One of the biggest hurdles homebuyers face is saving for a down payment. As you’re budgeting and planning for your home purchase, you’ll want to understand how much you’ll need to put down and how long it will take you to get there. The process may actually move faster than you think.

Using data from the U.S. Department of Housing and Urban Development (HUD) and Apartment List, we can estimate how long it might take someone earning the median income and paying the median rent to save up for a down payment on a median-priced home. Since saving for a down payment can be a great time to practice budgeting for housing costs, this estimate also uses the concept that a household should not pay more than 28% of their total income on monthly housing expenses.

According to the data, the national average for the time it would take to save for a 10% down payment is right around two and a half years (2.53). Residents in Iowa can save for a down payment the fastest, doing so in just over one year (1.31). The map below illustrates this time (in years) for each state:

What if you only need to save 3%?

What if you’re able to take advantage of one of the 3% down payment programs available? It’s a common misconception that you need a 20% down payment to buy a home, but there are actually more affordable options and down payment assistance programs available, especially for first-time buyers. The reality is, saving for a 3% down payment may not take several years. In fact, it could take less than a year in most states, as shown in the map below:

Bottom Line

Wherever you are in the process of saving for a down payment, you may be closer to your dream home than you think. Let’s connect to explore the down payment options available in our area and how they support your plans.

Since the birth of our nation, homeownership has always been considered a major piece of the American Dream. As Frederick Peters reports in Forbes:

“The idea of a place of one’s own drives the American story. We became a nation out of a desire to slip the bonds of Europe, which was still in many respects a collection of feudal societies. Old rich families, or the church, owned all the land and, with few exceptions, everyone else was a tenant. The magic of America lay not only in its sense of opportunity, but also in the belief that life could in every way be shaped by the individual. People traveled here not just for religious freedom, but because in America anything seemed possible.”

Additionally, a research paper released just prior to the shelter-in-place orders issued last year concludes:

“Homeownership is undeniably the cornerstone of the American Dream, and is inseparable from our national ethos that, through hard work, every American should have opportunities for prosperity and success. It is the stability and wealth creation that homeownership provides that represents the primary mechanism through which many American families are able to achieve upward socioeconomic mobility and greater opportunities for their children.”

Has the past year changed the American view on homeownership?

Definitely not. A survey of prospective homebuyers released by realtor.com last week reveals that becoming a homeowner is still the main reason this year’s first-time homebuyers want to purchase a home. When asked why they want to buy, three of the top four responses center on the financial benefits of owning a home. The top four reasons for buying are:

59% – “I want to be a homeowner”

33% – “I want to live in a space that I can invest in improving”

31% – “I need more space”

22% – “I want to build equity”

Millennials believe most strongly in homeownership.

The survey also reports that 62% of millennials say a desire to be a homeowner is the main reason they’re buying a home. This contradicts the thinking of some experts who had believed millennials were going to be the first “renter generation” in our nation’s history.

While reporting on the survey, George Ratiu, Senior Economist at realtor.com, said:

“Americans, even millennials who many thought would never buy, have a strong preference for homeownership for the same reasons many generations before them have — to invest in a place of their own and in their communities, and to build a solid financial foundation for themselves and their families.”

Odeta Kushi, Deputy Chief Economist for First American, also addresses millennial homeownership:

“Millennials have delayed marriage and having children in favor of investing in education, pushing marriage and family formation to their early-to-mid thirties, compared with previous generations, who primarily made these lifestyle choices in their twenties…Delayed lifestyle choices delay the desire for homeownership.”

Kushi goes on to explain:

“As more millennials get married and form families, millennials remain poised to transform the housing market. In fact, the housing market is already experiencing the earliest gusts of the tailwind.”

Bottom Line

As it always has been and very likely always will be, homeownership continues to be a major component in every generation’s pursuit of the American Dream.

For generations, the homebuying process never really changed. The seller would try to estimate the market value of the home and tack on a little extra to give themselves some negotiating room. That figure would become the listing price of the house. Buyers would then try to determine how much less than the full price they could offer and still get the home. The asking price was generally the ceiling of the negotiation. The actual sales price would almost always be somewhat lower than the list price. It was unthinkable to pay more than what the seller was asking.

Today is different.

The record-low supply of homes for sale coupled with very strong buyer demand is leading to a rise in bidding wars on many homes. Because of this, homes today often sell for more than the list price. In some cases, they sell for a lot more.

According to the Home Buyers and Sellers Generational Trendsreport just released by the National Association of Realtors (NAR), 45% of buyers paid full price or more.

You may need to change the way you look at the asking price of a home.

In this market, you likely can’t shop for a home with the old-school mentality of refusing to pay full price or more for a house.

Because of the shortage of inventory of houses for sale, many homes are actually being offered in an auction-like atmosphere in which the highest bidder wins the home. In an actual auction, the seller of an item agrees to take the highest bid, and many sellers set a reserve price on the item they’re selling. A reserve price is the minimum amount a seller will accept as the winning bid.

When navigating a competitive housing market, think of the list price of the house as the reserve price at an auction. It’s the minimum the seller will accept in many cases. Today, the asking price is often becoming the floor of the negotiation rather than the ceiling. Therefore, if you really love a home, know that it may ultimately sell for more than the sellers are asking. So, as you’re navigating the homebuying process, make sure you know your budget, know what you can afford, and work with a trusted advisor who can help you make all the right moves as you buy a home.

Bottom Line

Someone who’s more familiar with the housing market of the past than that of today may think offering more for a home than the listing price is foolish. However, frequent and competitive bidding wars are creating an auction-like atmosphere in many real estate transactions. Let’s connect so you have the best advice on how to make a competitive offer on a home in our local market.

According to data from the most recent Origination Insight Report by Ellie Mae, the average FICO® score on closed loans reached 753 in February. As lending standards have tightened recently, many are concerned over whether or not their credit score is strong enough to qualify for a mortgage. While stricter lending standards could be a challenge for some, many buyers may be surprised by the options that are still available for borrowers with lower credit scores.

The fact that the average American has seen their credit score go up in recent years is a great sign of financial health. As someone’s score rises, they’re building toward a stronger financial future. As more Americans with strong credit enter the housing market, we see a natural increase in the FICO® score distribution of closed loans, as shown in the graph below:If your credit score is below 750, it’s easy to see this data and fear that you may not be able to qualify for a mortgage. However, that’s not always the case. While the majority of borrowers right now do have a score above 750, there’s more to qualifying for a mortgage than just the credit score, and there are still options that allow people with lower credit scores to buy their dream home. Here’s what Experian, a global leader in consumer and business credit reporting, says:

Federal Housing Administration (FHA) loans:“With a 3.5% down payment, homebuyers may be able to get an FHA loan with a 580 credit score or higher. If you can manage a 10% down payment, though, that minimum goes as low as 500.”

Conventional loans:“The most popular loan type typically comes with a 620 minimum credit score.”

S. Department of Agriculture (USDA) loans:“In general, lenders require a minimum credit score of 640 for a USDA loan, though some may go as low as 580.”

S. Department of Veterans Affairs (VA) loans:“VA loans don’t technically have a minimum credit score, but lenders will typically require between 580 and 620.”

There’s no doubt a higher credit score will give you more options and better terms when applying for a mortgage, especially when lending is tight like it is right now. When planning to buy a home, speaking to an expert about steps you can take to improve your credit score is essential so you’re in the best position possible. However, don’t rule yourself out if your score is less than perfect – today’s market is still full of opportunity.

Bottom Line

Don’t let assumptions about whether your credit score is strong enough put a premature end to your homeownership goals. Let’s connect today to discuss the options that are best for you.

Last Thursday, Freddie Macannounced that their 30-year fixed mortgage rate was over 3% (3.02%) for the first time since last July. That news dominated real estate headlines that day and the next. Articles talked about the “negative impact” it may have on the housing market. However, we should realize two things:

1. The bump-up in rate should not have surprised anyone. Many had already projected that rates would rise slightly as we proceeded through the year.

2. Freddie Mac’s comments about the rate increase were not alarming:

“The rise in mortgage rates over the next couple of months is likely to be more muted in comparison to the last few weeks, and we expect a strong spring sales season.”

A “muted” rise in rates will not sink the real estate market, and most experts agree that it will be “a strong spring sales season.”

What does this mean for you?

Obviously, any buyer would rather mortgage rates not rise at all, as any upward movement increases their monthly mortgage payment. However, let’s put a 3.02% rate into perspective. Here are the Freddie Mac annual mortgage rates for the last five years:

2016: 3.65%

2017: 3.99%

2018: 4.54%

2019: 3.94%

2020: 3.11%

Though 3.02% is not as great as the sub-3% rates we saw over the previous seven weeks, it’s still very close to the all-time low (2.66% in December 2020).

And, if we expand our look at mortgage rates to consider the last 50 years, we can see that today’s rate is truly outstanding. Here are the rates over the last five decades:

1970s: 8.86%

1980s: 12.7%

1990s: 8.12%

2000s: 6.29%

2010s: 4.09%

Being upset that you missed the “best mortgage rate ever” is understandable. However, don’t throw the baby out with the bathwater. Buying now still makes more sense than waiting, especially if rates continue to bump up this year.

Bottom Line

It’s true that you may not get the same rate you would have five weeks ago. However, you will get a better rate than what was possible at almost any other point in history. Let’s connect today so you can lock in a great rate while they stay this low.

Whether you’re buying your first home or selling your current house, if your needs are changing and you think you need to move, the decision can be complicated. You may have to take personal or professional considerations into account, and only you can judge what impact those factors should have on your desire to move.

However, there’s one category that provides a simple answer. When deciding to buy now or wait until next year, the financial aspect of the purchase is easy to evaluate. You just need to ask yourself two questions:

Do I think home values will be higher a year from now?

Do I think mortgage rates will be higher a year from now?

From a purely financial standpoint, if the answer is ‘yes’ to eitherquestion, you should strongly consider buying now. If the answer to both questions is ‘yes,’ you should definitely buy now.

Nobody can guarantee what home values or mortgage rates will be by the end of this year. The experts, however, seem certain the answer to both questions above is a resounding ‘yes.’ Mortgage rates are expected to rise and home values are expected to appreciate rather nicely.

What does this mean to you?

Let’s look at how waiting would impact your financial situation. Here are the assumptions made for this example:

The experts are right – mortgage rates will be 3.18% at the end of the year

The experts are right – home values will appreciate by 5.9%

You want to buy a home valued at $350,000 today

You decide on a 10% down payment

Here’s the financial impact of waiting:

You pay an extra $20,650 for the house

You need an additional $2,065 for a down payment

You pay an extra $116/month in your mortgage payment ($1,392 additional per year)

You don’t gain the $20,650 increase in wealth through equity build-up

Bottom Line

There are many things to consider when buying a home. However, from a purely financial aspect, if you find a home that meets your needs, buying now makes much more sense than buying next year.

If you’re thinking of buying a home this year, you may be wondering how much money you need to come up with for your down payment. Many people may think it’s 20% of the loan to secure a mortgage. While there are plenty of lower down payment options available for qualified buyers who don’t want to put 20% down, it’s important to understand how a larger down payment can have great benefits too.

The truth is, there are many programs available that allow you to put down as little as 3.5%, which can be a huge benefit to those who want to purchase a home sooner rather than later. Those who have served our country may also qualify for a Veterans Affairs Home Loan (VA) and may not need a down payment. These programs have really cut down the savings time for many potential buyers, enabling them to start building family wealth sooner.

Here are four reasons why putting 20% down is a good plan if you can afford it.

1. Your interest rate may be lower.

A 20% down payment vs. a 3-5% down payment shows your lender you’re more financially stable and not a large credit risk. The more confident your lender is in your credit score and your ability to pay your loan, the lower the mortgage interest rate they’ll likely be willing to give you.

2. You’ll end up paying less for your home.

The larger your down payment, the smaller your loan amount will be for your mortgage. If you’re able to pay 20% of the cost of your new home at the start of the transaction, you’ll only pay interest on the remaining 80%. If you put down 5%, the additional 15% will be added to your loan and will accrue interest over time. This will end up costing you more over the lifetime of your home loan.

3. Your offer will stand out in a competitive market.

In a market where many buyers are competing for the same home, sellers like to see offers come in with 20% or larger down payments. The seller gains the same confidence as the lender in this scenario. You are seen as a stronger buyer with financing that’s more likely to be approved. Therefore, the deal will be more likely to go through.

4. You won’t have to pay Private Mortgage Insurance (PMI)

“PMI is an insurance policy that protects the lender if you are unable to pay your mortgage. It’s a monthly fee, rolled into your mortgage payment, that is required for all conforming, conventional loans that have down payments less than 20%. Once you’ve built equity of 20% in your home, you can cancel your PMI and remove that expense from your mortgage payment.”

As mentioned earlier, when you put down less than 20% when buying a home, your lender will see your loan as having more risk. PMI helps them recover their investment in you if you’re unable to pay your loan. This insurance isn’t required if you’re able to put down 20% or more.

Many times, home sellers looking to move up to a larger or more expensive home are able to take the equity they earn from the sale of their house to put down 20% on their next home. With the equity homeowners have today, it creates a great opportunity to put those savings toward a 20% or greater down payment on a new home.

If you’re looking to buy your first home, you’ll want to consider the benefits of 20% down versus a smaller down payment option.

Bottom Line

If you’re thinking of buying a home and are already saving for your down payment, let’s connect to discuss what fits best with your long-term plans.

If you’re looking for a home to purchase right now and having trouble finding one, you’re not alone. At a time like this when there are so few houses for sale, it’s normal to wonder if you’ll actually find one to buy. According to the National Association of Realtors (NAR), across the country, inventory of available homes for sale is at an all-time low – the lowest point recorded since NAR began tracking this metric in 1982. There are, however, more homes expected to hit the market later this year. Let’s break down the three key places they’ll likely come from as 2021 continues on.

1. Homeowners Who Didn’t Sell Last Year

In 2020, many sellers decided to pause their moving plans for a number of different reasons. From health concerns about the pandemic to financial uncertainty, plenty of homeowners decided not to move last year.

Now that vaccines are being distributed and there’s a light at the end of the COVID-19 tunnel, it should bring some peace of mind to many potential sellers. As Danielle Hale, Chief Economist at realtor.com, notes:

“Fortunately for would-be homebuyers, we expect sellers to return to the market as we see improvement in the economy and progress against the coronavirus.”

Many of the homeowners who decided not to sell in 2020 will enter the market later this year as they begin to feel more comfortable showing their house in person, understanding their financial situation, and simply having more security in life.

2. More New Homes Will Be Built

Last year was a strong year for home builders, and according to the National Association of Home Builders (NAHB), 2021 is expected to be even better:

“For 2021, NAHB expects ongoing growth for single-family construction. It will be the first year for which total single-family construction will exceed 1 million starts since the Great Recession.”

With more houses being built in many markets around the country, homeowners looking for new houses that meet their changing needs will be able to move into their dream homes. When they sell their current houses, this will create opportunities for those looking to find a home that’s already built to do so. It sets a simple chain reaction in motion for hopeful buyers.

3. Those Impacted Financially by the Economic Crisis

Many experts don’t anticipate a large wave of foreclosures coming to the market, given the forbearance options afforded to current homeowners throughout the pandemic. Some homeowners who have been impacted economically will, however, need to move this year. There are also homeowners who didn’t take advantage of the forbearance option or were already in a foreclosure situation before the pandemic began. In those cases, homeowners may decide to sell their houses instead of going into the foreclosure process, especially given the equity in homes today. Lawrence Yun, Chief Economist at NAR, explains:

“Given the huge price gains recently, I don’t think many homes will have to go to foreclosure…I think homes will just be sold, and there will be cash left over for the seller, even in a distressed situation. So that’s a bit of a silver lining in that we don’t expect a massive sale of distressed properties.”

As we can see, it looks like we’re going to have an increase in the number of homes for sale in 2021. With fears of the pandemic starting to ease, new homes being built, and more listings coming to the market prior to foreclosure, there’s hope if you’re planning to buy this year. And if you’re thinking of selling and making a move, doing so while demand for your house is high might create an outstanding move-up option for you.

Bottom Line

Housing demand is high and supply is low, so if you’re thinking of moving, it’s a great time to do so. There are likely many buyers who are looking for a home just like yours, and there are options coming for you to find a new house too. Let’s connect today to see how you can benefit from the opportunities available in our local market.

We’re currently experiencing historically low mortgage rates. Over the last fifty years, the average on a Freddie Mac 30-year fixed-rate mortgage has been 7.76%. Today, that rate is 2.81%. Flocks of homebuyers have been taking advantage of these remarkably low rates over the last twelve months. However, there’s no guarantee rates will remain this low much longer.

Whenever we try to forecast mortgage rates, we should consider the advice of Mark Fleming, Chief Economist at First American:

“You know, the fallacy of economic forecasting is don’t ever try and forecast interest rates and/or, more specifically, if you’re a real estate economist mortgage rates, because you will always invariably be wrong.”

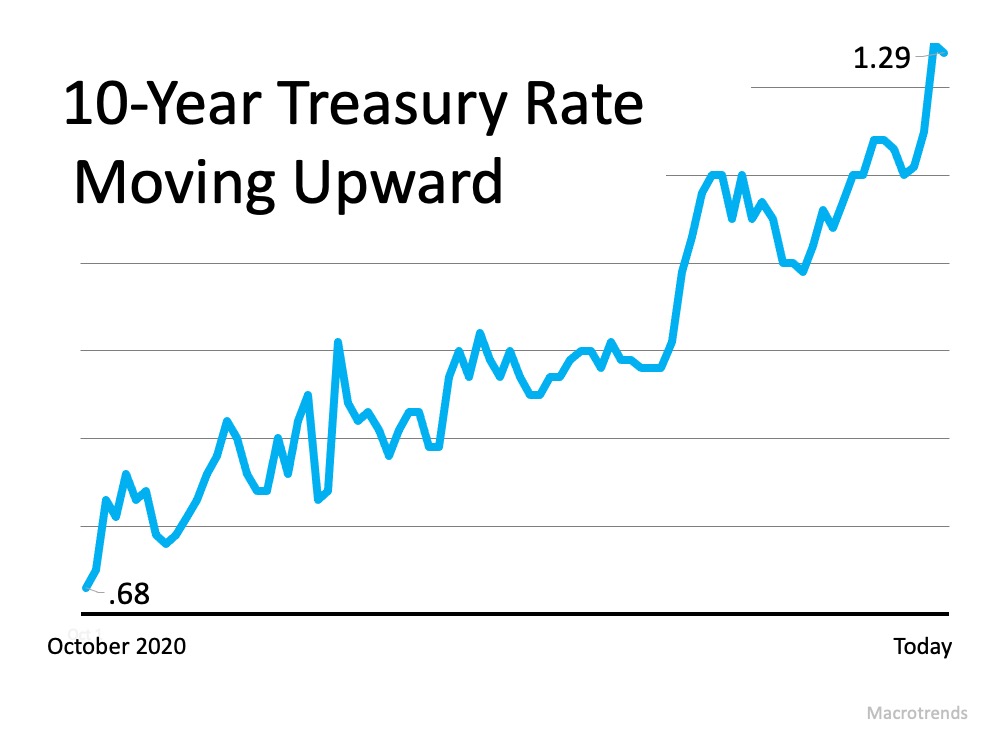

Many things impact mortgage rates. The economy, inflation, and Fed policy, just to name a few. That makes forecasting rates difficult. However, there’s one metric that has held up over the last fifty years – the relationship between mortgage rates and the 10-year treasury rate. Here’s a graph detailing this relationship since Freddie Mac started keeping mortgage rate records in 1972:There’s no denying the close relationship between the two. Over the last five decades, there’s been an average 1.7-point spread between these two rates. It’s this long-term relationship that has some forecasters projecting an increase in mortgage rates as we move throughout the year. This is based on the recent surge in the 10-year treasury rate shown here:The spread between the two is now 1.53, indicating mortgage rates could rise. Actually, a bump-up in rate has already begun. As Joel Kan, Associate VP of Economic Forecasting for the Mortgage Bankers Association, reveals:

“Expectations of faster economic growth and inflation continue to push Treasury yields & mortgage rates higher. Since hitting a survey low in December, the 30-year fixed rate has slowly risen, & last week climbed to its highest level since Nov 2020.”

How high might they go in 2021?

No one knows for sure. Sam Khater, Chief Economist for Freddie Mac, recently suggested:

“While there are multiple temporary factors driving up rates, the underlying economic fundamentals point to rates remaining in the low 3% range for the year.”

What does this mean for you?

Whether you’re a first-time buyer or you’ve purchased a home before, even an increase of half a point in mortgage rate (2.81 to 3.31%) makes a big difference. On a $300,000 mortgage, that difference (including principal and interest) is $82 a month, $984 a year, or a total of $29,520 over the life of the home loan.

Bottom Line

Based on the 50-year symbiotic relationship between treasury rates and mortgage rates, it appears mortgage rates could be headed up this year. It may make sense to buy now rather than wait.

Headlines matter. Right now, it’s hard to read about real estate without seeing a headline that suggests homes have become unaffordable for most Americans. In reality, there’s hard evidence that shows how owning a home is more affordable than renting in most parts of the country, as record-low interest rates are keeping monthly mortgage payments about 23% lower than the typical payment of 20 years ago. Despite the facts, misleading headlines persist, and they impact how hopeful homebuyers perceive the market.

In a recent survey by realtor.com, home shoppers indicated they were surprised by what they could actually afford when buying their first home. In fact, 47% discovered their budget was larger than they expected. George Ratiu, Senior Economist at realtor.com, explains:

“For first-time buyers, especially, the drop in the 30-year mortgage rate…has provided unexpected leverage. Lower rates allowed many buyers to stretch and buy more expensive homes while keeping their monthly budget the same.”

So why do these negative headlines that cast doubt on affordability continue to exist?

Most analysts only look at two of the three elements that make up the affordability equation: price and income. It’s true that incomes haven’t kept up with the price of houses. However, affordability is about the cost of the home, not just the price. For that reason, mortgage rates, the third element of the affordability equation, are important to consider.

For example, here’s the typical mortgage payment for assorted dates going back to 2000, as calculated by CoreLogic:Outside of the housing crash (when short sales and foreclosures drove prices down), it’s more affordable to buy a home today when you consider all three elements of the affordability equation: price, income,and mortgage rate.

Bottom Line

Whether you’re a first-time buyer or a move-up buyer, don’t let the headlines scare you away from your dream of homeownership. Instead, connect with mortgage and real estate professionals to determine what you can afford and what’s available at that price. Like almost half of the buyers in the survey, you may be pleasantly surprised.

My name is John Bendele and these are words to live by.

“What is the biggest challenge you are facing in life right now and how can I help?”

I believe when you are able to help others in their struggles, it will always bring a since of joy and accomplishment that is like no other. I enjoy bringing opportunities to people in real estate and in life. To be a lifting hand and a beacon of knowledge. It brings me great joy to guide and support others when making exciting and difficult choices. I have been a licensed realtor for over 7 years in Minnesota. Coming from a construction background, I will provide a wealth of knowledge about homes. Knowing homes allows me to a better negotiator with facts and details some may not. I enjoy working with sellers, investors and buyers.

I grew up in Southwest Texas and moved to Minnesota in 2015. I have lived in the White Bear Lake area until making a move over the lake to Willernie, MN where I now reside. I love spending quality time with my teenage boys who nicknamed me “JoJo”. My favorite things to do are being outdoors on or in the water, BBQing (TX style) and going on any adventure.

I want to bring knowledge, growth, excitement and wealth to the clients I encounter through being a realtor. I look forward to assisting you in your amazing journey in real estate.

Thank you,

John A Bendele

Meet Brittany

Brittany is a mama of three kiddos, a wife of a firefighter and added more love to her home with three dogs and two cats. Outside of the fun she has as an agent and her roles at home she enjoys doing any DIY projects she can get her hands on!

Brittany fell in love with the Real Estate gig in 2019. She grew up in Apple Valley, and now owns her childhood home. I guess you could say she is a south metro pro!

You!

Hey! If you’re looking for your next role as an agent let us know! This could be you!

Meet Shea Amundson

Hey, I’m Shea and I love helping people find a beautiful home that sets their soul on fire!

Meet Katie

Katie comes from the busy world of entertainment and being a Traveling Operations Manager. She transitioned to Real Estate back in 2018 and has been hooked ever since! Katie thrives on training, developing new systems, and helping agents grow! Katie joins Voila with the determination to help every agent and client make their dream a reality whether it be building their business or finding that dream home!

When Katie isn’t working, she is a full-time student at Metropolitan University. She enjoys cooking foods from all over the world, traveling, and has a habit of getting a new tattoo wherever she goes. She is huge into animal conservation and spending time with her dog Sawyer who often joins her on travels!

Meet Sarah Beth Lindstrom

Sarah wants to live in a world filled with innovative businesses daring enough to break the mold…monthly auto-shipments of Laffy Taffy’s, and lots and lots of laughter!!!

Having been in the real estate industry since 2005, her go to role has always been supporting her teams in any way that she can! She has gone from Listing and Transaction Management, to Team Manager, and now Director of Support! She is an ‘introverted extrovert’ that finds the, ‘behind the scenes’ with a hint of showing homes – to be a perfect blend.

When she’s not supporting her Voila Family, she is out getting one more rep in at the gym, finding new healthy recipes to attempt (and then trick her teenager into eating somehow), and enjoying quick road trips to…well, anywhere! She also plays on a competitive volleyball team in the winter, sand volleyball in the summer and softball in the spring and fall.

“Two things define you. The patience you have when you have nothing and the attitude when you have everything.”

Meet Jessi Andersen

In June of 2020 Jessi joined team of Voila…and…it’s that easy!

Ha! No really, it did all begin in June. New to this side of Real Estate, Jessi joined in hopes to take her chatty, outgoing self and bring some good of it! Her natural tendencies of networking and love of growth and goals, have been set in direction – expanding Voila!

Where is Jess when she isn’t nurturing the growth of Voila? Adventuring with her family outside in nature. Or perhaps baking up a new recipe while dancing the day away – and of course cheering for her little athletes at home, as well as the MN Vikings/Twins!

“In the end it is not the years in your life that count. It’s the life in your years” ~ Abe Lincoln

Meet Wyatt Lemon

Wyatt is a Real Estate Extraordinaire, and a Loving Husband, and a Lover of Life and a PAW-rent to 3 awesome dogs. Huge believer in the idea that life is what you make of it, so with that being said I guess you could say the glass is half full! Things I enjoy outside of work are Yoga, being a big time Foodie, and spending time with my family. I grew up in Hugo MN and have been a local resident my whole life. I studied Marketing at Century College as well as St. Cloud State University. I got into Real Estate in October of 2018 and have loved every minute of it!

Meet James Andersen

James Andersen is a human being who believes that the best in others is a reflection of the energy we bring.

Magnanimous behavior is the standard not the exception.

10+ years Army Career

5+ years Married

5+ years Father of Calendar Crushers

5+ years Real Estate Career

30+ years Life Experience

Let’s learn and grow together.

Meet Joey Torkildson

You are writing your own story in life! Is what you are doing right now supposed to be in that story? I hope so!

That’s why my goal is to always sign up, get uncomfortable, inspire through doing, shoot, then aim. We don’t have enough time on this planet to stay mundane and there are too many experiences to be doing one thing for too long! It’s all about the short term experiments!

Quick background: 19+ year US Army Master Sergeant vet; 10+ year transformer of lives through ownership (AKA: Realtor) ; 2+ year CEO of an Expansion Team with Hergenrother Realty Group ; Director of Agent Training with that same organization; Self employed for 12+ years; starting in late 2019 CoFounded a new disruptive real estate brokerage, Voila; Contagiously energetic teacher who loves helping people discover they can accomplish anything; Dad of two extremely crazy and loving boys; Husband of an amazingly supportive and ultimate gardener wife.

Let’s be curious explorers together! I love connecting with people and helping them achieve their goals and I’m a firm believer in the fact that you are one introduction away from your entire life changing!

Two quotes I live by: Amazing things rarely happen in your comfort zone and only those who attempt the absurd achieve the impossible!