If you’re trying to buy a home and are having a hard time finding one you can afford, it may be time to consider a fixer-upper.

Auto Added by WPeMatico

If you’re trying to buy a home and are having a hard time finding one you can afford, it may be time to consider a fixer-upper.

If you’re taking a look at your expenses as you retire, saving money where you can has a lot of appeal. One long-standing, popular way to do that is by downsizing to a smaller home.

When you think about cutting down on your spending, odds are you think of frequent purchases, like groceries and other goods. But when you downsize your house, you often end up downsizing the bills that come with it, like your mortgage payment, energy costs, and maintenance requirements. Realtor.com shares:

“A smaller home typically means lower bills and less upkeep. Then there’s the potential windfall that comes from selling your larger home and buying something smaller.”

That windfall is thanks to your home equity. If you’ve been in your house for a while, odds are you’ve built up a considerable amount of equity. And that equity is something you can use to help you buy a home that better fits your needs today. Daniel Hunt, CFA at Morgan Stanley, explains:

“Home equity can be a significant source of wealth for retirees, often representing a large portion of their net worth. . . . Retirement planning can be complex, but your home equity shouldn’t be overlooked.”

And when you’re ready to use that equity to fuel your next move, your real estate agent will be your guide through every step of the process. That includes setting the right price for your current house when you sell, finding the home that best fits your evolving needs, and understanding what you can afford at today’s mortgage rate.

If you’re thinking about downsizing, ask yourself these questions:

Then, meet with a real estate agent to get an answer to this one: What are my options in the market right now? A local real estate agent can walk you through how much equity you have in your house and how it positions you to win when you downsize.

Want to save money in retirement? Consider downsizing – it could really help you out. When you’re ready, connect with a local real estate agent about your goals in the housing market this year.

If you want to buy a home, you should know your credit score is a critical piece of the puzzle when it comes to qualifying for a mortgage. Lenders review your credit to see if you typically make payments on time, pay back debts, and more. Your credit score can also help determine your mortgage rate. An article from US Bank explains:

“A credit score isn’t the only deciding factor on your mortgage application, but it’s a significant one. So, when you’re house shopping, it’s important to know where your credit stands and how to use it to get the best mortgage rate possible.”

That means your credit score may feel even more important to your homebuying plans right now since mortgage rates are a key factor in affordability. According to the Federal Reserve Bank of New York, the median credit score in the U.S. for those taking out a mortgage is 770. But that doesn’t mean your credit score has to be perfect. The same article from US Bank explains:

“Your credit score (commonly called a FICO Score) can range from 300 at the low end to 850 at the high end. A score of 740 or above is generally considered very good, but you don’t need that score or above to buy a home.”

Working with a trusted lender is the best way to get more information on how your credit score could factor into your home loan and the mortgage rate you’re able to get. As FICO says:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single “cutoff score” used by all lenders and there are many additional factors that lenders may use to determine your actual interest rates.”

If you’re looking for ways to improve your score, Experian highlights some things you may want to focus on:

Finding ways to make your credit score better could help you get a lower mortgage rate. If you want to learn more, talk to a trusted lender.

No matter how you slice it, buying or selling a home is a big decision. And when you’re going through any change in your life and you need some guidance, what do you do? You get advice from people who know what they’re talking about.

Moving is no exception. You need insights from the pros to help you feel confident in your decision. Freddie Mac explains it like this:

“As you set out to find the right home for your family, be sure to select experienced, trusted professionals who will help you make informed decisions and avoid pitfalls.”

And while perfect advice isn’t possible – not even from the experts, what you can get is the very best advice out there.

For example, let’s say you need an attorney. You start off by finding an expert in the type of law required for your case. Once you do, they won’t immediately tell you how the case is going to end, or how the judge or jury will rule. But what a good attorney can do is walk you through the most effective strategies based on their experience and help you put a plan together. They’ll even use their knowledge to adjust that plan as new information becomes available.

The job of a real estate agent is similar. Just like you can’t find a lawyer to give you perfect advice, you won’t find a real estate professional who can either. That’s because it’s impossible to know everything that’s going to happen throughout your transaction. Their role is to give you the best advice they can.

To do that, an agent will draw on their experience, industry knowledge, and market data. They know the latest trends, the ins and outs of the homebuying and selling processes, and what’s worked for other people in the same situation as you.

With that expertise, a real estate advisor can anticipate what could happen next and work with you to put together a solid plan. Then, they’ll guide you through the process, helping you make decisions along the way. That’s the very definition of getting the best – not perfect – advice. And that’s the power of working with a real estate advisor.

If you’re looking to buy or sell a home, you want an expert on your side to help you each step of the way. Connect with a real estate professional so you have advice you can count on.

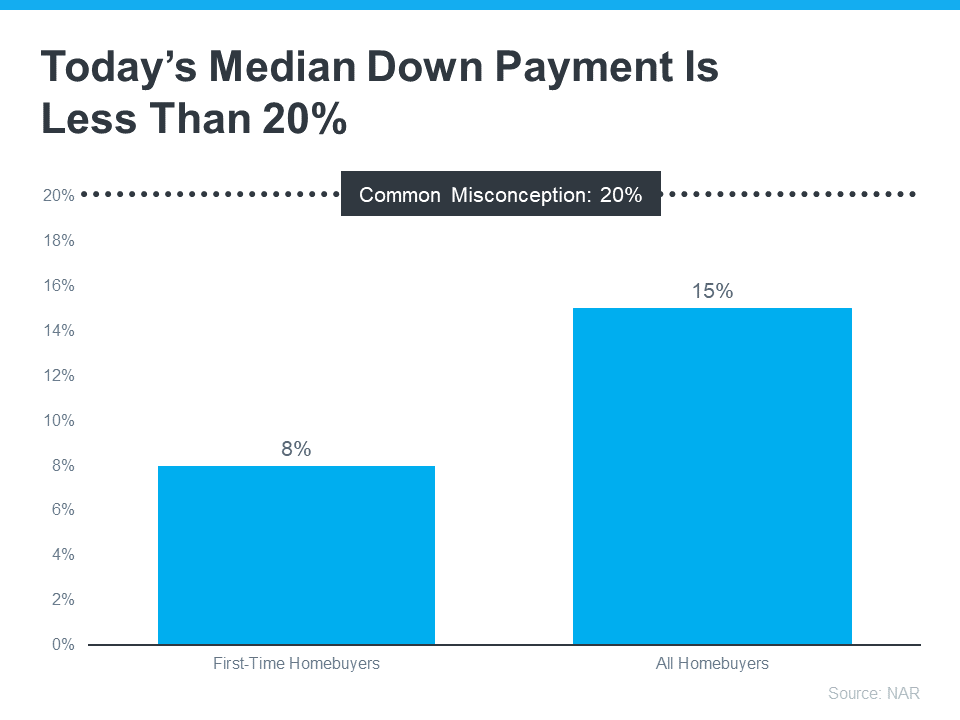

If you’re planning to buy your first home, saving up for all the costs involved can feel daunting, especially when it comes to the down payment. That might be because you’ve heard you need to save 20% of the home’s price to put down. Well, that isn’t necessarily the case.

Unless specified by your loan type or lender, it’s typically not required to put 20% down. That means you could be closer to your homebuying dream than you realize.

As The Mortgage Reports says:

“Although putting down 20% to avoid mortgage insurance is wise if affordable, it’s a myth that this is always necessary. In fact, most people opt for a much lower down payment.”

According to the National Association of Realtors (NAR), the median down payment hasn’t been over 20% since 2005. In fact, for all homebuyers today it’s only 15%. And it’s even lower for first-time homebuyers at just 8% (see graph below):

The big takeaway? You may not need to save as much as you originally thought.

According to Down Payment Resource, there are also over 2,000 homebuyer assistance programs in the U.S., and many of them are intended to help with down payments.

Plus, there are loan options that can help too. For example, FHA loans offer down payments as low as 3.5%, while VA and USDA loans have no down payment requirements for qualified applicants.

With so many resources available to help with your down payment, the best way to find what you qualify for is by consulting with your loan officer or broker. They know about local grants and loan programs that may help you out.

Don’t let the misconception that you have to have 20% saved up hold you back. If you’re ready to become a homeowner, lean on the professionals to find resources that can help you make your dreams a reality. If you put your plans on hold until you’ve saved up 20%, it may actually cost you in the long run. According to U.S. Bank:

“. . . there are plenty of reasons why it might not be possible. For some, waiting to save up 20% for a down payment may “cost” too much time. While you’re saving for your down payment and paying rent, the price of your future home may go up.”

Home prices are expected to keep appreciating over the next 5 years – meaning your future home will likely go up in price the longer you wait. If you’re able to use these resources to buy now, that future price growth will help you build equity, rather than cost you more.

Keep in mind that you don’t always need a 20% down payment to buy a home. If you’re looking to make a move this year, reach out to a trusted real estate professional to start the conversation about your homebuying goals.

Buying your first home is a big, exciting step and a major milestone that has the power to improve your life. As a first-time homebuyer, it’s a dream you can make come true, but there are some hurdles you’ll need to overcome in today’s housing market – specifically the limited supply of homes for sale and ongoing affordability challenges.

So, if you’re ready, willing, and able to buy your first home, here are three tips to help you turn your dream into a reality.

Paying the initial costs of homeownership, like your down payment and closing costs, can feel a bit daunting. But there are many assistance programs for first-time homebuyers that can help you get a loan with little or no money upfront. According to Bankrate:

“. . . you might qualify for a first-time homebuyer loan or assistance. First-time buyer loans typically have more flexible requirements, such as a lower down payment and credit score. Many help buyers with closing costs and the down payment through grants and low-interest loans.”

To find out more, talk to your state’s housing authority or check out websites like Down Payment Resource.

Right now, there aren’t enough homes for sale for everyone who wants to buy one. That’s pushing home prices up and making affordability tight for buyers. One way to deal with that issue and find a home right now is to consider condos and townhomes. Realtor.com explains:

“For many newbies, it might just be a matter of making a shift toward something they can better afford—like a condo or townhome. These lower-cost homes have historically been a stepping stone for buyers looking for a less expensive alternative to a single-family home.”

One reason why they may be more affordable is because they’re often smaller. But they still give you the chance to get your foot in the door and achieve your goal of owning a home and building equity. And that equity can help fuel your move into a larger home later on if you decide you need something bigger in the future. Hannah Jones, Senior Economic Analyst at Realtor.com, says:

“Condos can help prospective homebuyers who perhaps have a smaller budget, but who are really determined to get a foothold in the market and start to accumulate some equity. It can be a really great entry point.”

Another way to break into the market is by purchasing a home with friends or loved ones. That way you can split the cost of things like the mortgage and bills, to make it easier to afford a home. According to Money.com:

“Buying a home with another person has some obvious advantages in the mortgage department. With two incomes in the mix, buyers can likely qualify for a larger mortgage — a big help in today’s high-cost market.”

By exploring first-time homebuyer assistance, condos, townhomes, and multi-generational living, it can be easier to find and buy your first home. When you’re ready, connect with a local real estate agent.

Chances are at some point in your life you’ve heard the phrase, home is where the heart is. There’s a reason that’s said so often. Becoming a homeowner is emotional.

So, if you’re trying to decide if you want to keep on renting or if you’re ready to buy a home this year, here’s why it’s so easy to fall in love with homeownership.

Your house should be a space that’s uniquely you. And, if you’re a renter, that can be hard to achieve. When you rent, the paint colors are usually the standard shade of white, you don’t have much control over the upgrades, and you’ve got to be careful how many holes you put in the walls. But when you’re a homeowner, you have a lot more freedom. As the National Association of Realtors (NAR) says:

“The home is yours. You can decorate any way you want and choose the types of upgrades and new amenities that appeal to your lifestyle.”

Whether you want to paint the walls a cheery bright color or go for a dark moody tone, you can match your interior to your vibe. Imagine how it would feel to come home at the end of the day and walk into a space that feels like you.

One of the hardest things about renting is the uncertainty of what happens at the end of your lease. Does your payment go up so much that you have to move? What if your landlord decides to sell the property? It’s like you’re always waiting for the other shoe to drop. Jeff Ostrowski, a business journalist covering real estate and the economy, explains how homeownership can give you more peace of mind in a Money Geek article:

“Homeownership means you are the boss and have the biggest say in your lifestyle and family decisions. Suppose your kids are in public school and you don’t want to risk having them change schools because your landlord doesn’t renew your lease. Owning a home would remove much of the risk of having to move.”

You may also find you feel much more at home in the community once you own a house. That’s because, when you buy a home, you’re staking a claim and saying, I’m a part of this community. You’ll have neighbors, block parties, and more. And that’ll give you the feeling of being a part of something bigger. As the International Housing Association explains:

“. . . homeowning households are more socially involved in community affairs than their renting counterparts. This is due to both the fact that homeowners expect to remain in the community for a longer period of time and that homeowners have an ownership stake in the neighborhood.”

Becoming a homeowner is a journey – and it may have been a long road to get to the point where you’re ready to take the plunge. If you’re seriously considering leaving behind your rental and making this commitment, you should know the emotions that come with this owning a home are powerful. You’ll be able to walk up to your front door every day and have that sense of accomplishment welcome you home.

A home is a place that reflects who you are, a safe space for the ones you love the most, and a reflection of all you’ve accomplished. Connect with a local real estate professional if you’re ready to break up with your rental and buy a home.

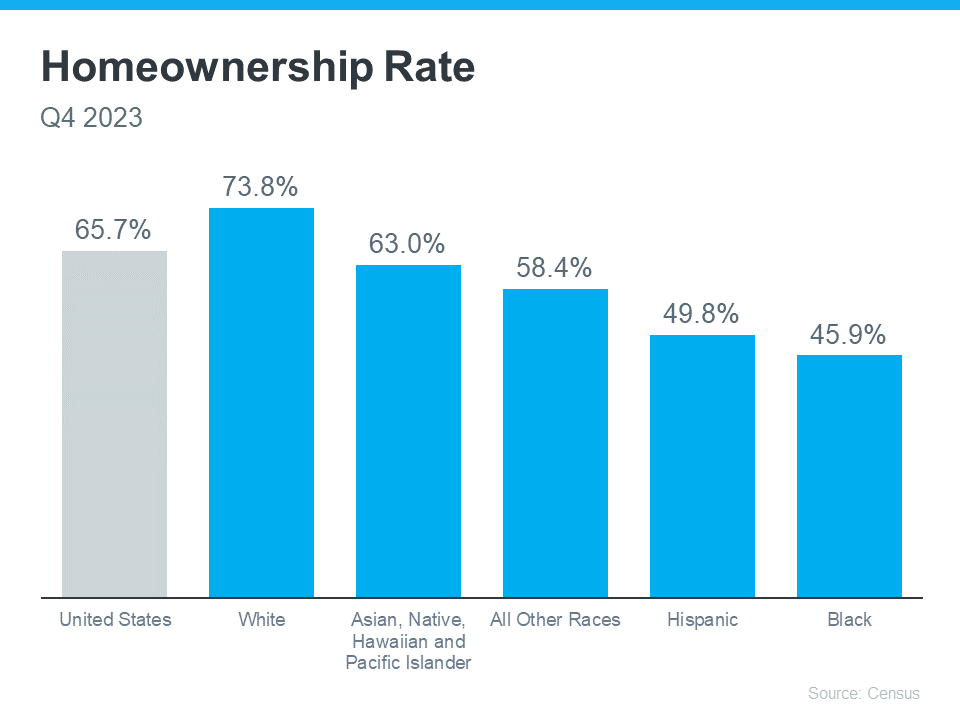

Homeownership is a major part of the American Dream. But, the path to achieving this dream can be quite difficult. While progress has been made to improve fair housing access, households of color still face unique challenges on the road to owning a home. Working with the right real estate experts can make all the difference for diverse buyers.

It’s clear that achieving homeownership is more challenging for certain groups because there’s still a measurable gap between the overall average U.S. homeownership rate and that of non-white groups. Today, Black households continue to have the lowest homeownership rate nationally (see graph below):

Homeownership is an important part of building household wealth that can be passed down to future generations. According to a report by the National Association of Realtors (NAR), almost half of Black homebuyers in 2023 were first-time buyers. That means many didn’t have home equity they could use toward their home purchase.

That financial hurdle alone makes buying a home more challenging, especially at a time when affordability is a major concern for first-time buyers. Jessica Lautz, Deputy Chief Economist at NAR says:

“It’s an incredibly difficult market for all home buyers right now, especially first-time home buyers and especially first-time home buyers of color.”

Because of these challenges, there are several down payment assistance programs specifically aimed at helping minority buyers fulfill their homeownership dreams:

Even if you don’t qualify for these programs, there are many other federal, state, and local options available to look into. And a real estate professional can help you find the ones that best meet your needs.

For minority homebuyers, the challenges that remain can be a point of pain and frustration. That’s why it’s so important for members of diverse groups to have the right team of experts on their sides throughout the homebuying process. These professionals aren’t only experienced advisors who understand the market and give the best advice, they’re also compassionate educators who will advocate for your best interests every step of the way.

Connect with a real estate professional to make sure you have to make sure you have the information and support you need as you walk the path to homeownership.

On the road to becoming a homeowner? If so, you may have heard the term pre-approval get tossed around. Let’s break down what it is and why it’s important if you’re looking to buy a home in 2024.

As part of the homebuying process, your lender will look at your finances to figure out what they’re willing to loan you. According to Investopedia, this includes things like your W-2, tax returns, credit score, bank statements, and more.

From there, they’ll give you a pre-approval letter to help you understand how much money you can borrow. Freddie Mac explains it like this:

“A pre-approval is an indication from your lender that they are willing to lend you a certain amount of money to buy your future home. . . . Keep in mind that the loan amount in the pre-approval letter is the lender’s maximum offer. Ultimately, you should only borrow an amount you are comfortable repaying.”

Now, that last piece is especially important. While home affordability is getting better, it’s still tight. So, getting a good idea of what you can borrow can help you really wrap your head around the financial side of things. It doesn’t mean you should borrow the full amount. It just tells you what you can borrow from that lender.

This sets you up to make an informed decision about your numbers. That way you’re able to tailor your home search to what you’re actually comfortable with budget-wise and can act fast when you find a home you love.

If you want to buy a home this year, there’s another reason you’re going to want to be sure you’re working with a trusted lender to make this a priority.

While more homes are being listed for sale, the overall number of available homes is still below the norm. At the same time, the recent downward trend in mortgage rates compared to last year is bringing more buyers back into the market. That imbalance of more demand than supply creates a bit of a tug-of-war for you.

It means you’ll likely find you have more competition from other buyers as more and more people who were sitting on the sidelines when mortgage rates were higher decide to jump back in. But pre-approval can help with that too.

Pre-approval shows sellers you mean business because you’ve already undergone a credit and financial check. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“Preapproval carries more weight because it means lenders have actually done more than a cursory review of your credit and your finances, but have instead reviewed your pay stubs, tax returns and bank statements. A preapproval means you’ve cleared the hurdles necessary to be approved for a mortgage up to a certain dollar amount.”

Sellers love that because that makes it more likely the sale will move forward without unexpected delays or issues. And if you may be competing with another buyer to land your dream home, why wouldn’t you do this to help stack the deck in your favor?

If you’re looking to buy a home in 2024, know that getting pre-approved is going to be a key piece of the puzzle. With lower mortgage rates bringing more buyers back into the market, this can help you make a strong offer that stands out from the crowd.

Finding the right home is one of the biggest challenges for potential buyers today. Right now, the supply of homes for sale is still low. But there is a bright spot. Newly built homes make up a larger percent of the total homes available for sale than normal. That’s why, if you’re craving more options, it makes sense to see if a newly built home is right for you.

But it’s important to remember the process of working with a builder is different than buying from a homeowner. And, while builders typically have sales agents on-site, having your own agent helps make sure you have proper representation throughout your homebuying journey. As Realtor.com says:

“Keep in mind that the on-site agent you meet at a new-construction office works for the builder. So, as the homebuyer, it’s a smart idea to bring in your own agent, as well, to help you negotiate and stay protected in the transaction.”

Here’s how having your own agent is key when you build or buy a new construction home.

It’s important to consider how the neighborhood and surrounding area may evolve before making your home purchase. Your agent is well-versed in the upcoming communities and developments that could influence your decision. One way a real estate agent can help is by reviewing the builder’s site plan. For example, you’ll want to know if there are any plans to construct a highway or add a drainage ditch behind your prospective backyard.

An agent also has expertise in the construction quality and reputation of different builders. They can give you insights into each one’s track record, customer satisfaction, and construction practices. Armed with this information, you can choose a builder known for consistently delivering top-notch homes.

The most obvious benefit of opting for new home construction is the opportunity to customize your home. Your agent will guide you through that process and share advice on the upgrades that are most likely to add long-term value to your home. Their expertise helps make sure you focus your budget on areas that will give you the greatest return on your investment later.

When it comes to working with builders, having a skilled negotiator on your side can make all the difference. Builder contracts can be complex. Your agent can help you navigate these contracts to make sure you fully understand the terms and conditions. Plus, agents are skilled negotiators who can advocate for you, potentially securing better deals, upgrades, or incentives throughout the process. As Realtor.com says:

“A good buyer’s agent will be able to review any contracts before you sign on the dotted line, ensuring you aren’t unwittingly agreeing to terms that only benefit the builder.”

If you are interested in buying or building a new construction home, having a trusted agent by your side can make a big difference. If you’d like to start that conversation, connect with a local real estate agent.