Last month, in a post on the Liberty Street Economics blog, the Federal Reserve Bank of New York noted that Americans believe buying a home is definitely or probably a better investment than buying stocks. Last week, a Gallup Poll reaffirmed those findings.

In an article on the current real estate market, Gallup reports:

“Gallup usually finds that Americans regard real estate as the best long-term investment among several options — seeing it as superior to stocks, gold, savings accounts and bonds. This year, 41% choose real estate as the best investment, up from 35% a year ago, with stocks a distant second.”

Here’s the breakdown:The article goes on to say:

“The 41% choosing real estate is the highest selecting any of the five investment options in the 11 years Gallup has asked this question.”

Is real estate really a secure investment right now?

Some question American confidence in real estate as a good long-term investment right now. They fear that the build-up in home values may be mirroring what happened right before the housing crash a little more than a decade ago. However, according to Merrill Lynch, J.P. Morgan, Morgan Stanley, and Goldman Sachs, the current real estate market is strong and sustainable.

As Morgan Stanley explains to their clients in a recent Thoughts on the Marketpodcast:

“Unlike 15 years ago, the euphoria in today’s home prices comes down to the simple logic of supply and demand. And we at Morgan Stanley conclude that this time the sector is on a sustainably, sturdy foundation . . . . This robust demand and highly challenged supply, along with tight mortgage lending standards, may continue to bode well for home prices. Higher interest rates and post pandemic moves could likely slow the pace of appreciation, but the upward trajectory remains very much on course.”

Bottom Line

America’s belief in the long-term investment value of homeownership has been, is, and will always be, very strong.

Buying your first home can be fraught with trouble and expenses that could be avoided if you learn what other first-time homebuyers wish they knew going in. Here is a list to help you prepare.

Get Mortgage Pre-approval Before Looking for a Home

Don’t get attached to a particular home to buy before you are preapproved. Getting pre-approval for a mortgage tells you what you can afford. It also speeds up the offer and purchase process and helps sellers take you seriously over other offers that still require approval. You could lose out on a home if you must wait to get approved.

Monthly Payments Are as Important as the Total Home Price

When assessing the affordability of a home, even if the price fits your approved mortgage amount, it’s important to figure out the monthly payments with the taxes, interest, and insurance added. First-time buyers often underestimate this and then struggle after the sale to afford their new home.

Be Choosey About Your Lender

Make sure your mortgage lender works with and for you in a timely manner. Don’t just settle on the first one you talk to without ensuring their promptness. Compare rates and be aware that a lender who doesn’t take your needs seriously could sabotage your negotiations with a seller.

Inspections Aren’t Just a Legal Technicality

Don’t be in such a hurry for your selected home to pass inspection just so your mortgage company gives the green light. You want to dig deeper than the surface in an inspection to be sure there are no major costly issues with the house and property that you will regret later. Get a well-respected inspector to go over the home, top to bottom. Finding issues may not deter you from buying, but it may help you negotiate a better price that will mitigate the expense of getting extra repair work done after the sale.

Don’t Compromise What You Want to Save a Few Thousand Dollars

Whether you get a 15 or 30-year mortgage, a few extra grand won’t necessarily add that much hardship to the practical cost for a home that provides the size, features and value you need over time. Remember, it’s also about what you can pay monthly, which can be lessened with a higher down payment, better interest rates, lower closing costs, property taxes, and insurance. Don’t skimp on important needs, or you may grow out of the house and end up paying for another move too soon.

Be Prepared for a Wild Emotional Ride

Buying a home is a wonderful step into your independent financial goals, along with finally being a homeowner. You should also realize that many things can go wrong. Sellers can make your life difficult. Mortgage rules and paperwork is exhausting. Offers can look promising and then fall through at the last minute. Buying a home can be extremely stressful. The bottom line is to keep a check on your emotions and don’t get discouraged when circumstances change.

Using Voila! real estate services can help you make good early decisions in this crazy seller’s market. Don’t go it alone, especially in your first time buying. Let us help you walk through the process with confidence. Remember, you don’t pay for the services of a buyer’s agent since all fees are paid by the seller. Contact us today!

When buying a home, it’s important to have a budget and make sure you plan ahead for certain homebuying expenses. Saving for a down payment is the main cost that comes to mind for many, but budgeting for the closing costs required to get a mortgage is just as important.

“When you close on a home, a number of fees are due. They typically range from 2% to 5% of the total cost of the home, and can include title insurance, origination fees, underwriting fees, document preparation fees, and more.”

For example, for someone buying a $300,000 home, they could potentially have between $6,000 and $15,000 in closing fees. If you’re in the market for a home above this price range, your closing costs could be greater. As mentioned above, closing costs are typically between 2% and 5% of your purchase price.

“There will be lots of paperwork in front of you on closing day, and not enough time to read them all. Work closely with your real estate agent, lender, and attorney, if you have one, to get all the documents you need ahead of time.

The most important thing to read is the closing disclosure, which shows your loan terms, final closing costs, and any outstanding fees. You’ll get this form about three days before closing since, once you (the borrower) sign it, there’s a three-day waiting period before you can sign the mortgage loan docs. If you have any questions about the numbers or what any of the mortgage terms mean, this is the time to ask—your real estate agent is a great resource for getting you all the answers you need.”

Bottom Line

As home prices are rising and more buyers are finding themselves competing in bidding wars, it’s more important than ever to make sure your plan includes budgeting for closing costs. Let’s connect to be sure you have everything you need to land your dream home.

Over the past year, the pandemic made it challenging for some homeowners to make their mortgage payments. Thankfully, the government initiated a forbearance program to provide much-needed support. Unless they’re extended once again, some of these plans and the corresponding mortgage payment deferral options will expire soon. That said, there’s still time to request assistance. If your loan is backed by HUD/FHA, USDA, or VA, you can apply for initial forbearance by June 30, 2021.

Recently, the Consumer Finance Institute of the Federal Reserve Bank of Philadelphiasurveyed a national sample of 1,172 homeowners with mortgages. They discussed their familiarity with and understanding of lender accommodations that might be available under the Coronavirus Aid, Relief, and Economic Security (CARES) Act. The results indicate that some borrowers didn’t take advantage of the support available through forbearance:

“Most borrowers who had not used forbearance during the pandemic reported that it was because they simply did not need it. However, among the remainder, a lack of understanding about available accommodations may also be playing a role. Around 2 out of 3 in this group reported not seeking forbearance because they were unsure or pessimistic about whether they would qualify — even though a high fraction of borrowers are eligible for forbearance under the Coronavirus Aid, Relief, and Economic Security (CARES) Act.”

Here are some of the reasons why those borrowers didn’t opt for forbearance:

They were concerned forbearance may be costly

They didn’t understand how to request forbearance

They didn’t understand how the plans worked and/or whether they would qualify

If you have similar questions or concerns, the following answers may ease your fears.

If you’re concerned forbearance may be costly:

The Consumer Financial Protection Bureau (CFPB) explains:

“For most loans, there will be no additional fees, penalties, or additional interest (beyond scheduled amounts) added to your account, and you do not need to submit additional documentation to qualify. You can simply tell your servicer that you have a pandemic-related financial hardship.”

It’s important to contact your mortgage provider (the company you send your mortgage payment to every month) to explain your current situation and determine the best plan available for your needs.

If you’re not sure how to request forbearance:

Here are 5 steps to follow when requesting mortgage forbearance:

Find the contact information for your servicer

Call your servicer

Ask if you’re eligible for protection under the CARES Act

Ask what happens when your forbearance period ends

Ask your servicer to provide the agreement in writing

If you don’t understand how the plans work and/or whether you will qualify:

This is how the Consumer Financial Protection Bureau (CFPB) explains the program:

“Forbearance is when your mortgage servicer or lender allows you to pause or reduce your mortgage payments for a limited time while you build back your finances…

Forbearance doesn’t mean your payments are forgiven or erased. You are still obligated to repay any missed payments, which, in most cases, may be repaid over time or when you refinance or sell your home. Before the end of the forbearance, your servicer will contact you about how to repay the missed payments.”

The CFPB also addresses who qualifies for forbearance relief:

“You may have a right to a COVID hardship forbearance if:

You experience financial hardship directly or indirectly due to the coronavirus pandemic.

You have a federally backed mortgage, which includes HUD/FHA, VA, USDA, Fannie Mae, and Freddie Mac loans.

For mortgages that are not federally backed, servicers may offer similar forbearance options. If you are struggling to make your mortgage payments, servicers are generally required to discuss payment relief options with you, whether or not your loan is federally backed.”

Bottom Line

Like many Americans, your home may be your biggest asset. By acting quickly, you might be able to take advantage of critical relief options to help keep you in your home. Even if you tried to apply at the beginning of the pandemic and it for some reason didn’t work out, try again. Contact your mortgage provider today to determine if you qualify. If you have additional concerns, let’s connect to answer your questions and determine if there are other mortgage relief options in our area as well.

It’s clear that consumers are concerned about how quickly home values are rising. Many people fear the speed of appreciation may lead to a crash in prices later this year. In fact, Google reports that the search for “When is the housing market going to crash?” has actually spiked 2450% over the past month.

“One of the most noteworthy things that came up in Inman’s conversations with agents was that every single one said they’ve had conversations with clients about whether or not the market is heading into a bubble.”

To alleviate some of these concerns, let’s look at what several financial analysts are saying about the current residential real estate market. Within the last thirty days, four of the major financial services giants came to the same conclusion: the housing market is strong, and price appreciation will continue. Here are their statements on the issue:

“Strong demand for housing looks sustainable. Even before the pandemic, demographic tailwinds and historically-low mortgage rates had pushed demand to high levels. … consumer surveys indicate that household buying intentions are now the highest in 20 years. … As a result, the model projects double-digit price gains both this year and next.”

“Homebuyers—interest rates are still historically low, though they are inching up. Housing prices have spiked during the last six-to-nine months, but we don’t expect them to fall soon, and we believe they are more likely to keep rising. If you are looking to purchase a new home, conditions now may be better than 12 months hence.”

“Unlike 15 years ago, the euphoria in today’s home prices comes down to the simple logic of supply and demand. And we at Morgan Stanley conclude that this time the sector is on a sustainably, sturdy foundation . . . . This robust demand and highly challenged supply, along with tight mortgage lending standards, may continue to bode well for home prices. Higher interest rates and post pandemic moves could likely slow the pace of appreciation, but the upward trajectory remains very much on course.”

“There are reasons to believe that this is likely to be an unusually long and strong housing expansion. Demand is very strong because the biggest demographic cohort in history is moving through the household-formation and peak home-buying stages of its life cycle. Coronavirus-related preference changes have also sharply boosted home buying demand. At the same time, supply is unusually tight, with available homes for sale at record-low levels. Double-digit price gains are rationing the supply.”

Bottom Line

If you’re concerned about making the decision to buy or sell right now, let’s connect to discuss what’s happening in our local market.

There’s no doubt that 2021 is the year of the seller when it comes to the housing market. If you’re a homeowner thinking of moving to better suit your changing needs, now is the perfect time to do so. Low mortgage rates are in your favor when you’re ready to purchase your dream home, and high buyer demand may give you the leverage you need to negotiate the best contract terms on the sale of your house. Here’s a look at what’s driving this sellers’ advantage and why there’s so much opportunity for homeowners who are ready to move this season.

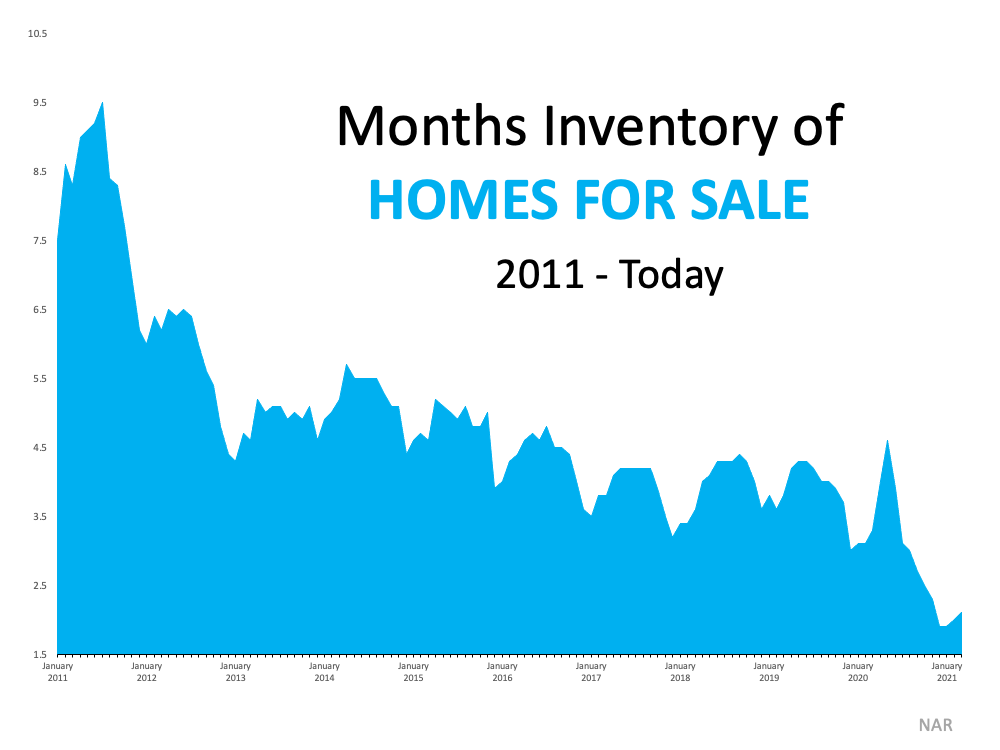

1. Historically Low Inventory

The National Association of Realtors (NAR) explains:

“Total housing inventory at the end of March amounted to 1.07 million units, up 3.9% from February’s inventory . . . Unsold inventory sits at a 2.1-month supplyat the current sales pace, marginally up from February’s 2.0-month supply and down from the 3.3-month supply recorded in March 2020.”

Even with a slight rise in the number of houses for sale this spring, inventory remains near an all-time low (See graph below):High buyer interest is creating a major imbalance between supply and demand, but as the small uptick in inventory shows, sellers are beginning to reenter the market. Selling your house now enables you to take advantage of buyer demand and get the most attention for your house – before more listings come to the market later this year.

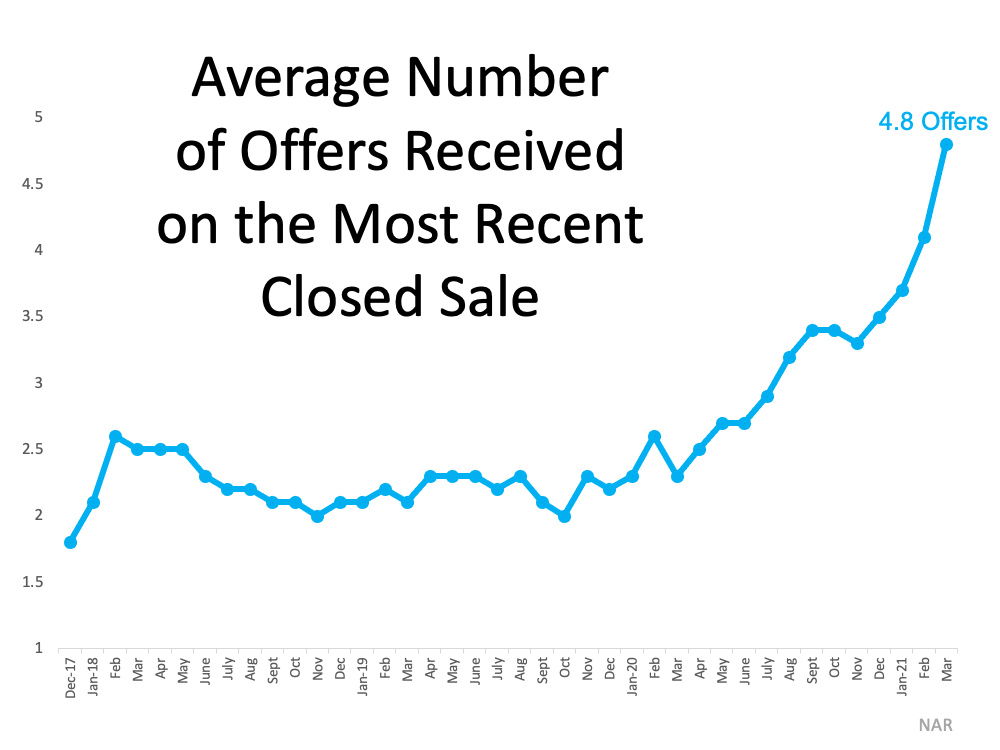

2. Frequent Bidding Wars

As a result of the supply and demand imbalance, homebuyers are entering bidding wars at an accelerating rate. NAR reportsthe average number of bids received on the most recently closed sales is 4.8 offers. This number has doubled since the first quarter of 2020 (See graph below):As buyers face increasingly tough competition while searching for homes to purchase, they’re more likely to be flexible and generous in their negotiations. This gives a seller the opportunity to choose the best buyer for their needs and be selective about things like time to close, contingencies, renovations, and more. Working with your trusted agent is the best way to determine how to navigate the negotiation process when selling your house.

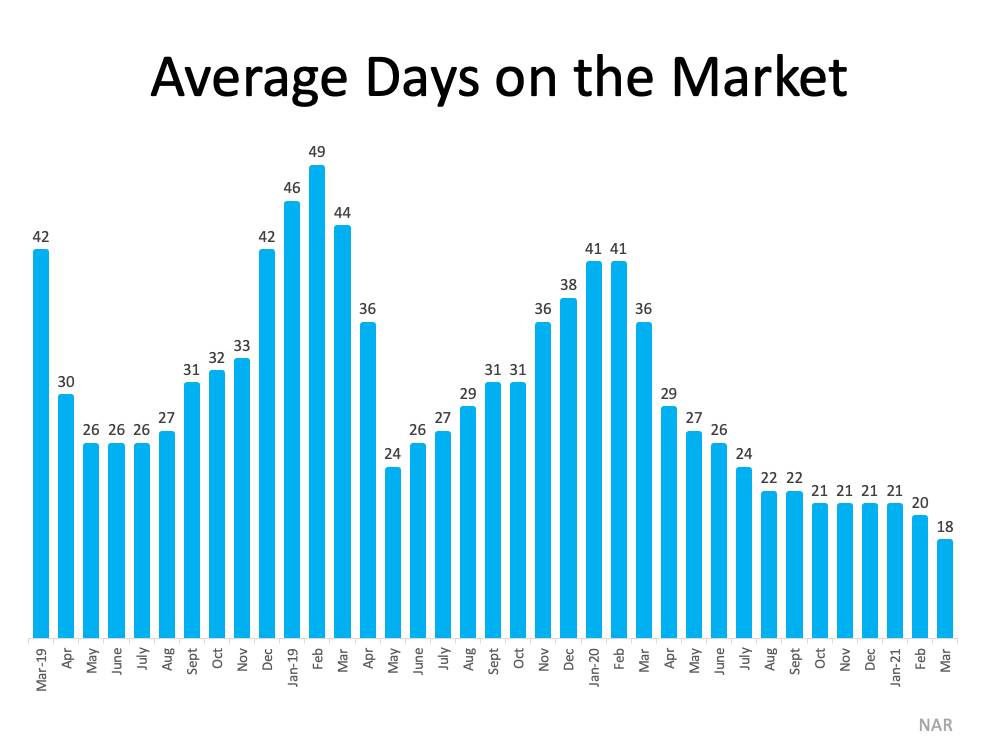

3. Days on the Market

In today’s market, sellers aren’t waiting very long to find a buyer for their house, either. NAR reports:

“Properties typically remained on the market for 18 days in March, down from 20 days in February and from 29 days in March 2020. 83% of the homes sold in March 2021 were on the market for less than a month.”(Seegraph below):

NAR Chief Economist Lawrence Yun explains:

“The sales for March would have been measurably higher, had there been more inventory…Days-on-market are swift, multiple offers are prevalent, and buyer confidence is rising.”

Bottom Line

If you’re thinking about moving, these three graphs clearly show that it’s a great time to sell your house. Let’s connect today so you can learn more about the opportunities in our local area.

Many people are sitting on the fence trying to decide if now’s the time to buy a home. Some are renters who have a strong desire to become homeowners but are unsure if buying right now makes sense. Others may be homeowners who are realizing that their current home no longer fits their changing needs.

To determine if they should buy now or wait another year, they both need to ask two simple questions:

Do I think home values will be higher a year from now?

Do I think mortgage rates will be higher a year from now?

Let’s shed some light on the answers to these questions.

Where will home prices be a year from now?

If you average the most recent projections from the major industry forecasters, the expectation is home prices will increase by 7.7%. Let’s take a house that’s valued today at $325,000 as an example.

If the buyer makes a 10% down payment ($32,500), they’ll end up borrowing $292,500 for their mortgage. Applying the projected rate of home price appreciation, that same house will cost $350,025 next year. With a 10% down payment ($35,003), they’d then have to borrow $315,022.

Therefore, as a result of rising home prices alone, a prospective buyer will have to put down an additional $2,503 and borrow an additional $22,523 just for waiting a year to make their move.

Where will mortgage rates be a year from now?

Today, mortgage rates are hovering around 3%. However, most experts believe they’ll rise as the economy continues to recover. Any increase in the mortgage rate will also increase a purchaser’s cost. Here are the forecasts for the first quarter of 2022 from four major entities:

The projections average out to 3.6% among these four forecasts, a jump up from where they are today.

What does it mean to you if home values and mortgage rates increase?

A buyer will pay a lot more in mortgage payments each month if both of these variables increase. Assuming a buyer purchases a $325,000 home this year with a 30-year fixed-rate loan at 3% after making a 10% down payment, their monthly principal and interest payment would be $1,233.

That same home one year from now could be $350,025, and the mortgage rate could be 3.6% (based on the industry forecasts mentioned above). That monthly principal and interest payment, after putting down 10%, totals $1,432.

The difference in the monthly mortgage payment would be $199. That’s $2,388 more per year and $71,640 over the life of the loan.

Add to that the approximately $25,000 a house with a similar value would build in home equity this year as a result of home price appreciation, and the total net worth increase a purchaser could gain by buying this year is nearly $100,000. That’s a small fortune.

Bottom Line

When asking if they should buy a home, many potential buyers think of the nonfinancial benefits of owning a home. When asking when to buy, the financial benefits make it clear that doing so now is much more advantageous than waiting until next year.

So far this year, mortgage rates continue to hover around 3%, encouraging many hopeful homebuyers to enter the housing market. However, there’s a good chance rates will increase later this year and going into 2022, ultimately making it more expensive to borrow money for a home loan. Here’s a look at what several experts have to say.

“Our long-term view for mortgage rates in 2021 is higher. As the economic outlook strengthens, thanks to progress against coronavirus and vaccines plus a dose of stimulus from the government, this pushes up expectations for economic growth . . . .”

“We forecast that mortgage rates will continue to rise through the end of next year. We estimate the 30-year fixed mortgage rate will average 3.4% in the fourth quarter of 2021, rising to 3.8% in the fourth quarter of 2022.”

The housing market keeps sailing along. The only headwind that could take it off course is the lack of inventory for sale. The National Association of Realtors (NAR) reports that there were 410,000 fewer single-family homes for sale this March than in March of 2020. The key to continued success in the residential housing market is for more listings to come on the market. However, many homeowners are concerned that selling their homes could be challenging for several reasons.

Recently, Homes.com released the findings of a survey that identified these concerns, as well as what it will take for homeowners to feel comfortable selling their houses. Here are the four major homeowner concerns and a quick explanation of what’s actually happening in the housing market today.

1. Homeowners don’t know if they’ll be able to secure their next home before selling.

In negotiations, leverage is the power that one side may have to influence the other side while moving closer to their negotiating position. A party’s leverage is based on the ability to award benefits or eliminate costs on the other side.

In today’s market, buyers have compelling reasons to purchase a home now:

To own a home of their own

To buy before prices continue to appreciate

To secure a mortgage at a historically low rate, while they last

These buyer needs give the seller tremendous leverage. Most already realize this leverage enables the homeowner to sell at a good price. However, this leverage may also be used to negotiate time to find their next home. The homeowner could sell their home to the buyer at today’s price, which will enable the purchaser to take advantage of current mortgage rates. In return, the buyer might lease the house back to the seller for a pre-determined length of time while the seller finds a new home or has one built.

This gives the buyer what they want while also giving the seller what they need. It’s a true win-win negotiation.

2. Homeowners don’t know if their current home will sell for the asking price or top market price.

This is the perfect time to maximize profits while selling a house. NAR just released a study showing that bidding wars are at an all-time high. The study reveals that when comparing the first quarter of last year to the first quarter of this year, the number of offers on homes for sale doubled from an average of 2.4 to 4.8 offers.

Whenever there’s a bidding war, the price of the item for sale escalates. Bloomberg recently reported:

“For the first time ever, the average U.S. home is selling for above its list price.”

If a seller is looking for a top-dollar sale, there’s no better time to sell than right now.

3. Homeowners don’t know if they will get an offer without their home requiring work or updates.

Again, leverage is the greatest strength a seller has in this market. Due to the lack of homes for sale, many buyers are more willing to take on home improvement projects themselves in order to get the home they’re after.

A recent post on whether or not to renovate before selling notes:

“It may be wise to let future homeowners remodel the bathroom or the kitchen to make design decisions that are best for their specific taste and lifestyle. As a seller, your dollars and time might be better spent working on small cosmetic updates, like refreshing some paint and power washing the exterior. Instead of over-investing in your home with upgrades that the buyers may change anyway, work with a real estate professional to determine the key projects that will maximize your listing, without overdoing it.”

If a seller is worried about doing work or updates on their home, they must realize that today’s historically low inventory likely renders these projects less critical to the sale of the house.

4. Homeowners don’t know if they can have a quick closing process.

When speed is important, there are two points sellers should look at:

“Properties typically remained on the market for 18 days in March, down from 20 days in February and from 29 days in March 2020. Eighty-three percent of the homes sold in March 2021 were on the market for less than a month.”

Eighteen days is fast, and it’s a new record. Here are the days the average house is on the market in each state:Regarding the time it will take to close the transaction, all-cash sales accounted for 23% of all home purchase transactions in March. All-cash sales can usually be closed in thirty days.

“Time to close all loans decreased in March. The average time to close a purchase fell to 51 days, down from 53 the month prior.”

If you’re looking for a quick closing process, there’s never been a market in which the two-step process (finding a buyer and closing the deal) has taken less time.

Bottom Line

Selling your house can be daunting, especially in a fast-paced market. However, the fact that we’re in such a strong sellers’ market clearly eliminates many common concerns. Let’s connect today so you can learn more about the opportunities for homeowners who are ready to sell.

Homeownership is a foundational part of the American Dream. As we look back on more than a year of sheltering in our homes, having a place of our own is more important than ever. While financial benefits are always a key aspect of homeownership, today, homeowners rank the nonfinancial and personal benefits with even higher value.

Recently, two national surveys revealed the reasons homeownership is such an important part of life. The top three personal benefits of homeownership noted by respondents in Unison’s 2021 report on The State of the American Homeowner are:

91% – feel secure, stable, or successful owning a home

70% – feel emotionally attached to the homes that have kept them safe over the past year

51% – call homeownership a “key part of their life”

These sentiments were supported by the most recent National Housing Survey from Fannie Mae, which also shows that the top three reasons Americans value homeownership have nothing to do with money. Those surveyed were given a list of feelings and accomplishments that are associated with or impacted by where we live. They were then asked, “To achieve this, are you better off owning or better off renting?” Here are the top three points from the list that respondents said homeownership could help them achieve:

91% – control over what you do with your living space

90% – a sense of privacy and security

89% – a good place for your family to raise your children

Other nonfinancial advantages of homeownership revealed by the survey include feeling engaged in a community, having flexibility in future decisions, and experiencing less stress.

Bottom Line

Financial and nonfinancial benefits are a key component to the value of homeownership, but the nonfinancial side is most valued after a year full of pandemic-driven challenges. Let’s connect today if you’re ready to take the first steps toward becoming a homeowner.

My name is John Bendele and these are words to live by.

“What is the biggest challenge you are facing in life right now and how can I help?”

I believe when you are able to help others in their struggles, it will always bring a since of joy and accomplishment that is like no other. I enjoy bringing opportunities to people in real estate and in life. To be a lifting hand and a beacon of knowledge. It brings me great joy to guide and support others when making exciting and difficult choices. I have been a licensed realtor for over 7 years in Minnesota. Coming from a construction background, I will provide a wealth of knowledge about homes. Knowing homes allows me to a better negotiator with facts and details some may not. I enjoy working with sellers, investors and buyers.

I grew up in Southwest Texas and moved to Minnesota in 2015. I have lived in the White Bear Lake area until making a move over the lake to Willernie, MN where I now reside. I love spending quality time with my teenage boys who nicknamed me “JoJo”. My favorite things to do are being outdoors on or in the water, BBQing (TX style) and going on any adventure.

I want to bring knowledge, growth, excitement and wealth to the clients I encounter through being a realtor. I look forward to assisting you in your amazing journey in real estate.

Thank you,

John A Bendele

Meet Brittany

Brittany is a mama of three kiddos, a wife of a firefighter and added more love to her home with three dogs and two cats. Outside of the fun she has as an agent and her roles at home she enjoys doing any DIY projects she can get her hands on!

Brittany fell in love with the Real Estate gig in 2019. She grew up in Apple Valley, and now owns her childhood home. I guess you could say she is a south metro pro!

You!

Hey! If you’re looking for your next role as an agent let us know! This could be you!

Meet Shea Amundson

Hey, I’m Shea and I love helping people find a beautiful home that sets their soul on fire!

Meet Katie

Katie comes from the busy world of entertainment and being a Traveling Operations Manager. She transitioned to Real Estate back in 2018 and has been hooked ever since! Katie thrives on training, developing new systems, and helping agents grow! Katie joins Voila with the determination to help every agent and client make their dream a reality whether it be building their business or finding that dream home!

When Katie isn’t working, she is a full-time student at Metropolitan University. She enjoys cooking foods from all over the world, traveling, and has a habit of getting a new tattoo wherever she goes. She is huge into animal conservation and spending time with her dog Sawyer who often joins her on travels!

Meet Sarah Beth Lindstrom

Sarah wants to live in a world filled with innovative businesses daring enough to break the mold…monthly auto-shipments of Laffy Taffy’s, and lots and lots of laughter!!!

Having been in the real estate industry since 2005, her go to role has always been supporting her teams in any way that she can! She has gone from Listing and Transaction Management, to Team Manager, and now Director of Support! She is an ‘introverted extrovert’ that finds the, ‘behind the scenes’ with a hint of showing homes – to be a perfect blend.

When she’s not supporting her Voila Family, she is out getting one more rep in at the gym, finding new healthy recipes to attempt (and then trick her teenager into eating somehow), and enjoying quick road trips to…well, anywhere! She also plays on a competitive volleyball team in the winter, sand volleyball in the summer and softball in the spring and fall.

“Two things define you. The patience you have when you have nothing and the attitude when you have everything.”

Meet Jessi Andersen

In June of 2020 Jessi joined team of Voila…and…it’s that easy!

Ha! No really, it did all begin in June. New to this side of Real Estate, Jessi joined in hopes to take her chatty, outgoing self and bring some good of it! Her natural tendencies of networking and love of growth and goals, have been set in direction – expanding Voila!

Where is Jess when she isn’t nurturing the growth of Voila? Adventuring with her family outside in nature. Or perhaps baking up a new recipe while dancing the day away – and of course cheering for her little athletes at home, as well as the MN Vikings/Twins!

“In the end it is not the years in your life that count. It’s the life in your years” ~ Abe Lincoln

Meet Wyatt Lemon

Wyatt is a Real Estate Extraordinaire, and a Loving Husband, and a Lover of Life and a PAW-rent to 3 awesome dogs. Huge believer in the idea that life is what you make of it, so with that being said I guess you could say the glass is half full! Things I enjoy outside of work are Yoga, being a big time Foodie, and spending time with my family. I grew up in Hugo MN and have been a local resident my whole life. I studied Marketing at Century College as well as St. Cloud State University. I got into Real Estate in October of 2018 and have loved every minute of it!

Meet James Andersen

James Andersen is a human being who believes that the best in others is a reflection of the energy we bring.

Magnanimous behavior is the standard not the exception.

10+ years Army Career

5+ years Married

5+ years Father of Calendar Crushers

5+ years Real Estate Career

30+ years Life Experience

Let’s learn and grow together.

Meet Joey Torkildson

You are writing your own story in life! Is what you are doing right now supposed to be in that story? I hope so!

That’s why my goal is to always sign up, get uncomfortable, inspire through doing, shoot, then aim. We don’t have enough time on this planet to stay mundane and there are too many experiences to be doing one thing for too long! It’s all about the short term experiments!

Quick background: 19+ year US Army Master Sergeant vet; 10+ year transformer of lives through ownership (AKA: Realtor) ; 2+ year CEO of an Expansion Team with Hergenrother Realty Group ; Director of Agent Training with that same organization; Self employed for 12+ years; starting in late 2019 CoFounded a new disruptive real estate brokerage, Voila; Contagiously energetic teacher who loves helping people discover they can accomplish anything; Dad of two extremely crazy and loving boys; Husband of an amazingly supportive and ultimate gardener wife.

Let’s be curious explorers together! I love connecting with people and helping them achieve their goals and I’m a firm believer in the fact that you are one introduction away from your entire life changing!

Two quotes I live by: Amazing things rarely happen in your comfort zone and only those who attempt the absurd achieve the impossible!

The article goes on to say:

The article goes on to say: