In today’s housing market, all eyes are on millennials. Not only are millennials the largest generation, but they’re also currently between 25 and 40 years old. These are often considered prime homebuying years when many people begin to form their own households and invest in real estate. If you’re like many millennials who are spending much more time at home these days, you may have a growing need for more space or upgraded features, making moving more desirable than ever.

For those millennials who already own a home, there’s a great opportunity to move up in 2021. Danielle Hale, Chief Economist at realtor.com, explains:

“Older millennials will be trade-up buyers with many having owned their first homes long enough to see substantial equity gains.”

Even if you bought a home sometime in the last few years, you may have more equity than you realize, and that’s a big factor to consider when you’re thinking about moving. According to the Homeowner Equity Insights Report from CoreLogic:

“In the third quarter of 2020, the average homeowner gained approximately $17,000 in equity during the past year. This marks the largest average equity gain since the first quarter of 2014.”

Growing equity can be the driver you’re looking for to fund your next move, especially if what you need in a home is changing right now. As equity builds over time, it can be put toward the down payment on your next home.

In addition to equity gains, today’s housing market affordability is powered by record-low mortgage rates, so moving at a time when you can get more for your money may be more realistic than you think.

Bottom Line

If you’re a millennial thinking about moving this year, you’re not alone. Let’s connect to shed light on the equity you have in your current home and the opportunities it can create.

There are so many great reasons to purchase a home, and over the past year, we’ve realized more of them than we ever thought possible. If you’re a first-time homebuyer, having a home of your own can give you a greater sense of security and accomplishment in a time that’s largely uncertain. If you’re a repeat buyer looking for your dream home, making a move might give you the space or features you need to find greater success and happiness in a new normal way of life. Whatever your motivations are, here are three reasons why becoming a homeowner now may help you win big in the long run.

1. Buying a Home Is a Great Investment

Several recent reports indicate that real estate is still a good investment, topping other options such as gold, stocks, bonds, and savings. Why? Real estate helps you build equity, a type of forced savings that grows your net worth. According to the latest Equity Report from ATTOM Data Solutions:

“The count of equity-rich properties in the fourth quarter of 2020 represented 30.2 percent, or about one in three, of the 59 million mortgaged homes in the United States. That was up from 28.3 percent in the third quarter of 2020, 27.5 percent in the second quarter and 26.7 percent in the fourth quarter of 2019, despite the ongoing economic damage caused by the worldwide Coronavirus pandemic.”

2. Mortgage Interest Rates Are Low

The Primary Mortgage Market Survey from Freddie Mac indicates interest rates for a 30-year mortgage have fallen since November 2018 when they hit 4.94%. In their latest forecast, Freddie Mac expects rates to remain low, leveling out to an average of 2.9% in 2021.

When you purchase a home at a low mortgage rate, it will impact your monthly mortgage payment, giving you the opportunity to likely get more house for your money.

3. Investing in Your Future Pays Off

There are some renters who haven’t purchased a home yet because they’re uncomfortable taking on the obligation of a mortgage. What many renters don’t realize, though, is the financial power of equity.

As a homeowner, your monthly mortgage payment becomes a form of ‘forced savings’ you can reinvest later in life as you see fit. You can use it in a variety of ways, like to fund a loved one’s education, move up to a bigger home, or start your own business. As a renter, you’re actually growing your landlord’s equity instead of your own.

If you’re ready to put your monthly payments to work for you and take steps toward those dreams and goals, purchasing a home may be the way to go, especially as rental prices continue to rise.

Bottom Line

Buying a home sooner rather than later could lead to substantial savings and long-term financial growth. Let’s connect to determine if homeownership is the right choice for you this year.

Headlines matter. Right now, it’s hard to read about real estate without seeing a headline that suggests homes have become unaffordable for most Americans. In reality, there’s hard evidence that shows how owning a home is more affordable than renting in most parts of the country, as record-low interest rates are keeping monthly mortgage payments about 23% lower than the typical payment of 20 years ago. Despite the facts, misleading headlines persist, and they impact how hopeful homebuyers perceive the market.

In a recent survey by realtor.com, home shoppers indicated they were surprised by what they could actually afford when buying their first home. In fact, 47% discovered their budget was larger than they expected. George Ratiu, Senior Economist at realtor.com, explains:

“For first-time buyers, especially, the drop in the 30-year mortgage rate…has provided unexpected leverage. Lower rates allowed many buyers to stretch and buy more expensive homes while keeping their monthly budget the same.”

So why do these negative headlines that cast doubt on affordability continue to exist?

Most analysts only look at two of the three elements that make up the affordability equation: price and income. It’s true that incomes haven’t kept up with the price of houses. However, affordability is about the cost of the home, not just the price. For that reason, mortgage rates, the third element of the affordability equation, are important to consider.

For example, here’s the typical mortgage payment for assorted dates going back to 2000, as calculated by CoreLogic:Outside of the housing crash (when short sales and foreclosures drove prices down), it’s more affordable to buy a home today when you consider all three elements of the affordability equation: price, income,and mortgage rate.

Bottom Line

Whether you’re a first-time buyer or a move-up buyer, don’t let the headlines scare you away from your dream of homeownership. Instead, connect with mortgage and real estate professionals to determine what you can afford and what’s available at that price. Like almost half of the buyers in the survey, you may be pleasantly surprised.

As more people continue to identify their changing needs this year, some are turning to the upscale housing sector for more space or finer features. In their most recent Luxury Market Report, the Institute for Luxury Home Marketing (ILHM) shares:

“In a snapshot of 2020, despite the devasting effects of the coronavirus pandemic, the luxury real estate market has seen one of its strongest years since 2008. In comparison to experts’ predictions in early 2020, it is remarkable how significant demands for property type, location, and amenity preferences have changed amid the pandemic.”

With more opportunities to work from home and a growing interest in having extra space for things like virtual school, working out, and cooking more meals, the desire to own a home that can meet these needs continues to increase. Additionally, record-low mortgage rates are creating opportunities for homebuyers to stretch their legs into higher price points or even expand their real estate portfolios. The ILHM report continues to say:

“Experts believe that the demand for exclusive residential properties outside the metropolitan areas will continue well into 2021; even with the introduction of vaccines, the pandemic is far from over.

For those who have moved to the suburbs and beyond, moving back to the city full time is unlikely while the work from home trend remains. Many of these affluent homeowners are now making their secondary properties their primary residences for the foreseeable future.”

If you’re interested in buying a home this year, it appears that some higher-priced markets may have more homes to choose from than those at lower price points. Javier Vivas, Director of Economic Research at realtor.com, notes:

“Interestingly, markets, where new supply is improving the fastest, tend to be higher priced than those that have yet to see improvement, suggesting sellers are more active in the more expensive markets.”

Bottom Line

If you’re hoping to buy the home of your dreams, this could be the year to achieve that goal. Let’s connect today to explore your possibilities.

Home values appreciated by about ten percent in 2020, and they’re forecast to appreciate by about five percent this year. This has some voicing concern that we may be in another housing bubble like the one we experienced a little over a decade ago. Here are three reasons why this market is totally different.

1. This time, housing supply is extremely limited

The price of any market item is determined by supply and demand. If supply is high and demand is low, prices normally decrease. If supply is low and demand is high, prices naturally increase.

In real estate, supply and demand are measured in “months’ supply of inventory,” which is based on the number of current homes for sale compared to the number of buyers in the market. The normal months’ supply of inventory for the market is about 6 months. Anything above that defines a buyers’ market, indicating prices will soften. Anything below that defines a sellers’ market in which prices normally appreciate.

Between 2006 and 2008, the months’ supply of inventory increased from just over 5 months to 11 months. The months’ supply was over 7 months in twenty-seven of those thirty-six months, yet home values continued to rise.

Months’ inventory has been under 5 months for the last 3 years, under 4 for thirteen of the last fourteen months, under 3 for the last six months, and currently stands at 1.9 months – a historic low.

Remember, if supply is low and demand is high, prices naturally increase.

2. This time, housing demand is real

During the housing boom in the mid-2000s, there was what Robert Schiller, a fellow at the Yale School of Management’s International Center for Finance, called “irrational exuberance.” The definition of the term is, “unfounded market optimism that lacks a real foundation of fundamental valuation, but instead rests on psychological factors.” Without considering historic market trends, people got caught up in the frenzy and bought houses based on an unrealistic belief that housing values would continue to escalate.

The mortgage industry fed into this craziness by making mortgage money available to just about anyone, as shown in the Mortgage Credit Availability Index (MCAI) published by the Mortgage Bankers Association. The higher the index, the easier it is to get a mortgage; the lower the index, the more difficult it is to obtain one. Prior to the housing boom, the index stood just below 400. In 2006, the index hit an all-time high of over 868. Again, just about anyone could get a mortgage. Today, the index stands at 122.5, which is well below even the pre-boom level.

In the current real estate market, demand is real, not fabricated. Millennials, the largest generation in the country, have come of age to marry and have children, which are two major drivers for homeownership. The health crisis is also challenging every household to redefine the meaning of “home” and to re-evaluate whether their current home meets that new definition. This desire to own, coupled with historically low mortgage rates, makes purchasing a home today a strong, sound financial decision. Therefore, today’s demand is very real.

Remember, if supply is low and demand is high, prices naturally increase.

3. This time, households have plenty of equity

Again, during the housing boom, it wasn’t just purchasers who got caught up in the frenzy. Existing homeowners started using their homes like ATM machines. There was a wave of cash-out refinances, which enabled homeowners to leverage the equity in their homes. From 2005 through 2007, Americans pulled out $824 billion dollars in equity. That left many homeowners with little or no equity in their homes at a critical time. As prices began to drop, some homeowners found themselves in a negative equity situation where the mortgage was higher than the value of their home. Many defaulted on their payments, which led to an avalanche of foreclosures.

Today, the banks and the American people have shown they learned a valuable lesson from the housing crisis a little over a decade ago. Cash-out refinance volume over the last three years was less than a third of what it was compared to the 3 years leading up to the crash.

This conservative approach has created levels of equity never seen before. According to Census Bureaudata, over 38% of owner-occupied housing units are owned ‘free and clear’ (without any mortgage). Also, ATTOM Data Solutions just released their fourth quarter 2020 U.S. Home Equity Report, which revealed:

“17.8 million residential properties in the United States were considered equity-rich, meaning that the combined estimated amount of loans secured by those properties was 50 percent or less of their estimated market value…The count of equity-rich properties in the fourth quarter of 2020 represented 30.2 percent, or about one in three, of the 59 million mortgaged homes in the United States.”

If we combine the 38% of homes that are owned free and clear with the 18.7% of all homes that have at least 50% equity (30.2% of the remaining 62% with a mortgage), we realize that 56.7% of all homes in this country have a minimum of 50% equity. That’s significantly better than the equity situation in 2008.

Bottom Line

This time, housing supply is at a historic low. Demand is real and rightly motivated. Even if there were to be a drop in prices, homeowners have enough equity to be able to weather a dip in home values. This is nothing like 2008. In fact, it’s the exact opposite.

Over the past year, our homes have become an integral part of our lives more than ever. They’re much more than the houses we live in. They’re our workplaces, virtual schools, and safe havens that provide shelter, stability, and protection through the evolving health crisis. Today, 65.8% of Americans are fortunate enough to call their homes their own.

As we continue to think about the future, our goals for the year, and what we want to achieve well beyond 2021, it’s a great time to look at the benefits of owning a home. Below are some highlights and quotes on the benefits of homeownership shared by the National Association of Realtors (NAR). From feel-good motivations to economic and social impacts on the local community, these items may give you reason to believe homeownership stretches well beyond your financial investment.

Non-Financial Benefits

Owning a home brings a sense of happiness, satisfaction, and pride.

Pride of Ownership: It feels good to have a place that’s truly your own, especially since you can customize it to your liking. “The personal satisfaction and sense of accomplishment achieved through homeownership can enhance psychological health, happiness and well-being for homeowners and those around them.”

Civic Participation: Homeownership creates stability, a sense of community, and increases civic engagement. It’s a way to add to the strength of your local area and drive value into your neighborhood.

Financial Benefits

Buying a home is also an investment in your financial future.

Net Worth: Homeownership builds your net worth. Today, the median household net worth of all homeowners is $254,900, while the median net worth of renters is only $6,270.

Financial Security: Equity, appreciation, and more predictable monthly housing expenses are huge financial benefits of owning a home. Homeownership is truly the best way to improve your long-term financial position.

Economic Benefits

Homeownership is even a local economic driver.

Housing-Related Spending: An economic force throughout our nation, housing-related expenses accounted for more than one-sixth of the country’s economic activity over the past three decades.

Entrepreneurship: Homeownership is also a form of forced savings that can provide entrepreneurial opportunities. “Owning a home enables new entrepreneurs to obtain access to credit to start or expand a business and generate new jobs by using their home as collateral for small business loans.”

Bottom Line

The benefits of homeownership go well beyond the basics. Homeownership is truly a way to build financial freedom, find greater satisfaction and happiness, and make a substantial impact in your community. If owning a home is part of your dream this year, let’s connect so you can begin the homebuying process today.

In today’s housing market, there are clear financial benefits to owning a home: increasing equity, the chance to build your net worth, and appreciating home values, just to name a few. If you’re a renter, it’s never too early to think about how homeownership can propel you toward a stronger future. Here’s a dive into three often-overlooked financial benefits of homeownership and how preparing for them now can steer you in the direction of greater financial security and savings.

1. You Won’t Always Have a Monthly Housing Payment

“Every payment brings you closer to owning the house. When you pay your rent, that money is spent. Gone. Bye. Not returning. But when you pay your mortgage, you work toward full ownership.”

As a homeowner, you can eventually eliminate the monthly payment you make on your house. That’s a huge win and a big factor in how homeownership can drive stability and savings in your life. As soon as you buy a home, your monthly housing costs begin to work for you as forced savings in the form of equity. When you build equity and grow your net worth, you can continue to reinvest those savings into your future, maybe even by buying that next dream home. The possibilities are truly endless.

2. Homeownership Is a Tax Break

One thing people who have never owned a home don’t always think about are the tax advantages of homeownership. The same article states:

“You have tax advantages. Many of the costs of owning a home—like property taxes—are tax deductible. And if you’re paying off a mortgage, you’ll get to count your mortgage interest as a deduction when you file your tax return.”

Whether you’re living in your first home or your fifth, it’s a huge financial advantage to have some tax relief tied to the interest you pay each year. It’s one thing you definitely don’t get when you’re renting. Be sure to work with a tax professional to get the best possible benefits on your annual return.

3. Monthly Housing Costs Are Predictable

A third benefit is the fact that monthly costs start to become more predictable with homeownership, something that doesn’t happen if you’re renting. Ramsey also notes:

“Rent rates will go up. Even if you found a killer deal in a hot area, inflation, competition, and rising property values will cause your rent to go up year after year.”

With a mortgage, you can keep your monthly housing costs relatively steady and predictable. Your monthly costs are most likely based on a fixed-rate mortgage, which allows you to budget your finances over a longer period of time. Rental prices have been skyrocketing since 2012, and with today’s low mortgage rates, it’s a great time to get more for your money when purchasing a home. If you want to lock-in your monthly payment at a low rate and have a solid understanding of what you’re going to spend in your mortgage payment each month, buying a home may be your best bet.

Bottom Line

If you’re ready to start feeling the benefits of stability, savings, and predictability that come with owning a home, let’s connect to determine if buying sooner rather than later is right for you.

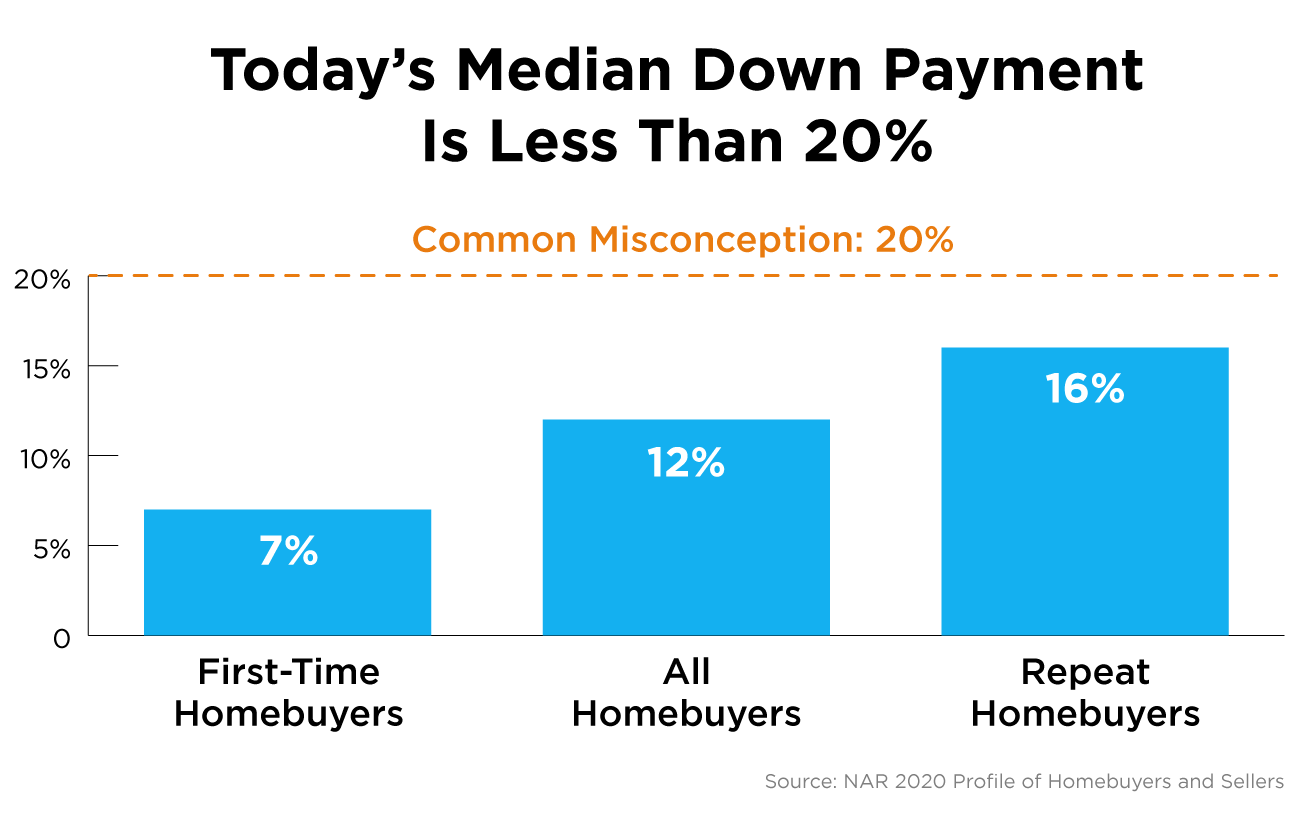

Is the idea of saving for a down payment holding you back from buying a home right now? You may be eager to take advantage of today’s low mortgage rates, but the thought of needing a large down payment might make you want to pump the brakes. Today, there’s still a common myth that you have to come up with 20% of the total sale price for your down payment. This means people who could buy a home may be putting their plans on hold because they don’t have that much saved yet. The reality is, whether you’re looking for your first home or you’ve purchased one before, youmost likelydon’t need to put 20% down. Here’s why.

“The most damaging down payment myth—since it stops the homebuying process before it can start—is the belief that 20% is necessary.”

If saving that much money sounds daunting, potential homebuyers might give up on the dream of homeownership before they even begin – but they don’t have to.

Data in the 2020 Profile of Home Buyers and Sellers from the National Association of Realtors (NAR) indicates that the median down payment actually hasn’t been over 20% since 2005, and even then, that was for repeat buyers, not first-time homebuyers. As the image below shows, today’s median down payment is clearly less than 20%.

What does this mean for potential homebuyers?

As we can see, the median down payment was lowest for first-time buyers with the 2020 percentage coming in at 7%. If you’re a first-time buyer and putting down 7% still seems high, understand that there are programs that allow qualified buyers to purchase a home with a down payment as low as 3.5%. There are even options like VA loans and USDA loans with no down payment requirements for qualified applicants.

It’s important for potential homebuyers (whether they’re repeat or first-time buyers) to know they likely don’t need to put down 20% of the purchase price, but they do need to do their homework to understand the options available. Be sure to work with trusted professionals from the start to learn what you may qualify for in the homebuying process.

Bottom Line

Don’t let down payment myths keep you from hitting your homeownership goals. If you’re hoping to buy a home this year, let’s connect to review your options.

Every year, households across the country make the decision to rent for another year or take the leap into homeownership. They look at their earnings and savings and then decide what makes the most financial sense. That equation will most likely take into consideration monthly housing costs, tax advantages, and other incremental expenses. Using these measurements, recent studies show that it’s still more affordable to own than rent in most of the country.

There is, however, another financial advantage to owning a home that’s often forgotten in the analysis – the wealth built through equity when you own a home.

Odeta Kushi, Deputy Chief Economist for First American, discusses this point in a recent blog post. She explains:

“Once you include the equity benefit of price appreciation, owning made more financial sense than renting in 48 out of the 50 top markets, with the only exceptions being San Francisco and San Jose, Calif.”

What has this equity piece meant to homeowners in the past?

ATTOM Data Solutions, the curator of one of the nation’s premier property databases, just analyzed the typical home-price gain owners nationwide enjoyed when they sold their homes. Here’s a breakdown of their findings:The typical gain in the sale of the home (equity) has increased significantly over the last five years.

CoreLogic, another property data curator, also weighed in on the subject. According to their latest Homeowner Equity Insights Report, the average homeowner gained $17,000 in equity in just the last year alone.

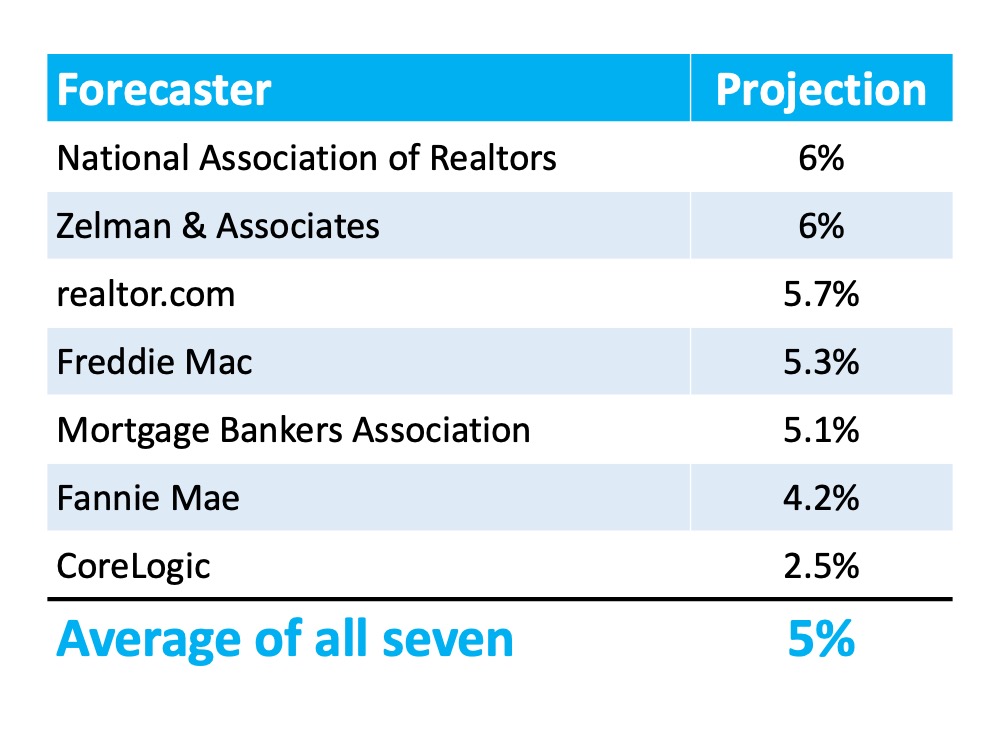

What does the future look like for homeowners when it comes to equity?

Here are the seven major home price appreciation forecasts for 2021:The National Association of Realtors (NAR) just reported that today, the median-priced home in the country sells for $309,800. If homes appreciate by 5% this year (the average of the forecasts), the homeowner will increase their wealth by $15,490 in 2021 through increased equity.

Bottom Line

As you make your plans for the coming year, be sure to consider the equity benefits of home price appreciation as you weigh the financial advantages of buying over renting. When you do, you may find this is the perfect time to jump into homeownership.

As we approach the anniversary of the hardships we’ve faced through this pandemic and the subsequent recession, it’s normal to reflect on everything that’s changed and wonder what’s ahead for 2021. While there are signs of economic recovery as vaccines are being issued, we still have a long way to go. It’s at times like these we want exact information about anything we’re doing. That information brings knowledge, and this gives us a sense of relief and comfort in uncertain times.

If you’re thinking about buying or selling a home today, the same need for information is very real. But, because it’s such a big step in our lives, that desire for clear information is even greater in the homebuying or selling process. Given the current level of overall anxiety, we want that advice to be truly perfect. The challenge is, no one can give you “perfect” advice. Experts can, however, give you the best advice possible.

Let’s say you need an attorney, so you seek out an expert in the type of law required for your case. When you go to her office, she won’t immediately tell you how the case is going to end or how the judge or jury will rule. If she could, that would be perfect advice. What a good attorney can do, however, is discuss with you the most effective strategies you can take. She may recommend one or two approaches she believes will be best for your case.

She’ll then leave you to make the decision on which option you want to pursue. Once you decide, she can help you put a plan together based on the facts at hand. She’ll help you achieve the best possible resolution and make whatever modifications in the strategy are necessary to guarantee that outcome. That’s an example of the best advice possible.

The role of a real estate professional is just like the role of a lawyer. An agent can’t give you perfect advice because it’s impossible to know exactly what’s going to happen throughout the transaction – especially in this market.

An agent can, however, give you the best advice possible based on the information and situation at hand, guiding you through the process to help you make the necessary adjustments and best decisions along the way. An agent will lead you to the best offer available. That’s exactly what you want and deserve.

Bottom Line

If you’re thinking of buying or selling this year, let’s connect to make sure you get the best advice possible.

My name is John Bendele and these are words to live by.

“What is the biggest challenge you are facing in life right now and how can I help?”

I believe when you are able to help others in their struggles, it will always bring a since of joy and accomplishment that is like no other. I enjoy bringing opportunities to people in real estate and in life. To be a lifting hand and a beacon of knowledge. It brings me great joy to guide and support others when making exciting and difficult choices. I have been a licensed realtor for over 7 years in Minnesota. Coming from a construction background, I will provide a wealth of knowledge about homes. Knowing homes allows me to a better negotiator with facts and details some may not. I enjoy working with sellers, investors and buyers.

I grew up in Southwest Texas and moved to Minnesota in 2015. I have lived in the White Bear Lake area until making a move over the lake to Willernie, MN where I now reside. I love spending quality time with my teenage boys who nicknamed me “JoJo”. My favorite things to do are being outdoors on or in the water, BBQing (TX style) and going on any adventure.

I want to bring knowledge, growth, excitement and wealth to the clients I encounter through being a realtor. I look forward to assisting you in your amazing journey in real estate.

Thank you,

John A Bendele

Meet Brittany

Brittany is a mama of three kiddos, a wife of a firefighter and added more love to her home with three dogs and two cats. Outside of the fun she has as an agent and her roles at home she enjoys doing any DIY projects she can get her hands on!

Brittany fell in love with the Real Estate gig in 2019. She grew up in Apple Valley, and now owns her childhood home. I guess you could say she is a south metro pro!

You!

Hey! If you’re looking for your next role as an agent let us know! This could be you!

Meet Shea Amundson

Hey, I’m Shea and I love helping people find a beautiful home that sets their soul on fire!

Meet Katie

Katie comes from the busy world of entertainment and being a Traveling Operations Manager. She transitioned to Real Estate back in 2018 and has been hooked ever since! Katie thrives on training, developing new systems, and helping agents grow! Katie joins Voila with the determination to help every agent and client make their dream a reality whether it be building their business or finding that dream home!

When Katie isn’t working, she is a full-time student at Metropolitan University. She enjoys cooking foods from all over the world, traveling, and has a habit of getting a new tattoo wherever she goes. She is huge into animal conservation and spending time with her dog Sawyer who often joins her on travels!

Meet Sarah Beth Lindstrom

Sarah wants to live in a world filled with innovative businesses daring enough to break the mold…monthly auto-shipments of Laffy Taffy’s, and lots and lots of laughter!!!

Having been in the real estate industry since 2005, her go to role has always been supporting her teams in any way that she can! She has gone from Listing and Transaction Management, to Team Manager, and now Director of Support! She is an ‘introverted extrovert’ that finds the, ‘behind the scenes’ with a hint of showing homes – to be a perfect blend.

When she’s not supporting her Voila Family, she is out getting one more rep in at the gym, finding new healthy recipes to attempt (and then trick her teenager into eating somehow), and enjoying quick road trips to…well, anywhere! She also plays on a competitive volleyball team in the winter, sand volleyball in the summer and softball in the spring and fall.

“Two things define you. The patience you have when you have nothing and the attitude when you have everything.”

Meet Jessi Andersen

In June of 2020 Jessi joined team of Voila…and…it’s that easy!

Ha! No really, it did all begin in June. New to this side of Real Estate, Jessi joined in hopes to take her chatty, outgoing self and bring some good of it! Her natural tendencies of networking and love of growth and goals, have been set in direction – expanding Voila!

Where is Jess when she isn’t nurturing the growth of Voila? Adventuring with her family outside in nature. Or perhaps baking up a new recipe while dancing the day away – and of course cheering for her little athletes at home, as well as the MN Vikings/Twins!

“In the end it is not the years in your life that count. It’s the life in your years” ~ Abe Lincoln

Meet Wyatt Lemon

Wyatt is a Real Estate Extraordinaire, and a Loving Husband, and a Lover of Life and a PAW-rent to 3 awesome dogs. Huge believer in the idea that life is what you make of it, so with that being said I guess you could say the glass is half full! Things I enjoy outside of work are Yoga, being a big time Foodie, and spending time with my family. I grew up in Hugo MN and have been a local resident my whole life. I studied Marketing at Century College as well as St. Cloud State University. I got into Real Estate in October of 2018 and have loved every minute of it!

Meet James Andersen

James Andersen is a human being who believes that the best in others is a reflection of the energy we bring.

Magnanimous behavior is the standard not the exception.

10+ years Army Career

5+ years Married

5+ years Father of Calendar Crushers

5+ years Real Estate Career

30+ years Life Experience

Let’s learn and grow together.

Meet Joey Torkildson

You are writing your own story in life! Is what you are doing right now supposed to be in that story? I hope so!

That’s why my goal is to always sign up, get uncomfortable, inspire through doing, shoot, then aim. We don’t have enough time on this planet to stay mundane and there are too many experiences to be doing one thing for too long! It’s all about the short term experiments!

Quick background: 19+ year US Army Master Sergeant vet; 10+ year transformer of lives through ownership (AKA: Realtor) ; 2+ year CEO of an Expansion Team with Hergenrother Realty Group ; Director of Agent Training with that same organization; Self employed for 12+ years; starting in late 2019 CoFounded a new disruptive real estate brokerage, Voila; Contagiously energetic teacher who loves helping people discover they can accomplish anything; Dad of two extremely crazy and loving boys; Husband of an amazingly supportive and ultimate gardener wife.

Let’s be curious explorers together! I love connecting with people and helping them achieve their goals and I’m a firm believer in the fact that you are one introduction away from your entire life changing!

Two quotes I live by: Amazing things rarely happen in your comfort zone and only those who attempt the absurd achieve the impossible!