Around this time each year, many homeowners decide to wait until after the holidays to sell their houses. Similarly, others who already have their homes on the market remove their listings until the spring. Let’s unpack the top reasons why selling your house now, or keeping it on the market this season, is the best choice you can make. This year, buyers want to purchase homes for the holidays, and your house might be the perfect match.

Here are seven great reasons not to wait to sell your house this holiday season:

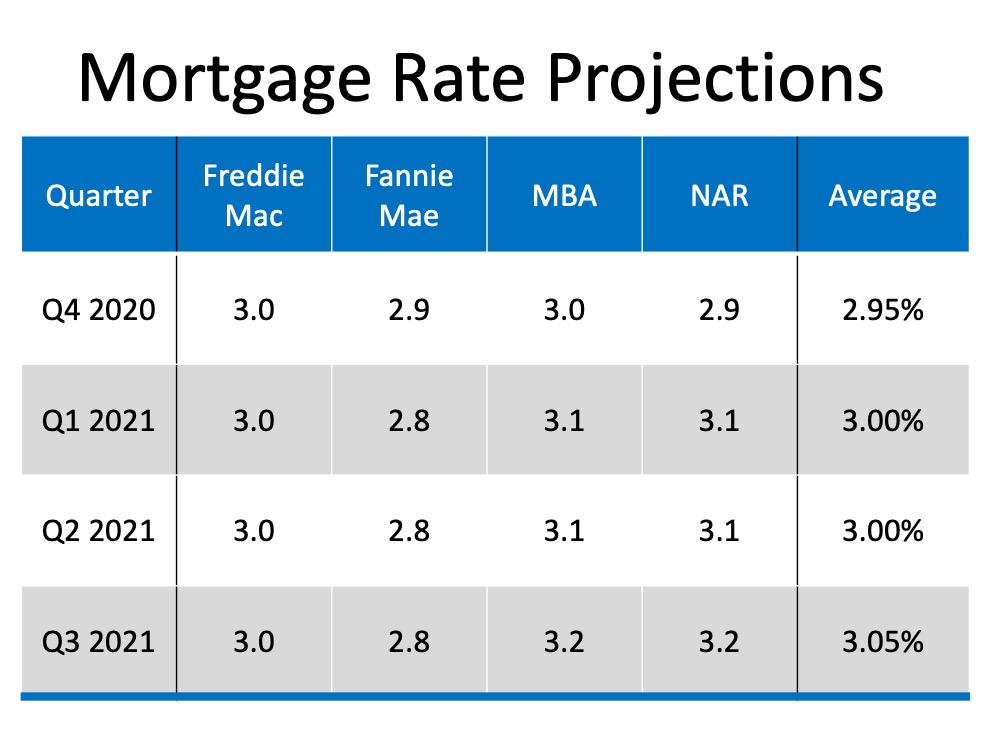

1. Buyers are active now. Mortgage rates are historically low, providing motivation for those who are ready to get more for their money over the life of their home loan.

2. Purchasers who look for homes during the holidays are serious ones, and they’re ready to buy.

3. You can restrict the showings in your house to days and times that are most convenient for you, or even select virtual options. You’ll remain in control, especially in today’s sellers’ market.

4. Homes decorated for the holidays appeal to many buyers.

5. Today, there’s minimal competition for you as a seller. There just aren’t enough houses on the market to satisfy buyer demand, meaning sellers are in the driver’s seat. Over the past year, inventory has declined to record lows, making it the opportune time to sell your house (See graph below):  6. The desire to own a home doesn’t stop during the holidays. Buyers who have been searching throughout the fall and have been running into more and more bidding wars are still on the lookout. Your home may be the answer.

6. The desire to own a home doesn’t stop during the holidays. Buyers who have been searching throughout the fall and have been running into more and more bidding wars are still on the lookout. Your home may be the answer.

7. This season is the sweet spot for sellers, and the number of listings will increase after the holidays. In many parts of the country, more new construction will also be available for sale in 2021, which will lessen the demand for your house next year.

Bottom Line

More than ever, this may be the year it makes the most sense to list your house during the holiday season. Let’s connect today to determine if selling now is your best move.

When you continually hear how rates are hitting record lows, you may be wondering: Are they going to keep falling? Should I wait until they get even lower?

When you continually hear how rates are hitting record lows, you may be wondering: Are they going to keep falling? Should I wait until they get even lower?