When buying a home, it’s important to have a budget and make sure you plan ahead for certain homebuying expenses. Saving for a down payment is the main cost that comes to mind for many, but budgeting for the closing costs required to get a mortgage is just as important.

“When you close on a home, a number of fees are due. They typically range from 2% to 5% of the total cost of the home, and can include title insurance, origination fees, underwriting fees, document preparation fees, and more.”

For example, for someone buying a $300,000 home, they could potentially have between $6,000 and $15,000 in closing fees. If you’re in the market for a home above this price range, your closing costs could be greater. As mentioned above, closing costs are typically between 2% and 5% of your purchase price.

“There will be lots of paperwork in front of you on closing day, and not enough time to read them all. Work closely with your real estate agent, lender, and attorney, if you have one, to get all the documents you need ahead of time.

The most important thing to read is the closing disclosure, which shows your loan terms, final closing costs, and any outstanding fees. You’ll get this form about three days before closing since, once you (the borrower) sign it, there’s a three-day waiting period before you can sign the mortgage loan docs. If you have any questions about the numbers or what any of the mortgage terms mean, this is the time to ask—your real estate agent is a great resource for getting you all the answers you need.”

Bottom Line

As home prices are rising and more buyers are finding themselves competing in bidding wars, it’s more important than ever to make sure your plan includes budgeting for closing costs. Let’s connect to be sure you have everything you need to land your dream home.

Many people are sitting on the fence trying to decide if now’s the time to buy a home. Some are renters who have a strong desire to become homeowners but are unsure if buying right now makes sense. Others may be homeowners who are realizing that their current home no longer fits their changing needs.

To determine if they should buy now or wait another year, they both need to ask two simple questions:

Do I think home values will be higher a year from now?

Do I think mortgage rates will be higher a year from now?

Let’s shed some light on the answers to these questions.

Where will home prices be a year from now?

If you average the most recent projections from the major industry forecasters, the expectation is home prices will increase by 7.7%. Let’s take a house that’s valued today at $325,000 as an example.

If the buyer makes a 10% down payment ($32,500), they’ll end up borrowing $292,500 for their mortgage. Applying the projected rate of home price appreciation, that same house will cost $350,025 next year. With a 10% down payment ($35,003), they’d then have to borrow $315,022.

Therefore, as a result of rising home prices alone, a prospective buyer will have to put down an additional $2,503 and borrow an additional $22,523 just for waiting a year to make their move.

Where will mortgage rates be a year from now?

Today, mortgage rates are hovering around 3%. However, most experts believe they’ll rise as the economy continues to recover. Any increase in the mortgage rate will also increase a purchaser’s cost. Here are the forecasts for the first quarter of 2022 from four major entities:

The projections average out to 3.6% among these four forecasts, a jump up from where they are today.

What does it mean to you if home values and mortgage rates increase?

A buyer will pay a lot more in mortgage payments each month if both of these variables increase. Assuming a buyer purchases a $325,000 home this year with a 30-year fixed-rate loan at 3% after making a 10% down payment, their monthly principal and interest payment would be $1,233.

That same home one year from now could be $350,025, and the mortgage rate could be 3.6% (based on the industry forecasts mentioned above). That monthly principal and interest payment, after putting down 10%, totals $1,432.

The difference in the monthly mortgage payment would be $199. That’s $2,388 more per year and $71,640 over the life of the loan.

Add to that the approximately $25,000 a house with a similar value would build in home equity this year as a result of home price appreciation, and the total net worth increase a purchaser could gain by buying this year is nearly $100,000. That’s a small fortune.

Bottom Line

When asking if they should buy a home, many potential buyers think of the nonfinancial benefits of owning a home. When asking when to buy, the financial benefits make it clear that doing so now is much more advantageous than waiting until next year.

One of the biggest hurdles homebuyers face is saving for a down payment. As you’re budgeting and planning for your home purchase, you’ll want to understand how much you’ll need to put down and how long it will take you to get there. The process may actually move faster than you think.

Using data from the U.S. Department of Housing and Urban Development (HUD) and Apartment List, we can estimate how long it might take someone earning the median income and paying the median rent to save up for a down payment on a median-priced home. Since saving for a down payment can be a great time to practice budgeting for housing costs, this estimate also uses the concept that a household should not pay more than 28% of their total income on monthly housing expenses.

According to the data, the national average for the time it would take to save for a 10% down payment is right around two and a half years (2.53). Residents in Iowa can save for a down payment the fastest, doing so in just over one year (1.31). The map below illustrates this time (in years) for each state:

What if you only need to save 3%?

What if you’re able to take advantage of one of the 3% down payment programs available? It’s a common misconception that you need a 20% down payment to buy a home, but there are actually more affordable options and down payment assistance programs available, especially for first-time buyers. The reality is, saving for a 3% down payment may not take several years. In fact, it could take less than a year in most states, as shown in the map below:

Bottom Line

Wherever you are in the process of saving for a down payment, you may be closer to your dream home than you think. Let’s connect to explore the down payment options available in our area and how they support your plans.

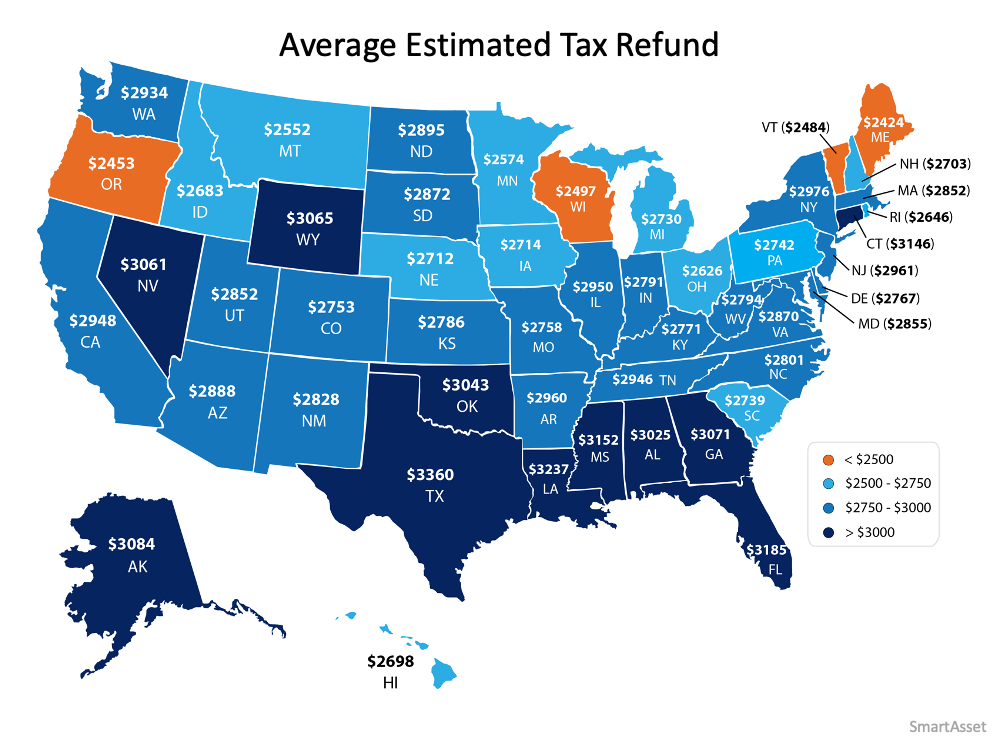

If you’re planning to buy a home this year, saving for a down payment is one of the most important steps in the process. One of the best ways to jumpstart your savings is by starting with the help of your tax refund.

Using data from the Internal Revenue Service (IRS), it’s estimated that Americans can expect an average refund of $2,925 when filing their taxes this year. The map below shows the average anticipated tax refund by state:Thanks to programs from the Federal Housing Authority, Freddie Mac, and Fannie Mae, many first-time buyers can purchase a home with as little as 3% down. In addition, Veterans Affairs Loans allow many veterans to put 0% down. You may have heard the common myth that you need to put 20% down when you buy a home, but thankfully for most homebuyers, a 20% down payment isn’t actually required. It’s important to work with your real estate professional and your lender to understand all of your options.

How can your tax refund help?

If you’re a first-time buyer, your tax refund may cover more of a down payment than you realize.

If you take into account the median home sale price by state, the map below shows the percentage of a 3% down payment that’s covered by the average anticipated tax refund:The darker the blue, the closer your tax refund gets you to homeownership when you qualify for one of the low down payment programs. Maybe this is the year to plan ahead and put your tax refund toward the down payment on a home.

Not enough money from your tax return?

A recent paper from the National Bureau of Economic Research found that, of the households that received a stimulus check last year, “One third report that they primarily saved the stimulus money.” If you had the opportunity to save your Economic Impact Payments, you may consider putting that money toward your down payment or closing costs as well. Your trusted real estate professional can also advise you on the down payment assistance programs available in your area.

Bottom Line

Saving for a down payment can seem like a daunting task, but it doesn’t have to be. This year, your tax refund and your stimulus savings could add up big when it comes to reaching your homeownership goals.

Whether you’re buying your first home or selling your current house, if your needs are changing and you think you need to move, the decision can be complicated. You may have to take personal or professional considerations into account, and only you can judge what impact those factors should have on your desire to move.

However, there’s one category that provides a simple answer. When deciding to buy now or wait until next year, the financial aspect of the purchase is easy to evaluate. You just need to ask yourself two questions:

Do I think home values will be higher a year from now?

Do I think mortgage rates will be higher a year from now?

From a purely financial standpoint, if the answer is ‘yes’ to eitherquestion, you should strongly consider buying now. If the answer to both questions is ‘yes,’ you should definitely buy now.

Nobody can guarantee what home values or mortgage rates will be by the end of this year. The experts, however, seem certain the answer to both questions above is a resounding ‘yes.’ Mortgage rates are expected to rise and home values are expected to appreciate rather nicely.

What does this mean to you?

Let’s look at how waiting would impact your financial situation. Here are the assumptions made for this example:

The experts are right – mortgage rates will be 3.18% at the end of the year

The experts are right – home values will appreciate by 5.9%

You want to buy a home valued at $350,000 today

You decide on a 10% down payment

Here’s the financial impact of waiting:

You pay an extra $20,650 for the house

You need an additional $2,065 for a down payment

You pay an extra $116/month in your mortgage payment ($1,392 additional per year)

You don’t gain the $20,650 increase in wealth through equity build-up

Bottom Line

There are many things to consider when buying a home. However, from a purely financial aspect, if you find a home that meets your needs, buying now makes much more sense than buying next year.

If you’re thinking of buying a home this year, you may be wondering how much money you need to come up with for your down payment. Many people may think it’s 20% of the loan to secure a mortgage. While there are plenty of lower down payment options available for qualified buyers who don’t want to put 20% down, it’s important to understand how a larger down payment can have great benefits too.

The truth is, there are many programs available that allow you to put down as little as 3.5%, which can be a huge benefit to those who want to purchase a home sooner rather than later. Those who have served our country may also qualify for a Veterans Affairs Home Loan (VA) and may not need a down payment. These programs have really cut down the savings time for many potential buyers, enabling them to start building family wealth sooner.

Here are four reasons why putting 20% down is a good plan if you can afford it.

1. Your interest rate may be lower.

A 20% down payment vs. a 3-5% down payment shows your lender you’re more financially stable and not a large credit risk. The more confident your lender is in your credit score and your ability to pay your loan, the lower the mortgage interest rate they’ll likely be willing to give you.

2. You’ll end up paying less for your home.

The larger your down payment, the smaller your loan amount will be for your mortgage. If you’re able to pay 20% of the cost of your new home at the start of the transaction, you’ll only pay interest on the remaining 80%. If you put down 5%, the additional 15% will be added to your loan and will accrue interest over time. This will end up costing you more over the lifetime of your home loan.

3. Your offer will stand out in a competitive market.

In a market where many buyers are competing for the same home, sellers like to see offers come in with 20% or larger down payments. The seller gains the same confidence as the lender in this scenario. You are seen as a stronger buyer with financing that’s more likely to be approved. Therefore, the deal will be more likely to go through.

4. You won’t have to pay Private Mortgage Insurance (PMI)

“PMI is an insurance policy that protects the lender if you are unable to pay your mortgage. It’s a monthly fee, rolled into your mortgage payment, that is required for all conforming, conventional loans that have down payments less than 20%. Once you’ve built equity of 20% in your home, you can cancel your PMI and remove that expense from your mortgage payment.”

As mentioned earlier, when you put down less than 20% when buying a home, your lender will see your loan as having more risk. PMI helps them recover their investment in you if you’re unable to pay your loan. This insurance isn’t required if you’re able to put down 20% or more.

Many times, home sellers looking to move up to a larger or more expensive home are able to take the equity they earn from the sale of their house to put down 20% on their next home. With the equity homeowners have today, it creates a great opportunity to put those savings toward a 20% or greater down payment on a new home.

If you’re looking to buy your first home, you’ll want to consider the benefits of 20% down versus a smaller down payment option.

Bottom Line

If you’re thinking of buying a home and are already saving for your down payment, let’s connect to discuss what fits best with your long-term plans.

Is the idea of saving for a down payment holding you back from buying a home right now? You may be eager to take advantage of today’s low mortgage rates, but the thought of needing a large down payment might make you want to pump the brakes. Today, there’s still a common myth that you have to come up with 20% of the total sale price for your down payment. This means people who could buy a home may be putting their plans on hold because they don’t have that much saved yet. The reality is, whether you’re looking for your first home or you’ve purchased one before, youmost likelydon’t need to put 20% down. Here’s why.

“The most damaging down payment myth—since it stops the homebuying process before it can start—is the belief that 20% is necessary.”

If saving that much money sounds daunting, potential homebuyers might give up on the dream of homeownership before they even begin – but they don’t have to.

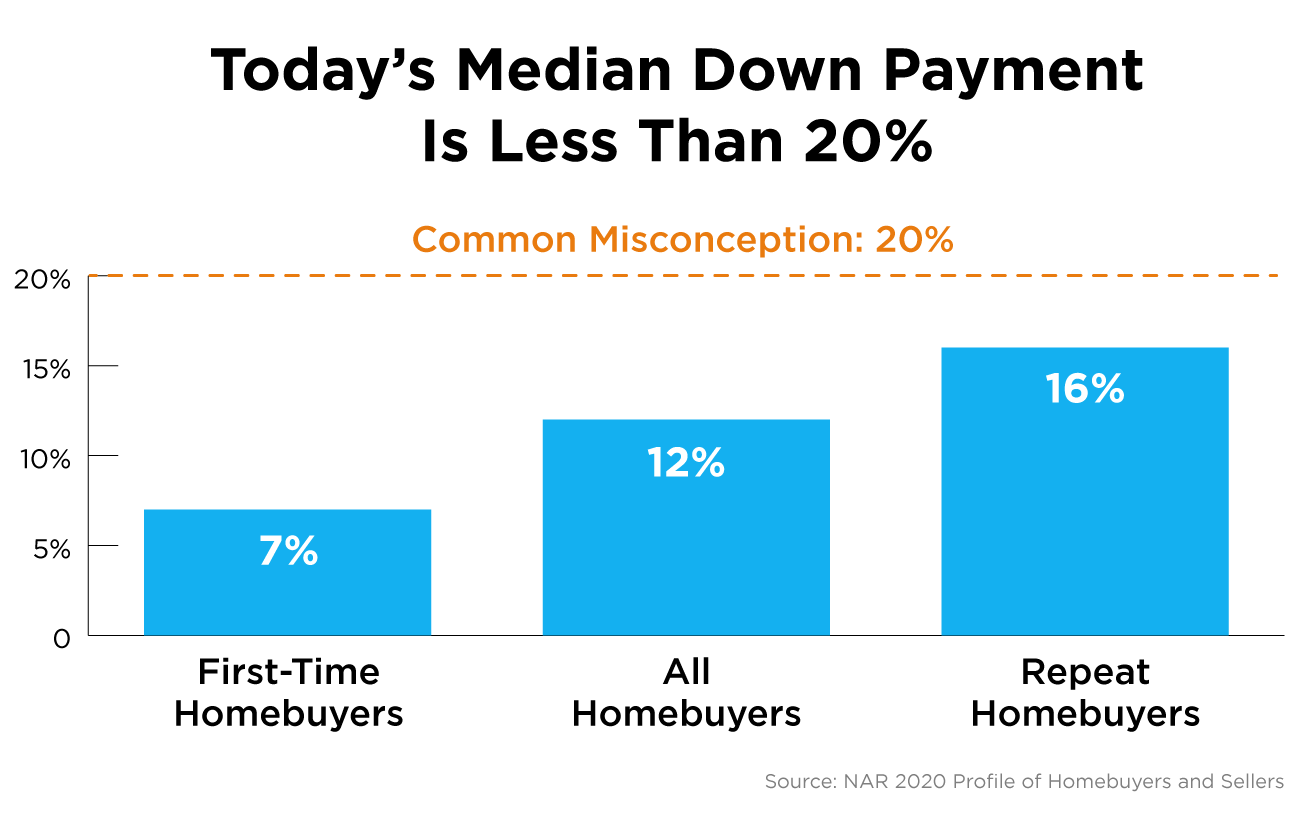

Data in the 2020 Profile of Home Buyers and Sellers from the National Association of Realtors (NAR) indicates that the median down payment actually hasn’t been over 20% since 2005, and even then, that was for repeat buyers, not first-time homebuyers. As the image below shows, today’s median down payment is clearly less than 20%.

What does this mean for potential homebuyers?

As we can see, the median down payment was lowest for first-time buyers with the 2020 percentage coming in at 7%. If you’re a first-time buyer and putting down 7% still seems high, understand that there are programs that allow qualified buyers to purchase a home with a down payment as low as 3.5%. There are even options like VA loans and USDA loans with no down payment requirements for qualified applicants.

It’s important for potential homebuyers (whether they’re repeat or first-time buyers) to know they likely don’t need to put down 20% of the purchase price, but they do need to do their homework to understand the options available. Be sure to work with trusted professionals from the start to learn what you may qualify for in the homebuying process.

Bottom Line

Don’t let down payment myths keep you from hitting your homeownership goals. If you’re hoping to buy a home this year, let’s connect to review your options.

In 1963, Martin Luther King, Jr. inspired a powerful movement with his famous “I Have a Dream” speech. Through his passion and determination, he sparked interest, ambition, and courage in his audience. Today, reflecting on his message encourages many of us to think about our own dreams, goals, beliefs, and aspirations. For many Americans, one of those common goals is owning a home: a piece of land, a roof over our heads, and a place where we can grow and flourish.

If you’re dreaming of buying a home this year, start by connecting with a local real estate professional to understand what goes into the process. With a trusted advisor at your side, you can then begin to answer the questions below to set yourself up for homebuying success.

1. How Can I Better Understand the Process, and How Much Can I Afford?

The process of buying a home is not one to enter into lightly. You need to decide on key things like how long you plan on living in an area, school districts you prefer, what kind of commute works for you, and how much you can afford to spend.

Keep in mind, before you start the process to purchase a home, you’ll also need to apply for a mortgage. Lenders will evaluate several factors connected to your financial track record, one of which is your credit history. They’ll want to see how well you’ve been able to minimize past debts, so make sure you’ve been paying your student loans, credit cards, and car loans on time. If your financial situation has changed recently, be sure to discuss that with your lender as well. Most agents have loan officers they trust and will provide referrals for you.

“Financial planners recommend limiting the amount you spend on housing to 25 percent of your monthly budget.”

2. How Much Do I Need for a Down Payment?

In addition to knowing how much you can afford on a monthly mortgage payment, understanding how much you’ll need for a down payment is another critical step. Thankfully, there are many different options and resources in the market to potentially reduce the amount you may think you need to put down.

If you’re concerned about saving for a down payment, start small and be consistent. A little bit each month goes a long way. Jumpstart your savings by automatically adding a portion of your monthly paycheck into a separate savings account or house fund. AmericaSaves.orgsays:

“Over time, these automatic deposits add up. For example, $50 a month accumulates to $600 a year and $3,000 after five years, plus interest that has compounded.”

Before you know it, you’ll have enough for a down payment if you’re disciplined and thoughtful about your process.

3. Saving Takes Time: Practice Living on a Budget

As tempting as it is to pass the extra time you may be spending at home these days with a little retail therapy, putting that extra money toward your down payment will help accelerate your path to homeownership. It’s the little things that count, so start trying to live on a slightly tighter budget if you aren’t doing so already. A budget will allow you to save more for your down payment and help you pay down other debts to improve your credit score.

A survey of millennial spending shows, “68% reported that shelter in place orders helped them save for their down payment.” Danielle Hale, Chief Economist at realtor.com, also notes:

“If there is any silver lining to the current economic landscape, it’s that mortgage rates are hanging around record lows…Additionally, shelter-in-place orders helped many who were fortunate enough to keep their jobs save for a down payment — one of the largest hurdles of buying a home. The combination of low rates and the opportunity to save is enabling many millennials to move up their home buying timeline.”

While you don’t need to cut all of the extras out of your current lifestyle, making smarter choices and limiting your spending in areas where you can slim down will make a big difference.

Bottom Line

If homeownership is on your dream list this year, take a good look at what you can prioritize to help you get there. To determine the steps you should take to start the process, let’s connect today.

In a year that was financially devastating for many Americans, some good news for most homeowners is the dramatic gain in home equity over the last twelve months. Last week, CoreLogic released its 2020 3rd Quarter Homeowner Equity Insights report, which reveals four major findings:

S. homeowners with mortgages have seen their equity increase by a total of $1 trillion since the third quarter of 2019.

The average homeowner gained approximately $17,000 in equity over the past year.

This is a 10.8% increase in equity over last year.

The average household with a mortgage now has $194,000 in home equity.

This has given many homeowners the ability to redesign their homes to meet their changing needs. Frank Martell, President and CEO of CoreLogic, explains in the report:

“The housing market has remained a strong pillar in an otherwise tumultuous economic year. A sharp rise in demand, spurred by record-low interest rates, continues to bolster homeowner equity. And with many people now spending more time than ever before at home, some homeowners have tapped into their strengthening equity to fund renovations.”

This build-up in equity also gives more options to homeowners who have been financially impacted by the pandemic. Today, homeowners with substantial equity are in a much better position to work out a deal with their lender if they cannot pay their mortgage. Alternatively, they also have the power to sell and walk away with their equity in the form of cash or as a down payment toward a more affordable house. Frank Nothaft, Chief Economist for CoreLogic, addresses the issue in the report:

“Over the past year, strong home price growth has created a record level of home equity for homeowners…This provides an important buffer to protect families if they experience financial difficulties and is one reason for the generational-low in foreclosure rates reported.”

Here’s a map showing equity gains by state:This gain in home equity is a blessing for homeowners in these trying times, and it seems that the next two years will continue to reward those who own a home.

Last week, the National Association of Realtors (NAR) held their 2020 Real Estate Forecast Summit. At the summit, they shared the results of a recent survey of 23 economic and housing market experts. The median forecast among the experts called for home values to increase further by 8% in 2021 and 5.5% in 2022.

Bottom Line

In a year that has many of us reevaluating what “home” really means, those who own their homes have been rewarded with a financial windfall that averages $17,000 individually and totals $1 trillion nationally.

Homeownership is on the goal list for many young adults, but sometimes it’s hard to know exactly how to get there. From understanding the homebuying process to pre-approval and down payment assistance options, uncertainty along the way can ultimately hold some buyers back.

Today, there are over 75 million Millennials and 67 million Gen Z’ers in the U.S., making up a significant number of both current and soon-to-be homebuyers. According to a recent Fannie Maesurvey of more than 2,000 of these individuals:

“88% said they are confident they will achieve homeownership someday.”

In addition, the survey also reveals that for younger generations, the motivation to own a home may be more emotional than financial compared to previous generations:

<50% say they want to use their home as an asset

78% believe it’s the best way to live the way they want, without restrictions

80% believe homeownership is the best way to make it on their own

Whether homeownership goals come from the heart or are driven by financial aspirations (or maybe both), the obstacles standing in the way don’t have to bring these dreams to a screeching halt. The same survey also reveals two key roadblocks for potential buyers. Thankfully, they’re both easily overcome with the power of knowledge and trusted advisors leading the way. Here’s a look at these two challenges potential homebuyers face today:

1. 73% of future homebuyers are unaware of low-down-payment mortgage options

For those who want to purchase a home, low-down-payment options are instrumental to affording one sooner rather than later, especially given the amount of debt many younger adults have accumulated. Fannie Mae also notes:

“Among the challenges they face is an unprecedented amount of debt, along with a lack of understanding of the mortgage process and their own purchasing power. Debt, in particular, creates many obstacles such as a limited ability to save and the fear of taking on more debt.”

Today, there are more than 2,340 down payment assistance programs available nationwide to help relieve this pressure. Understanding what’s out there and the options available may help many buyers become homeowners faster than they thought possible. In a year like this, with record-low mortgage rates making their mark in the history books, being able to take advantage of the opportunity buyers have right now is essential to long-term affordability.

2. 64% of buyers expect lenders and other real estate professionals to educate them about the mortgage process

While many people love to do a quick search online to find instant answers to their questions, it isn’t the only way younger generations want to consume information or build their knowledge base. As the survey mentions, having trusted professionals help them learn what it takes to achieve their dreams is definitely on their wish list too.

Bottom Line

If you’re aiming for homeownership someday, it may be in closer reach than you think. Let’s connect so you can learn about the process and get the guidance you need to make it happen.

My name is John Bendele and these are words to live by.

“What is the biggest challenge you are facing in life right now and how can I help?”

I believe when you are able to help others in their struggles, it will always bring a since of joy and accomplishment that is like no other. I enjoy bringing opportunities to people in real estate and in life. To be a lifting hand and a beacon of knowledge. It brings me great joy to guide and support others when making exciting and difficult choices. I have been a licensed realtor for over 7 years in Minnesota. Coming from a construction background, I will provide a wealth of knowledge about homes. Knowing homes allows me to a better negotiator with facts and details some may not. I enjoy working with sellers, investors and buyers.

I grew up in Southwest Texas and moved to Minnesota in 2015. I have lived in the White Bear Lake area until making a move over the lake to Willernie, MN where I now reside. I love spending quality time with my teenage boys who nicknamed me “JoJo”. My favorite things to do are being outdoors on or in the water, BBQing (TX style) and going on any adventure.

I want to bring knowledge, growth, excitement and wealth to the clients I encounter through being a realtor. I look forward to assisting you in your amazing journey in real estate.

Thank you,

John A Bendele

Meet Brittany

Brittany is a mama of three kiddos, a wife of a firefighter and added more love to her home with three dogs and two cats. Outside of the fun she has as an agent and her roles at home she enjoys doing any DIY projects she can get her hands on!

Brittany fell in love with the Real Estate gig in 2019. She grew up in Apple Valley, and now owns her childhood home. I guess you could say she is a south metro pro!

You!

Hey! If you’re looking for your next role as an agent let us know! This could be you!

Meet Shea Amundson

Hey, I’m Shea and I love helping people find a beautiful home that sets their soul on fire!

Meet Katie

Katie comes from the busy world of entertainment and being a Traveling Operations Manager. She transitioned to Real Estate back in 2018 and has been hooked ever since! Katie thrives on training, developing new systems, and helping agents grow! Katie joins Voila with the determination to help every agent and client make their dream a reality whether it be building their business or finding that dream home!

When Katie isn’t working, she is a full-time student at Metropolitan University. She enjoys cooking foods from all over the world, traveling, and has a habit of getting a new tattoo wherever she goes. She is huge into animal conservation and spending time with her dog Sawyer who often joins her on travels!

Meet Sarah Beth Lindstrom

Sarah wants to live in a world filled with innovative businesses daring enough to break the mold…monthly auto-shipments of Laffy Taffy’s, and lots and lots of laughter!!!

Having been in the real estate industry since 2005, her go to role has always been supporting her teams in any way that she can! She has gone from Listing and Transaction Management, to Team Manager, and now Director of Support! She is an ‘introverted extrovert’ that finds the, ‘behind the scenes’ with a hint of showing homes – to be a perfect blend.

When she’s not supporting her Voila Family, she is out getting one more rep in at the gym, finding new healthy recipes to attempt (and then trick her teenager into eating somehow), and enjoying quick road trips to…well, anywhere! She also plays on a competitive volleyball team in the winter, sand volleyball in the summer and softball in the spring and fall.

“Two things define you. The patience you have when you have nothing and the attitude when you have everything.”

Meet Jessi Andersen

In June of 2020 Jessi joined team of Voila…and…it’s that easy!

Ha! No really, it did all begin in June. New to this side of Real Estate, Jessi joined in hopes to take her chatty, outgoing self and bring some good of it! Her natural tendencies of networking and love of growth and goals, have been set in direction – expanding Voila!

Where is Jess when she isn’t nurturing the growth of Voila? Adventuring with her family outside in nature. Or perhaps baking up a new recipe while dancing the day away – and of course cheering for her little athletes at home, as well as the MN Vikings/Twins!

“In the end it is not the years in your life that count. It’s the life in your years” ~ Abe Lincoln

Meet Wyatt Lemon

Wyatt is a Real Estate Extraordinaire, and a Loving Husband, and a Lover of Life and a PAW-rent to 3 awesome dogs. Huge believer in the idea that life is what you make of it, so with that being said I guess you could say the glass is half full! Things I enjoy outside of work are Yoga, being a big time Foodie, and spending time with my family. I grew up in Hugo MN and have been a local resident my whole life. I studied Marketing at Century College as well as St. Cloud State University. I got into Real Estate in October of 2018 and have loved every minute of it!

Meet James Andersen

James Andersen is a human being who believes that the best in others is a reflection of the energy we bring.

Magnanimous behavior is the standard not the exception.

10+ years Army Career

5+ years Married

5+ years Father of Calendar Crushers

5+ years Real Estate Career

30+ years Life Experience

Let’s learn and grow together.

Meet Joey Torkildson

You are writing your own story in life! Is what you are doing right now supposed to be in that story? I hope so!

That’s why my goal is to always sign up, get uncomfortable, inspire through doing, shoot, then aim. We don’t have enough time on this planet to stay mundane and there are too many experiences to be doing one thing for too long! It’s all about the short term experiments!

Quick background: 19+ year US Army Master Sergeant vet; 10+ year transformer of lives through ownership (AKA: Realtor) ; 2+ year CEO of an Expansion Team with Hergenrother Realty Group ; Director of Agent Training with that same organization; Self employed for 12+ years; starting in late 2019 CoFounded a new disruptive real estate brokerage, Voila; Contagiously energetic teacher who loves helping people discover they can accomplish anything; Dad of two extremely crazy and loving boys; Husband of an amazingly supportive and ultimate gardener wife.

Let’s be curious explorers together! I love connecting with people and helping them achieve their goals and I’m a firm believer in the fact that you are one introduction away from your entire life changing!

Two quotes I live by: Amazing things rarely happen in your comfort zone and only those who attempt the absurd achieve the impossible!