Don’t be impressed by the headlines reporting year-over-year housing numbers for the next several months (data covering March, April, May, and June). The data will most likely show eye-popping one-year increases.

While the year-over-year jumps will certainly be striking, consumers should take these numbers with a grain of salt, as the situation highlights a short-term quirk in the reporting of this data. Essentially, the increases will reflect a combination of two things: sharply lower housing numbers during last year’s virus-related market collapse and the subsequent strong rebound. This will result in what will appear to be unbelievable growth.

Let’s use single-family home sales as an example:As the graph reveals, last spring’s buying market was anything but typical. Instead of sales increasing, they fell sharply as a result of stay-at-home orders that virtually shut the real estate industry down.

This spring’s real estate market will bounce back with more normal seasonal sales increases. The percentage increase in sales will be astronomical – not because sales have skyrocketed, but instead because they will be compared to last year’s low numbers.

Bottom Line

There are likely to be some sensational headlines about real estate over the coming months. However, don’t be fooled. The actual story is that the real estate market is finally back to normal.

This year, mortgage rates have started to slowly climb above recent record-breaking lows. Many homeowners planning to move may feel like they’ve missed the chance to score a great rate on their next mortgage. In reality, there’s still time to secure a rate far below the historic norm. Here’s why.

After creeping up for seven consecutive weeks, average mortgage rates have dropped more recently (See graph below). With rates taking a slight dip over the past two weeks at the same time the inventory of houses for sale is so low, homeowners today are sitting in the optimal seat to sell. What’s the advantage of selling your house now? Securing a low mortgage rate on your next home.To take advantage of today’s real estate market, experts are encouraging homeowners to act now before interest rates climb. Danielle Hale, Chief Economist at realtor.com, explains:

“…mortgage rates slid for a second week … but we don’t expect rates to stay at this level for too long.”

Hale continues to say:

“For sellers, getting in early optimizes odds of a quick sale at a good price before there’s too much competition, but that means acting now … In this environment, sellers probably really can’t go wrong, and that’s especially true in the nation’s hottest housing markets where homes are selling quickly and getting the greatest number of viewers online.”

Most experts agree that rates will continue to trend upward. Sam Khater, Chief Economist at Freddie Mac, states:

“Despite the pause in mortgage rates recently, we expect them to increase modestly for the remainder of this year.”

In addition, Freddie Mac recently released their Quarterly Forecast, which notes:

“We forecast that mortgage rates will continue to rise through the end of next year. We estimate the 30-year fixed mortgage rate will average 3.4% in the fourth quarter of 2021, rising to 3.8% in the fourth quarter of 2022.” (See graph below):

While buyers everywhere want to secure the lowest rate possible, it’s important to remember that today’s rates are still much lower than the historic norm. Odeta Kushi, Deputy Chief Economist at First American, emphasizes:

“While mortgage rates have trended up in recent months, they are still historically low, so relative to one year ago, housing actually is still more affordable and that’s really thanks to this low mortgage rate environment we find ourselves in.”

Bottom Line

If you’re thinking of moving, don’t miss the opportunity to score a great rate on your next home mortgage. Let’s connect today so you can get your house ready to sell and find your dream home while mortgage rates are still low.

The financial benefits of buying a home as compared to renting one are always up for debate. However, one element of the equation is often ignored – the ability to build wealth as a homeowner.

Most experts are calling for home prices to continue appreciating over the next several years. The most recent Home Price Expectation Survey, a survey of over one hundred economists, real estate experts, and investment and market strategists, expects home appreciation to increase as follows:

2021: 6%

2022: 4.5%

2023: 4%

2024: 3.6%

2025: 3.5%

Using their annual projections, the graph below shows the equity build-up a purchaser could earn, using a $350,000 home as an example:A homeowner could increase their net worth by over $80,000 in five years. That’s an average of $16,000 annually. That number should be in any equation determining the financial benefits of owning a home compared to renting.

Bottom Line

Homeowners are going to make a substantial amount of money in home equity over the next five years. If you’re ready to buy a home, let’s connect so you can enjoy this great benefit as well.

One of the biggest hurdles homebuyers face is saving for a down payment. As you’re budgeting and planning for your home purchase, you’ll want to understand how much you’ll need to put down and how long it will take you to get there. The process may actually move faster than you think.

Using data from the U.S. Department of Housing and Urban Development (HUD) and Apartment List, we can estimate how long it might take someone earning the median income and paying the median rent to save up for a down payment on a median-priced home. Since saving for a down payment can be a great time to practice budgeting for housing costs, this estimate also uses the concept that a household should not pay more than 28% of their total income on monthly housing expenses.

According to the data, the national average for the time it would take to save for a 10% down payment is right around two and a half years (2.53). Residents in Iowa can save for a down payment the fastest, doing so in just over one year (1.31). The map below illustrates this time (in years) for each state:

What if you only need to save 3%?

What if you’re able to take advantage of one of the 3% down payment programs available? It’s a common misconception that you need a 20% down payment to buy a home, but there are actually more affordable options and down payment assistance programs available, especially for first-time buyers. The reality is, saving for a 3% down payment may not take several years. In fact, it could take less than a year in most states, as shown in the map below:

Bottom Line

Wherever you are in the process of saving for a down payment, you may be closer to your dream home than you think. Let’s connect to explore the down payment options available in our area and how they support your plans.

A recent Survey of Consumer Finances study released by the Federal Reserve reveals the net worth of homeowners is forty times greater than that of renters. If you’re wondering if homeownership is a good investment, the study clearly answers that question, and the answer is yes.

Do Americans believe a home is a better investment than stocks?

In a post on the Liberty Street Economics blog, the Federal Reserve Bank of New York notes that 93.3% of Americans believe buying a home is definitely or probably a better investment than buying stocks.

Here’s how the results break down:The survey also shows a wide range of reasons why Americans feel that way (respondents were able to pick more than one answer):

Bottom Line

The data show how strongly Americans believe in homeownership as an investment. That belief is warranted. The Liberty Street Economics blog put it best by saying:

“Housing represents the largest asset owned by most households and is a major means of wealth accumulation, particularly for the middle class.”

Over the past year, we’ve had plenty of opportunities to reflect on what we consider most important in our lives. The place we call home is one of the biggest things many of us are reevaluating. George Ratiu, Senior Economist at realtor.com, shares:

“The very nature of the pandemic, through the health implications, social distancing, and need to isolate, has really brought a central focus on the importance of home for most Americans…In a sense, it has elevated real estate markets as a centerpiece of our lives.”

For some, this has spurred an interest in making a move to a home that better suits our changing needs. In a recent study on today’s homebuyer preferences, the National Association of Home Builders (NAHB) states:

“When asked more specifically how the pandemic may have impacted their preference for home size…21% or about 1 out of every 5 buyers, do want a larger home now as a direct result of the health crisis, while another segment – 12% – would prefer a smaller one instead.”

While you might expect more time at home to lead to a need for more space, it’s interesting that a significant portion of homeowners actually want less. For those who own larger homes right now and have a desire to move, today’s housing market is full of opportunities. Danielle Hale, Chief Economist at realtor.com, explains:

“In a real estate market that is tipped in the favor of sellers, boomers and older homeowners are really the ones holding the cards…Those who are selling homes can use the profits to help them buy new ones.”

As a homeowner today, you likely have equity that can be put toward the purchase of your next home. With the equity growth homes have seen over the past year, you may have more than you think, which can help significantly as you make a move into your next home. According to a report from the National Association of Realtors (NAR):

“Home sellers cited that they sold their homes for a median of $66,000 more than they purchased it. Sellers 22 to 30 years gained the least at $33,400 in equity compared to sellers 66 to 74 years gained $100,000 in equity as they likely had lived in their homes for a longer period of time.”

Despite the benefits of growing home equity, some homeowners are still hesitant to move and could be considering remodeling or making changes to their current space instead. However, if you’ve thought about aging in place rather than downsizing, you may want to reconsider. The U.S. Census Bureaupoints out:

“Of the nation’s 115 million housing units, only 10% are ready to accommodate older populations.”

If your house is no longer the best fit for your evolving needs, it may be time to put your equity to work for you and downsize to the home you really want.

Bottom Line

Today’s housing market favors homeowners who are ready to sell their houses and make a move. If you’re thinking about downsizing this year, let’s connect to discuss your options in our local market.

A Fannie Maesurvey recently revealed some of the most highly-rated benefits of homeownership, which continue to be key drivers in today’s power-packed housing market. Here are the top four financial benefits of owning a home according to consumer respondents:

88% – a better chance of saving for retirement

87% – the best investment plan

85% – the chance to be better off financially

85% – the chance to build up wealth

Additional financial advantages of homeownership included in the survey are having the best overall tax situation and being able to live within your budget.

Does homeownership actually give you a better chance to build wealth?

No one can question a person’s unique feelings about the importance of homeownership. However, it’s fair to ask if the numbers justify homeownership as a financial asset.

Last fall, the Federal Reserve released the Survey of Consumer Finances, a report done every three years, with the latest edition covering through 2019. Their findings confirmed that homeownership is a clear financial benefit. The survey found that homeownershave forty times higher net worth than renters ($255,000 for homeowners compared to $6,300 for renters).

The difference in net worth between homeowners and renters has continued to grow. Here’s a graph showing the results of the last four Fed surveys:The above graph only includes data through 2019, but according to CoreLogic, the equity held by homeowners grew by $26,300 over the last twelve months alone. That means the gap between the net worth of homeowners and renters has probably widened even further over the last year.

Some might argue the difference in net worth may be due to homeowners normally having larger incomes than renters and therefore the ability to save more money. However, a study by First American shows homeowners have greater net worth than renters regardless of their income level. Here are the findings:Others may think homeowners are older and that’s why they have a greater net worth. However, a Joint Center for Housing Studies ofHarvard Universityreport on homeowners and renters over the age of 65 reveals:

“The ability to build equity puts homeowners far ahead of renters in terms of household wealth…the median owner age 65 and over had home equity of $143,500 and net wealth of $319,200. By comparison, the net wealth of the same-age renter was just $6,700.”

Homeowners 65 and older have 47.6 times greater net worth than renters.

Bottom Line

The idea of homeownership as a direct way to build your net worth has met the test of time. Let’s connect if you’re ready to take steps toward becoming a homeowner.

Last Friday, the Bureau of Labor Statistics released a very encouraging jobs report. The economy gained 916,000 jobs in March – well above expert projections of 650,000 to 675,000. The unemployment rate fell again and is now at 6%.

What does this mean for you?

Our lives are deeply impacted by our nation’s economy. The better the economy is doing overall, the better most individuals in the country will do as well. Here’s a look at what four experts told the Wall Street Journal after reviewing last week’s report.

Michael Feroli, JPMorgan Chase:

“The powerful tailwind of the reopening of economic activity appears to be gathering force; while the level of employment last month was still 8.4 million positions below that which prevailed before the pandemic, it is reasonable to expect that a majority of those lost jobs will be recouped in coming months.”

Mike Fratantoni, Mortgage Bankers Association:

“We fully expect that this pace of job gains will continue for months, and anticipate that the unemployment rate, now at 6%, will be well below 5% by the end of the year.”

Paul Ashworth, Capital Economics:

“With the vaccination program likely to reach critical mass within the next couple of months and the next round of fiscal stimulus providing a big boost, there is finally real light at the end of the tunnel.”

Jason Schenker, Prestige Economics:

“People are getting back to work and the vaccine isn’t just inoculating the population, it’s clearly inoculating the economy.”

What does this mean for residential real estate?

Today, the biggest challenge for homebuyers is the lack of homes currently for sale. With listing inventory down 52% from a year ago, bidding wars are skyrocketing. As a result, home prices are climbing.

One answer to this challenge is to build more homes to satisfy the demand. The latest jobs report gives hope for new housing construction, and therefore brings hope to buyers as well. Here’s what three industry economists said about the increase in construction jobs revealed in the report:

“Construction jobs boomed in March, one of the largest monthly gains ever. This raises the prospect for more home building and more inventory reaching the market in the upcoming months. The housing market has been hot with fast rising home prices but has been constrained by a lack of supply. By hiring more workers and building more homes, home prices will move to a manageable level to give more Americans a shot at ownership.”

“Great jobs report for a housing market in an inventory crisis. Residential construction building jobs increased 3.9% from pre-2020 recession peak in Feb. 2020. The construction industry remains a labor-intensive industry. We need more hammers at work to build more homes.”

“Good job numbers in March for residential construction. 37,000 gain from Feb to March. 3.03 million total employment for home builders and remodelers, and up 49,100 from Jan 2020.”

Bottom Line

An improving economy with a falling unemployment rate will benefit households across the country, as well as the overall housing market.

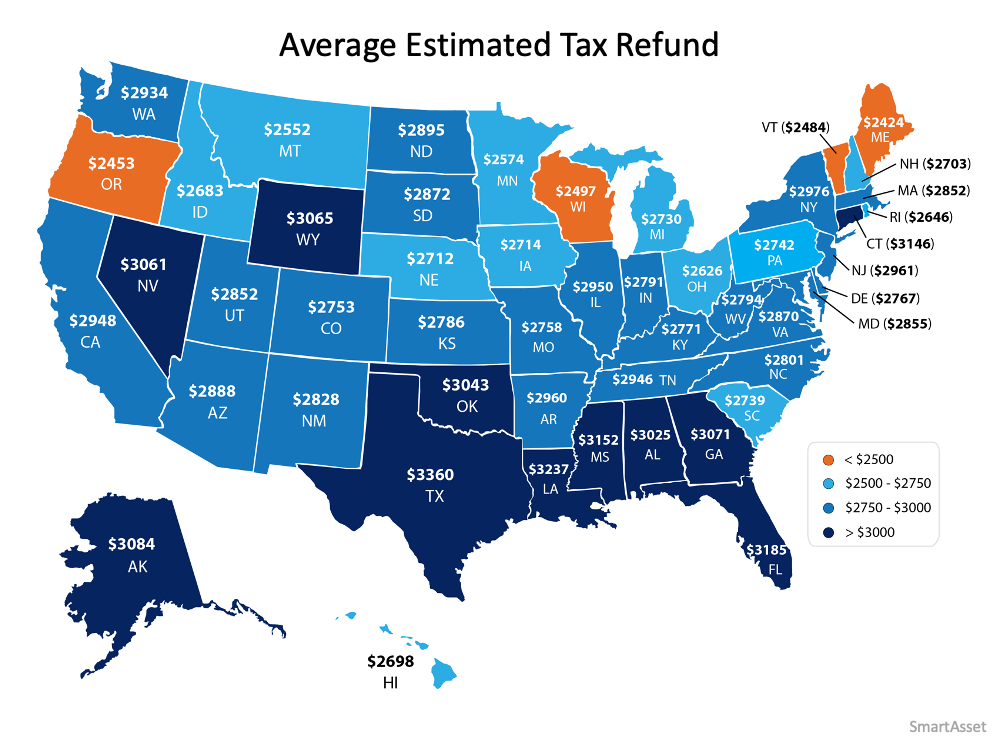

If you’re planning to buy a home this year, saving for a down payment is one of the most important steps in the process. One of the best ways to jumpstart your savings is by starting with the help of your tax refund.

Using data from the Internal Revenue Service (IRS), it’s estimated that Americans can expect an average refund of $2,925 when filing their taxes this year. The map below shows the average anticipated tax refund by state:Thanks to programs from the Federal Housing Authority, Freddie Mac, and Fannie Mae, many first-time buyers can purchase a home with as little as 3% down. In addition, Veterans Affairs Loans allow many veterans to put 0% down. You may have heard the common myth that you need to put 20% down when you buy a home, but thankfully for most homebuyers, a 20% down payment isn’t actually required. It’s important to work with your real estate professional and your lender to understand all of your options.

How can your tax refund help?

If you’re a first-time buyer, your tax refund may cover more of a down payment than you realize.

If you take into account the median home sale price by state, the map below shows the percentage of a 3% down payment that’s covered by the average anticipated tax refund:The darker the blue, the closer your tax refund gets you to homeownership when you qualify for one of the low down payment programs. Maybe this is the year to plan ahead and put your tax refund toward the down payment on a home.

Not enough money from your tax return?

A recent paper from the National Bureau of Economic Research found that, of the households that received a stimulus check last year, “One third report that they primarily saved the stimulus money.” If you had the opportunity to save your Economic Impact Payments, you may consider putting that money toward your down payment or closing costs as well. Your trusted real estate professional can also advise you on the down payment assistance programs available in your area.

Bottom Line

Saving for a down payment can seem like a daunting task, but it doesn’t have to be. This year, your tax refund and your stimulus savings could add up big when it comes to reaching your homeownership goals.

Today, some are afraid the real estate market is starting to look a lot like it did in 2006, just prior to the housing crash. One of the factors they’re pointing to is the availability of mortgage money. Recent articles about the availability of low down payment loans and down payment assistance programs are causing fear that we’re returning to the bad habits seen 15 years ago. Let’s alleviate these concerns.

Several times a year, the Mortgage Bankers Association releases an index titled The Mortgage Credit Availability Index (MCAI). According to their website:

“The MCAI provides the only standardized quantitative index that is solely focused on mortgage credit. The MCAI is…a summary measure which indicates the availability of mortgage credit at a point in time.”

Basically, the index determines how easy it is to get a mortgage. The higher the index, the more available mortgage credit becomes. Here’s a graph of the MCAI dating back to 2004, when the data first became available:As we can see, the index stood at about 400 in 2004. Mortgage credit became more available as the housing market heated up, and then the index passed 850 in 2006. When the real estate market crashed, so did the MCAI (to below 100) as mortgage money became almost impossible to secure. Thankfully, lending standards have eased somewhat since. The index, however, is still below 150, which is about one-sixth of what it was in 2006.

Why did the index rage out of control during the housing bubble?

The main reason was the availability of loans with extremely weak lending standards. To keep up with demand in 2006, many mortgage lenders offered loans that put little emphasis on the eligibility of the borrower. Lenders were approving loans without always going through a verification process to confirm if the borrower would likely be able to repay the loan.

Some of these loans offered attractive, low interest rates that increased over time. The loans were popular because they could be obtained quickly and without the borrower having to provide documentation up front. However, as the rates increased, borrowers struggled to pay their mortgages.

Today, lending standards are much tighter. As Investopediaexplains, the risky loans given at that time are extremely rare today, primarily because lending standards have drastically improved:

“In the aftermath of the crisis, the U.S. government issued new regulations to improve standard lending practices across the credit market, which included tightening the requirements for granting loans.”

An example of the relaxed lending standards leading up to the housing crash is the FICO® credit score associated with a loan. What’s a FICO® score? The website myFICOexplains:

“A credit score tells lenders about your creditworthiness (how likely you are to pay back a loan based on your credit history). It is calculated using the information in your credit reports. FICO® Scores are the standard for credit scores—used by 90% of top lenders.”

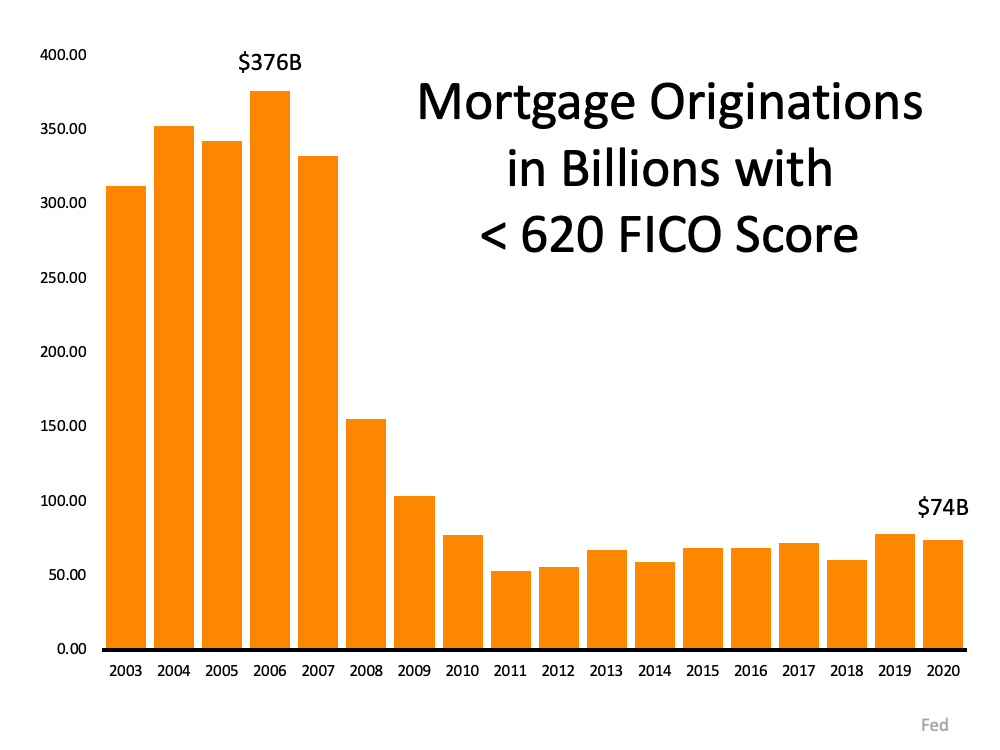

During the housing boom, many mortgages were written for borrowers with a FICO score under 620. Experianreveals that, in today’s market, lenders are more cautious about lower credit scores:

“Statistically speaking, 28% of consumers with credit scores in the Fair range are likely to become seriously delinquent in the future…Some lenders dislike those odds and choose not to work with individuals whose FICO® Scores fall within this range.”

There are definitely still loan programs that allow a 620 score. However, lending institutions overall are much more attentive about measuring risk when approving loans. According to Ellie Mae’s latest Origination Insight Report, the average FICO® score on all loans originated in February was 753.

The graph below shows the billions of dollars in mortgage money given annually to borrowers with a credit score under 620.In 2006, mortgage entities originated $376 billion dollars in loans for purchasers with a score under 620. Last year, that number was only $74 billion.

Bottom Line

In 2006, lending standards were much more relaxed with little evaluation done to measure a borrower’s potential to repay their loan. Today, standards are tighter, and the risk is reduced for both lenders and borrowers. These are two very different housing markets, so there’s no need to panic over today’s lending standards.

My name is John Bendele and these are words to live by.

“What is the biggest challenge you are facing in life right now and how can I help?”

I believe when you are able to help others in their struggles, it will always bring a since of joy and accomplishment that is like no other. I enjoy bringing opportunities to people in real estate and in life. To be a lifting hand and a beacon of knowledge. It brings me great joy to guide and support others when making exciting and difficult choices. I have been a licensed realtor for over 7 years in Minnesota. Coming from a construction background, I will provide a wealth of knowledge about homes. Knowing homes allows me to a better negotiator with facts and details some may not. I enjoy working with sellers, investors and buyers.

I grew up in Southwest Texas and moved to Minnesota in 2015. I have lived in the White Bear Lake area until making a move over the lake to Willernie, MN where I now reside. I love spending quality time with my teenage boys who nicknamed me “JoJo”. My favorite things to do are being outdoors on or in the water, BBQing (TX style) and going on any adventure.

I want to bring knowledge, growth, excitement and wealth to the clients I encounter through being a realtor. I look forward to assisting you in your amazing journey in real estate.

Thank you,

John A Bendele

Meet Brittany

Brittany is a mama of three kiddos, a wife of a firefighter and added more love to her home with three dogs and two cats. Outside of the fun she has as an agent and her roles at home she enjoys doing any DIY projects she can get her hands on!

Brittany fell in love with the Real Estate gig in 2019. She grew up in Apple Valley, and now owns her childhood home. I guess you could say she is a south metro pro!

You!

Hey! If you’re looking for your next role as an agent let us know! This could be you!

Meet Shea Amundson

Hey, I’m Shea and I love helping people find a beautiful home that sets their soul on fire!

Meet Katie

Katie comes from the busy world of entertainment and being a Traveling Operations Manager. She transitioned to Real Estate back in 2018 and has been hooked ever since! Katie thrives on training, developing new systems, and helping agents grow! Katie joins Voila with the determination to help every agent and client make their dream a reality whether it be building their business or finding that dream home!

When Katie isn’t working, she is a full-time student at Metropolitan University. She enjoys cooking foods from all over the world, traveling, and has a habit of getting a new tattoo wherever she goes. She is huge into animal conservation and spending time with her dog Sawyer who often joins her on travels!

Meet Sarah Beth Lindstrom

Sarah wants to live in a world filled with innovative businesses daring enough to break the mold…monthly auto-shipments of Laffy Taffy’s, and lots and lots of laughter!!!

Having been in the real estate industry since 2005, her go to role has always been supporting her teams in any way that she can! She has gone from Listing and Transaction Management, to Team Manager, and now Director of Support! She is an ‘introverted extrovert’ that finds the, ‘behind the scenes’ with a hint of showing homes – to be a perfect blend.

When she’s not supporting her Voila Family, she is out getting one more rep in at the gym, finding new healthy recipes to attempt (and then trick her teenager into eating somehow), and enjoying quick road trips to…well, anywhere! She also plays on a competitive volleyball team in the winter, sand volleyball in the summer and softball in the spring and fall.

“Two things define you. The patience you have when you have nothing and the attitude when you have everything.”

Meet Jessi Andersen

In June of 2020 Jessi joined team of Voila…and…it’s that easy!

Ha! No really, it did all begin in June. New to this side of Real Estate, Jessi joined in hopes to take her chatty, outgoing self and bring some good of it! Her natural tendencies of networking and love of growth and goals, have been set in direction – expanding Voila!

Where is Jess when she isn’t nurturing the growth of Voila? Adventuring with her family outside in nature. Or perhaps baking up a new recipe while dancing the day away – and of course cheering for her little athletes at home, as well as the MN Vikings/Twins!

“In the end it is not the years in your life that count. It’s the life in your years” ~ Abe Lincoln

Meet Wyatt Lemon

Wyatt is a Real Estate Extraordinaire, and a Loving Husband, and a Lover of Life and a PAW-rent to 3 awesome dogs. Huge believer in the idea that life is what you make of it, so with that being said I guess you could say the glass is half full! Things I enjoy outside of work are Yoga, being a big time Foodie, and spending time with my family. I grew up in Hugo MN and have been a local resident my whole life. I studied Marketing at Century College as well as St. Cloud State University. I got into Real Estate in October of 2018 and have loved every minute of it!

Meet James Andersen

James Andersen is a human being who believes that the best in others is a reflection of the energy we bring.

Magnanimous behavior is the standard not the exception.

10+ years Army Career

5+ years Married

5+ years Father of Calendar Crushers

5+ years Real Estate Career

30+ years Life Experience

Let’s learn and grow together.

Meet Joey Torkildson

You are writing your own story in life! Is what you are doing right now supposed to be in that story? I hope so!

That’s why my goal is to always sign up, get uncomfortable, inspire through doing, shoot, then aim. We don’t have enough time on this planet to stay mundane and there are too many experiences to be doing one thing for too long! It’s all about the short term experiments!

Quick background: 19+ year US Army Master Sergeant vet; 10+ year transformer of lives through ownership (AKA: Realtor) ; 2+ year CEO of an Expansion Team with Hergenrother Realty Group ; Director of Agent Training with that same organization; Self employed for 12+ years; starting in late 2019 CoFounded a new disruptive real estate brokerage, Voila; Contagiously energetic teacher who loves helping people discover they can accomplish anything; Dad of two extremely crazy and loving boys; Husband of an amazingly supportive and ultimate gardener wife.

Let’s be curious explorers together! I love connecting with people and helping them achieve their goals and I’m a firm believer in the fact that you are one introduction away from your entire life changing!

Two quotes I live by: Amazing things rarely happen in your comfort zone and only those who attempt the absurd achieve the impossible!

As the graph reveals, last spring’s buying market was anything but typical. Instead of sales increasing, they fell sharply as a result of stay-at-home orders that virtually shut the real estate industry down.

As the graph reveals, last spring’s buying market was anything but typical. Instead of sales increasing, they fell sharply as a result of stay-at-home orders that virtually shut the real estate industry down.