment Resource, there are also over 2,000 homebuyer assistance programs in the U.S., and many of them are intended to help with down payments.

Plus, there are loan options that can help too. For example, FHA loans offer down payments as low as 3.5%, while VA and USDA loans have no down payment requirements for qualified applicants.

With so many resources available to help with your down payment, the best way to find what you qualify for is by consulting with your loan officer or broker. They know about local grants and loan programs that may help you out.

Don’t let the misconception that you have to have 20% saved up hold you back. If you’re ready to become a homeowner, lean on the professionals to find resources that can help you make your dreams a reality. If you put your plans on hold until you’ve saved up 20%, it may actually cost you in the long run. According to U.S. Bank:

“. . . there are plenty of reasons why it might not be possible. For some, waiting to save up 20% for a down payment may “cost” too much time. While you’re saving for your down payment and paying rent, the price of your future home may go up.”

Home prices are expected to keep appreciating over the next 5 years – meaning your future home will likely go up in price the longer you wait. If you’re able to use these resources to buy now, that future price growth will help you build equity, rather than cost you more.

Keep in mind that you don’t always need a 20% down payment to buy a home. If you’re looking to make a move this year, reach out to a trusted real estate professional to start the conversation about your homebuying goals.

Buying your first home is a big, exciting step and a major milestone that has the power to improve your life. As a first-time homebuyer, it’s a dream you can make come true, but there are some hurdles you’ll need to overcome in today’s housing market – specifically the limited supply of homes for sale and ongoing affordability challenges.

So, if you’re ready, willing, and able to buy your first home, here are three tips to help you turn your dream into a reality.

Paying the initial costs of homeownership, like your down payment and closing costs, can feel a bit daunting. But there are many assistance programs for first-time homebuyers that can help you get a loan with little or no money upfront. According to Bankrate:

“. . . you might qualify for a first-time homebuyer loan or assistance. First-time buyer loans typically have more flexible requirements, such as a lower down payment and credit score. Many help buyers with closing costs and the down payment through grants and low-interest loans.”

To find out more, talk to your state’s housing authority or check out websites like Down Payment Resource.

Right now, there aren’t enough homes for sale for everyone who wants to buy one. That’s pushing home prices up and making affordability tight for buyers. One way to deal with that issue and find a home right now is to consider condos and townhomes. Realtor.com explains:

“For many newbies, it might just be a matter of making a shift toward something they can better afford—like a condo or townhome. These lower-cost homes have historically been a stepping stone for buyers looking for a less expensive alternative to a single-family home.”

One reason why they may be more affordable is because they’re often smaller. But they still give you the chance to get your foot in the door and achieve your goal of owning a home and building equity. And that equity can help fuel your move into a larger home later on if you decide you need something bigger in the future. Hannah Jones, Senior Economic Analyst at Realtor.com, says:

“Condos can help prospective homebuyers who perhaps have a smaller budget, but who are really determined to get a foothold in the market and start to accumulate some equity. It can be a really great entry point.”

Another way to break into the market is by purchasing a home with friends or loved ones. That way you can split the cost of things like the mortgage and bills, to make it easier to afford a home. According to Money.com:

“Buying a home with another person has some obvious advantages in the mortgage department. With two incomes in the mix, buyers can likely qualify for a larger mortgage — a big help in today’s high-cost market.”

By exploring first-time homebuyer assistance, condos, townhomes, and multi-generational living, it can be easier to find and buy your first home. When you’re ready, connect with a local real estate agent.

Homeownership is a major part of the American Dream. But, the path to achieving this dream can be quite difficult. While progress has been made to improve fair housing access, households of color still face unique challenges on the road to owning a home. Working with the right real estate experts can make all the difference for diverse buyers.

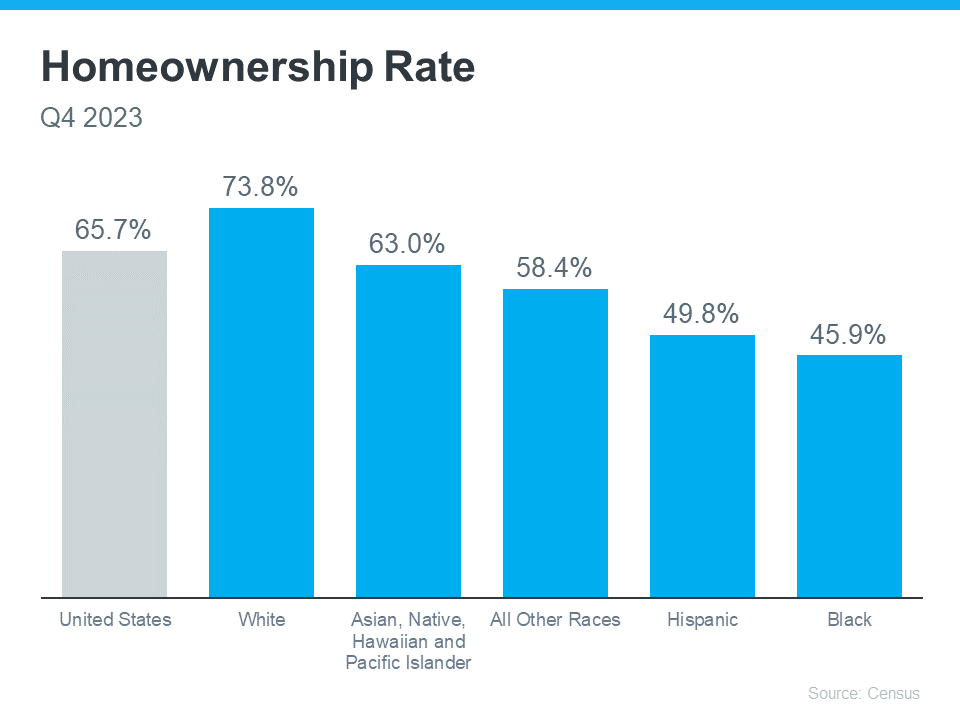

It’s clear that achieving homeownership is more challenging for certain groups because there’s still a measurable gap between the overall average U.S. homeownership rate and that of non-white groups. Today, Black households continue to have the lowest homeownership rate nationally (see graph below):

Homeownership is an important part of building household wealth that can be passed down to future generations. According to a report by the National Association of Realtors (NAR), almost half of Black homebuyers in 2023 were first-time buyers. That means many didn’t have home equity they could use toward their home purchase.

That financial hurdle alone makes buying a home more challenging, especially at a time when affordability is a major concern for first-time buyers. Jessica Lautz, Deputy Chief Economist at NAR says:

“It’s an incredibly difficult market for all home buyers right now, especially first-time home buyers and especially first-time home buyers of color.”

Because of these challenges, there are several down payment assistance programs specifically aimed at helping minority buyers fulfill their homeownership dreams:

Even if you don’t qualify for these programs, there are many other federal, state, and local options available to look into. And a real estate professional can help you find the ones that best meet your needs.

For minority homebuyers, the challenges that remain can be a point of pain and frustration. That’s why it’s so important for members of diverse groups to have the right team of experts on their sides throughout the homebuying process. These professionals aren’t only experienced advisors who understand the market and give the best advice, they’re also compassionate educators who will advocate for your best interests every step of the way.

Connect with a real estate professional to make sure you have to make sure you have the information and support you need as you walk the path to homeownership.