Spring is almost here, and many are wondering what it will bring for the housing market. Even though the pandemic continues on, it’s certain to be very different from the spring we experienced at this time last year. Here’s what a few industry experts have to say about the housing market and how it will bloom this season.

“Despite early weakness, we expect to see new listings grow in March and April as they traditionally do heading into spring, and last year’s extraordinarily low new listings comparison point will mean year over year gains. One other potential bright spot for would-be homebuyers, new construction, which has risen at a year over year pace of 20% or more for the last few months, will provide additional for-sale inventory relief.”

“Some people will feel comfortable listing their home during the first half of 2021. Others will want to wait until the vaccines are widely distributed. This suggests more inventory will be for sale in late 2021 and into the spring selling season in 2022.”

“Since reaching a low point in January, mortgage rates have risen by more than 30 basis points… However, the rise in mortgage rates over the next couple of months is likely to be more muted in comparison to the last few weeks, and we expect a strong spring sales season.”

“As the housing market heads into the spring home buying season, the ongoing supply and demand imbalance all but assures more house price growth…Many find it hard to believe, but housing is actually undervalued in most markets and the gap between house-buying power and sale prices indicates there’s room for further house price growth in the months to come.”

Bottom Line

The experts are very optimistic about the housing market right now. If you pressed pause on your real estate plans over the winter, let’s chat to determine how you can re-engage in the homebuying process this spring.

Last March, many involved in the residential housing industry feared the market would be crushed under the pressure of a once-in-a-lifetime pandemic. Instead, real estate had one of its best years ever. Home sales and prices were both up substantially over the year before. 2020 was so strong that many now fear the market’s exuberance mirrors that of the last housing boom and, as a result, we’re now headed for another crash.

However, there are many reasons this real estate market is nothing like 2008. Here are six visuals to show the dramatic differences.

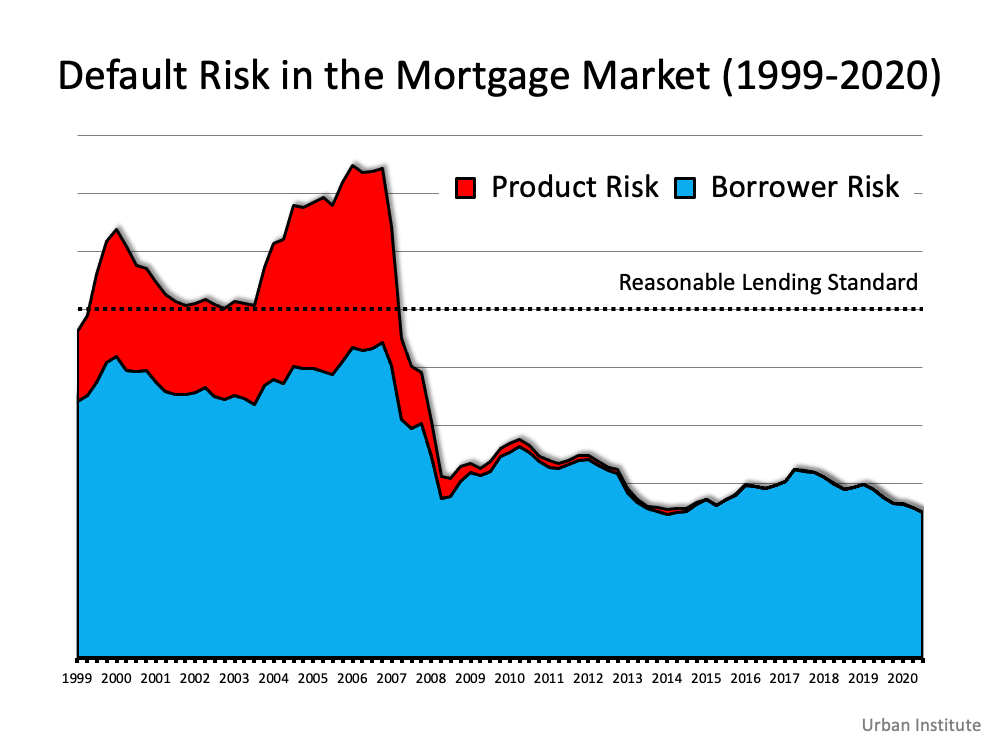

1. Mortgage standards are nothing like they were back then.

During the housing bubble, it was difficult not to get a mortgage. Today, it’s tough to qualify. Recently, the Urban Institute released their latest Housing Credit Availability Index (HCAI) which “measures the percentage of owner-occupied home purchase loans that are likely to default—that is, go unpaid for more than 90 days past their due date. A lower HCAI indicates that lenders are unwilling to tolerate defaults and are imposing tighter lending standards, making it harder to get a loan. A higher HCAI indicates that lenders are willing to tolerate defaults and are taking more risks, making it easier to get a loan.”

The index shows that lenders were comfortable taking on high levels of risk during the housing boom of 2004-2006. It also reveals that today, the HCAI is under 5 percent, which is the lowest it’s been since the introduction of the index. The report explains:

“Significant space remains to safely expand the credit box. If the current default risk was doubled across all channels, risk would still be well within the pre-crisis standard of 12.5 percent from 2001 to 2003 for the whole mortgage market.”

This is nothing like the last time.

2. Prices aren’t soaring out of control.

Below is a graph showing annual home price appreciation over the past four years compared to the four years leading up to the height of the housing bubble. Though price appreciation was quite strong last year, it’s nowhere near the rise in prices that preceded the crash.There’s a stark difference between these two periods of time. Normal appreciation is 3.8%. So, while current appreciation is higher than the historic norm, it’s certainly not accelerating out of control as it did in the early 2000s.

This is nothing like the last time.

3. We don’t have a surplus of homes on the market. We have a shortage.

The months’ supply of inventory needed to sustain a normal real estate market is approximately six months. Anything more than that is an overabundance and will causes prices to depreciate. Anything less than that is a shortage and will lead to continued appreciation. As the next graph shows, there were too many homes for sale in 2007, and that caused prices to tumble. Today, there’s a shortage of inventory, which is causing an acceleration in home values.This is nothing like the last time.

4. New construction isn’t making up the difference in inventory needed.

Some may think new construction is filling the void. However, if we compare today to right before the housing crash, we can see that an overabundance of newly built homes was a major challenge then, but isn’t now.This is nothing like the last time.

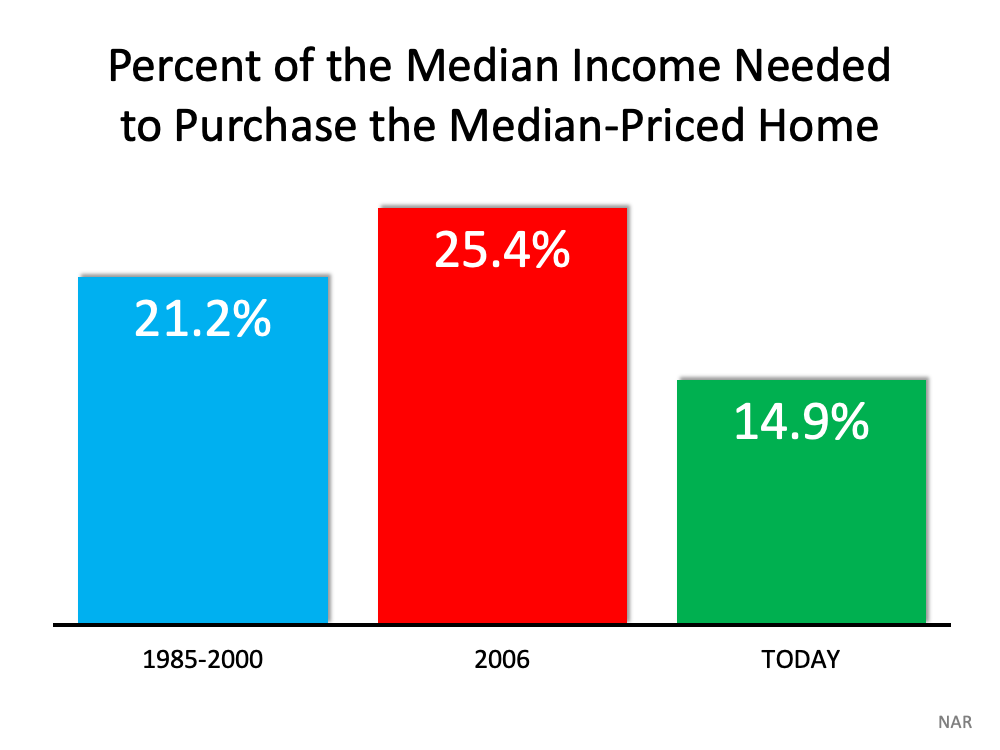

5. Houses aren’t becoming too expensive to buy.

The affordability formula has three components: the price of the home, the wages earned by the purchaser, and the mortgage rate available at the time. Fifteen years ago, prices were high, wages were low, and mortgage rates were over 6%. Today, prices are still high. Wages, however, have increased, and the mortgage rate is about 3%. That means the average homeowner pays less of their monthly income toward their mortgage payment than they did back then. Here’s a chart showing that difference:As Mark Fleming, Chief Economist for First American, explains:

“Lower mortgage interest rates and rising incomes correspond with higher house prices as home buyers can afford to borrow and buy more. If housing is appropriately valued, house-buying power should equal or outpace the median sale price of a home. Looking back at the bubble years, house prices exceeded house-buying power in 2006, but today house-buying power is nearly twice as high as the median sale price nationally.”

This is nothing like the last time.

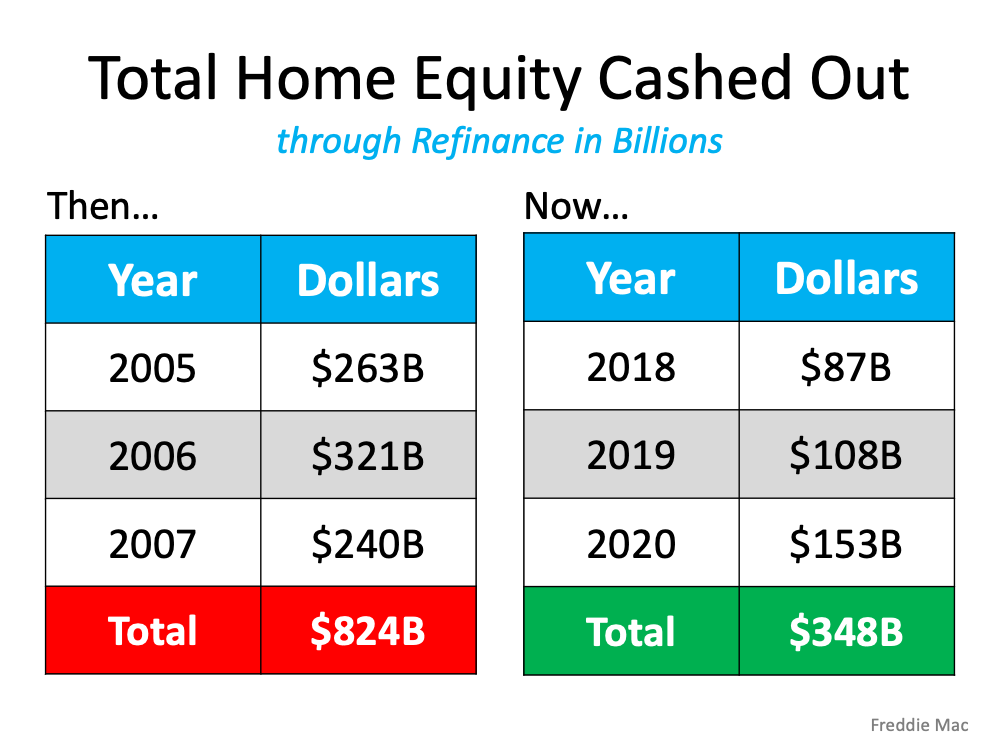

6. People are equity rich, not tapped out.

In the run-up to the housing bubble, homeowners were using their homes as personal ATM machines. Many immediately withdrew their equity once it built up, and they learned their lesson in the process. Prices have risen nicely over the last few years, leading to over 50% of homes in the country having greater than 50% equity – and owners have not been tapping into it like the last time. Here’s a table comparing the equity withdrawal over the last three years compared to 2005, 2006, and 2007. Homeowners have cashed out almost $500 billion dollars less than before:During the crash, home values began to fall, and sellers found themselves in a negative equity situation (where the amount of the mortgage they owed was greater than the value of their home). Some decided to walk away from their homes, and that led to a wave of distressed property listings (foreclosures and short sales), which sold at huge discounts, thus lowering the value of other homes in the area. With the average home equity now standing at over $190,000, this won’t happen today.

This is nothing like the last time.

Bottom Line

If you’re concerned that we’re making the same mistakes that led to the housing crash, take a look at the charts and graphs above to help alleviate your fears.

When selling a house, most homeowners hope for a quick and profitable transaction that puts them in a position to make a great move. If you’re waiting for the best time to win as a seller, the market is calling your name this spring. Here are five reasons why this is the perfect time to sell your house if you’re ready.

1. There’s high demand from homebuyers.

Buyer demand is strong right now, and buyers are active in the market. ShowingTime, which tracks the average number of buyer showings on residential properties, recently announced that buyer showings are up 51.5% compared to this time last year. Daniil Cherkasskiy, Chief Analytics Officer at ShowingTime, notes:

“As anticipated, demand for real estate remains elevated and continues to be affected by low levels of inventory…On average, each home is getting 50 percent or more requests this year compared to January of last year. As we head into the busy season, it’s likely we’ll push into even more extreme territory until the supply starts catching up with demand.”

When your house is positioned to get a ton of attention from competitive buyers, you’re in the best spot possible as the seller.

2. There aren’t enough houses for sale.

Purchaser demand is so high, the market is running out of available houses for sale. Recently, realtor.comreported:

“Nationally, the inventory of homes for sale in February decreased by 48.6% over the past year, a higher rate of decline compared to the 42.6% drop in January. This amounted to 496,000 fewer homes for sale compared to February of last year.”

The National Association of Realtors (NAR) also reveals that, while home sales are skyrocketing, the inventory of existing homes for sale is continuing to drop dramatically. Houses are essentially selling as fast as they’re hitting the market – in fact, NAR reports that the average house is on the market for only 21 days.

It’s this imbalance between high buyer demand and a low supply of houses for sale that gives sellers such an advantage. A seller will always negotiate the best deal when demand is high and supply is low. That’s exactly what’s happening in the real estate market today.

3. You have a lot of leverage in today’s market.

Clearly, many more people are interested in buying than selling this spring, creating the ultimate sellers’ market. When this happens, homeowners in a position to sell have the upper hand in negotiations.

According to NAR, agents are reporting an average of 3.7 offers per house and an increase in bidding wars. As a seller, this means the ball is in your court – so much so that you can use your leverage to negotiate the best possible contract. Demand is there, and now is the perfect time to sell for the most favorable terms.

4. It’s a great way to use your home equity.

According to the latest data from CoreLogic, as of the third quarter of 2020, the average homeowner gained $17,000 in equity over the past year, and that number continues to grow as home values appreciate. Equity is a type of forced savings that grows during your time as a homeowner and can be put toward bigger goals like buying your next dream home.

Mark Fleming, Chief Economist at First American,notes:

“As homeowners gain equity in their homes, they are more likely to consider using that equity to purchase a larger or more attractive home – the wealth effect of rising equity. In today’s housing market, fast rising demand against the limited supply of homes for sale has resulted in continued house price appreciation.”

5. It’s a chance to find a home that meets your needs.

So much has changed over the past year, including what many of us need in a home. Spending extra time where we currently live is enabling many of us to re-evaluate homeownership and what we find most important in a home.

Whether it’s a house that has the features suited to working remotely, space for virtual or hybrid schooling, a home gym or theater, or something else, selling this spring gives you a chance to make a move and find the home of your dreams.

Bottom Line

Today’s housing market belongs to the sellers. If you’ve considered making a move but have been waiting for the right market conditions, your wait may be over. Let’s connect so you’ll be positioned to win when you sell your house this spring.

Last year, many homeowners thought twice about selling their houses due to the onset of the health crisis. This year, however, homeowners are beginning to regain their confidence when it comes to selling safely. The latest Home Purchase Sentiment Index (HPSI) by Fannie Mae shows that 57% of consumers believe now is a good time to sell.

Doug Duncan, Vice President and Chief Economist at Fannie Mae,explains:

“Overall, the index’s monthly increase was driven largely by a substantial jump in the share of consumers reporting that it’s a good time to sell a home, with many citing favorable mortgage rates, high home prices, and low housing inventory as their primary rationale.”

Normally, spring is the busiest season in the housing market – the time when many homeowners decide to list their houses. While this is obviously not a normal year since the pandemic is still very much upon us, experts are optimistic that consumer positivity around selling will lead to more homeowners making moves this year. Duncan continues to say:

“We will pay close attention to see if this newfound optimism develops into a trend.”

What does this mean if you’re thinking of selling your house?

The fact that there are so few houses available for sale today is one driver that’s encouraging consumers to think more positively about selling. The National Association of Realtors (NAR) states:

“Total housing inventory at the end of January amounted to 1.04 million units, down 1.9% from December and down 25.7% from one year ago (1.40 million).”

With so few homes available to buy, your house will be more likely to rise to the top of an eager purchaser’s wish list in this competitive market. Today’s high buyer activity is creating upward pressure on home prices and more multiple-offer scenarios. According to the Realtors Confidence Index Survey from NAR, the average home for sale is receiving 3.7 offers today, up from 2.3 offers just one year ago. This makes selling even more enticing.

In this kind of sellers’ market, you have a huge advantage in the process. And here’s another win – you can also use your equity toward a down payment on a new home when you move.

Wondering where you’ll go if you try to move while it’s so challenging to find a home to buy? Well, in many areas, there are more homes available at the higher end of the market, so finding a move-up home may be less of an issue if you’re ready to search for your dream home this spring.

Bottom Line

If you pressed pause on selling your house last year, now may be the best time to put your plans back into motion while inventory is so low. Let’s connect today to get the process started.

The real estate market was on fire during the second half of 2020. Buyer demand was way up, and the supply of homes available for sale hit record lows. The price of anything is determined by the supply and demand ratio, so home prices skyrocketed last year. Dr. Lynn Fisher, Deputy Director of the Federal Housing Finance Agency (FHFA) Division of Research and Statistics, explains:

“House prices nationwide recorded the largest annual and quarterly increase in the history of the FHFA Home Price Index. Low mortgage rates, pent up demand from homebuyers, and a limited housing supply propelled every region of the country to experience faster growth in 2020 compared to a year ago despite the pandemic.”

Here are the year-end home price appreciation numbers from the FHFA and two other prominent pricing indexes:

The past year was truly a remarkable time for homeowners as prices appreciated substantially. Lawrence Yun, Senior Economist at the National Association of Realtors (NAR), reveals:

“A typical homeowner in 2020, just by being a homeowner, would have accumulated around $24,000 in housing wealth.”

What will happen with home prices this year?

Many experts believe buyer demand will soften somewhat as mortgage rates are poised to bump up slightly. Some also believe the inventory challenge will ease as more listings come to market this year.

Based on this, most forecasters anticipate we’ll see strong appreciation in 2021 – but not as strong as last year. Here are seven prominent groups and their projections:

Bottom Line

Home price appreciation will be strong this year, but it won’t reach the historic levels of 2020. Let’s connect if you’d like to find out what your house is currently worth in our local market.

If you’re looking for a home to purchase right now and having trouble finding one, you’re not alone. At a time like this when there are so few houses for sale, it’s normal to wonder if you’ll actually find one to buy. According to the National Association of Realtors (NAR), across the country, inventory of available homes for sale is at an all-time low – the lowest point recorded since NAR began tracking this metric in 1982. There are, however, more homes expected to hit the market later this year. Let’s break down the three key places they’ll likely come from as 2021 continues on.

1. Homeowners Who Didn’t Sell Last Year

In 2020, many sellers decided to pause their moving plans for a number of different reasons. From health concerns about the pandemic to financial uncertainty, plenty of homeowners decided not to move last year.

Now that vaccines are being distributed and there’s a light at the end of the COVID-19 tunnel, it should bring some peace of mind to many potential sellers. As Danielle Hale, Chief Economist at realtor.com, notes:

“Fortunately for would-be homebuyers, we expect sellers to return to the market as we see improvement in the economy and progress against the coronavirus.”

Many of the homeowners who decided not to sell in 2020 will enter the market later this year as they begin to feel more comfortable showing their house in person, understanding their financial situation, and simply having more security in life.

2. More New Homes Will Be Built

Last year was a strong year for home builders, and according to the National Association of Home Builders (NAHB), 2021 is expected to be even better:

“For 2021, NAHB expects ongoing growth for single-family construction. It will be the first year for which total single-family construction will exceed 1 million starts since the Great Recession.”

With more houses being built in many markets around the country, homeowners looking for new houses that meet their changing needs will be able to move into their dream homes. When they sell their current houses, this will create opportunities for those looking to find a home that’s already built to do so. It sets a simple chain reaction in motion for hopeful buyers.

3. Those Impacted Financially by the Economic Crisis

Many experts don’t anticipate a large wave of foreclosures coming to the market, given the forbearance options afforded to current homeowners throughout the pandemic. Some homeowners who have been impacted economically will, however, need to move this year. There are also homeowners who didn’t take advantage of the forbearance option or were already in a foreclosure situation before the pandemic began. In those cases, homeowners may decide to sell their houses instead of going into the foreclosure process, especially given the equity in homes today. Lawrence Yun, Chief Economist at NAR, explains:

“Given the huge price gains recently, I don’t think many homes will have to go to foreclosure…I think homes will just be sold, and there will be cash left over for the seller, even in a distressed situation. So that’s a bit of a silver lining in that we don’t expect a massive sale of distressed properties.”

As we can see, it looks like we’re going to have an increase in the number of homes for sale in 2021. With fears of the pandemic starting to ease, new homes being built, and more listings coming to the market prior to foreclosure, there’s hope if you’re planning to buy this year. And if you’re thinking of selling and making a move, doing so while demand for your house is high might create an outstanding move-up option for you.

Bottom Line

Housing demand is high and supply is low, so if you’re thinking of moving, it’s a great time to do so. There are likely many buyers who are looking for a home just like yours, and there are options coming for you to find a new house too. Let’s connect today to see how you can benefit from the opportunities available in our local market.

The housing market has been scorching hot over the last twelve months. Buyers and their high demand have far outnumbered sellers and a short supply of houses. According to the latest Existing Home Sales Report from the National Association of Realtors (NAR), sales are up 23.7% from the same time last year while the inventory of homes available for sale is down 25.7%. There are 360,000 fewer single-family homes for sale today than there were at this time last year. This increase in demand coupled with such limited supply is leading to more bidding wars throughout the country.

Rose Quint, Assistant Vice President for Survey Research with the National Association of Home Builders (NAHB), recently reported:

“The number one reason long-time searchers haven’t made a home purchase is not because of their inability to find an affordably-priced home, but because they continue to get outbid by other offers.”

A survey in the NAHB report showed that 40% of buyers have been outbid for a home they wanted to purchase. This is more than twice the percentage in 2019, which was 19%.

What does this mean for sellers today?

It means sellers have tremendous leverage when negotiating with buyers.

In negotiations, leverage is the power that one side may have to influence the other side while moving closer to their negotiating position. A party’s leverage is based on its ability to award benefits or eliminate costs on the other side.

In today’s market, a buyer wants three things:

To buy a home

To buy now before prices continue to appreciate

To buy now and take advantage of historically low mortgage rates while they last

These three buyer needs give the homeowner tremendous leverage when selling their house. Most realize this leverage enables the seller to sell at a good price. However, there may be another need the seller has that can be satisfied by using this leverage.

Here’s an example:

Odeta Kushi, Deputy Chief Economist at First American, recently identified a situation in which many sellers are finding themselves today:

“As mortgage rates are expected to remain near 3%, millennials continue to form households and more existing homeowners tap their equity for the purchase of a better home…Many homeowners may want to upgrade, but do not for fear that they will be unable to find a home to buy.”

She then offers a possible solution:

“While the fear of not being able to find something to buy will not disappear in a limited supply environment, new housing supply can incentivize existing homeowners to move.”

There’s no doubt many sellers would love to build a new home to perfectly fit their changing wants and needs. However, most builders require that they sell their house first. If the seller sells their home, where would they live while their new home is being constructed?

Going back to the concept of leverage:

As mentioned, buyers have compelling reasons to purchase a home now, and many homeowners have challenges to address if they want to sell. Perhaps they can make a deal to satisfy each party’s needs. But how?

The seller may decide to sell their home to the buyer at today’s price, which will enable the purchaser to take advantage of current mortgage rates. In return, the buyer might lease the house back to the seller for a pre-determined length of time while the seller’s new home is being built. A true win-win negotiation.

Not every buyer will agree to such a deal – but you only need one.

That’s just one example of how a seller might be able to overcome a challenge because of the leverage they have in today’s market. Maybe you feel a need to make certain repairs before selling. Perhaps you need time to get permits or approvals for certain upgrades you made to the house. Whatever the challenge, you may be able to work it out.

Bottom Line

If you’re considering selling your house now but worry a huge obstacle stands in your way, let’s connect. Maybe with the leverage you currently have, you can negotiate a deal that will allow you to make the move of your dreams.

In today’s housing market, it seems harder than ever to find a home to buy. Before the health crisis hit us a year ago, there was already a shortage of homes for sale. When many homeowners delayed their plans to sell at the same time that more buyers aimed to take advantage of record-low mortgage rates and purchase a home, housing inventory dropped even further. Experts consider this to be the biggest challenge facing an otherwise hot market while buyers continue to compete for homes. As Danielle Hale, Chief Economist at realtor.com, explains:

“With buyers active in the market and seller participation lagging, homes are selling quickly andthe total number available for sale at any point in time continues to drop lower. In January as a whole, the number of for sale homes dropped below 600,000.”

Every month, realtor.com releases new data showing the year-over-year change in inventory of existing homes for sale. As you can see in the map below, nationwide, inventory is 42.6% lower than it was at this time last year:

Does this mean houses aren’t being put on the market for sale?

Not exactly. While there are fewer existing homes being listed right now, many homes are simply selling faster than they’re being counted as current inventory. The market is that competitive! It’s like when everyone was trying to find toilet paper to buy last spring and it was flying off the shelves faster than it could be stocked in the stores. That’s what’s happening in the housing market: homes are being listed for sale, but not at a rate that can keep up with heavy demand from competitive buyers.

In the same realtor.com report, Hale explains:

“Time on the market was 10 days faster than last year meaning that buyers still have to make decisions quickly in order to be successful. Today’s buyers have many tools to help them do that, including the ability to be notified as soon as homes meeting their search criteria hit the market. By tailoring search and notifications to the homes that are a solid match, buyers can act quickly and compete successfully in this faster-paced housing market.”

The Good News for Homeowners

The health crisis has been a major reason why potential sellers have held off this long, but as vaccines become more widely available, homeowners will start making their moves. Ali Wolf, Chief Economist at Zonda, confirms:

“Some people will feel comfortable listing their home during the first half of 2021. Others will want to wait until the vaccines are widely distributed.”

With more homeowners getting ready to sell later this year, putting your house on the market sooner rather than later is the best way to make sure your listing shines brighter than the rest.

When you’re ready to sell your house, you’ll likely want it to sell as quickly as possible, for the best price, and with little to no hassle. If you’re looking for these selling conditions, you’ll find them in today’s market. When demand is high and inventory is low, sellers have the ability to create optimal terms and timelines for the sale, making now an exceptional time to move.

Bottom Line

Today’s housing market is a big win for sellers, but these conditions won’t last forever. If you’re in a position to sell your house now, you may not want to wait for your neighbors to do the same. Let’s connect to discuss how to sell your house safely so you’re able to benefit from today’s high demand and low inventory.

There have been a lot of headlines reporting on how homeowner equity (the difference between the current market value of your home and the amount you owe on your mortgage) has dramatically increased over the past few years. CoreLogic indicated that equity increased for the average homeowner by $17,000 in the last year alone. ATTOM Data Solutions, in their latest U.S. Home Equity Report, revealed that 30.2% of the 59 million mortgaged homes in the United States have at least 50% equity. That doesn’t even include the 38% of homes that are owned free and clear, meaning they don’t have a mortgage at all.

How can equity help a household?

Having equity in your home can dramatically impact your life. Equity is like a savings account you can tap into when you need cash. Like any other savings, you should be sensible in how you use it, though. Here are three good reasons to consider using your equity.

1. You’re experiencing financial hardship (job loss, medical expenses, etc.)

Equity gives you options during difficult financial times. With equity, you could refinance your house to get cash which may ease the burden. It also puts you in a better position to talk to the bank about restructuring your home loan until you can get back on your feet.

Today, there are 2.7 million Americans who are currently in a forbearance program because of the pandemic. Ninety percent of those in the program have at least 10% equity. That puts them in a better position to get a loan modification instead of facing foreclosure because many banks will see the equity as a form of collateral in a new deal. If you’re in this position, even if you can’t get a modification, the equity allows you the option to sell your house and walk away with your equity instead of losing the house and your investment in it.

2. You need money to start a new business

We’ve all heard the stories about how many great American companies started in the founder’s garage (i.e., Disney, Hewlett Packard, Apple, Yankee Candle, Keeping Current Matters). What we might not realize, however, is the garage (along with the rest of the home) supplied the start-up money for many of these companies in the form of a refinance.

If you’re passionate about an idea you have for a new product or service, the equity in your home may enable you to make that dream a reality.

3. You want to invest in a loved one’s future

It’s been a long-standing tradition in this country for many households to help pay college expenses for their children. Some have tapped into the equity in their homes to do that.

Additionally, George Ratiu, Senior Economist for realtor.com, notes:

“52% of Americans who bought their first home in 2020 said they got help with their down payment from friends or family. The number one lender? Their parents.”

It’s safe to assume a percentage of that down payment money likely came from home equity.

Bottom Line

Savings in any form is a good thing. The forced savings you can earn from making a mortgage payment enables you to build wealth through home equity. That equity can come in handy in both good and more challenging times.

In today’s housing market, all eyes are on millennials. Not only are millennials the largest generation, but they’re also currently between 25 and 40 years old. These are often considered prime homebuying years when many people begin to form their own households and invest in real estate. If you’re like many millennials who are spending much more time at home these days, you may have a growing need for more space or upgraded features, making moving more desirable than ever.

For those millennials who already own a home, there’s a great opportunity to move up in 2021. Danielle Hale, Chief Economist at realtor.com, explains:

“Older millennials will be trade-up buyers with many having owned their first homes long enough to see substantial equity gains.”

Even if you bought a home sometime in the last few years, you may have more equity than you realize, and that’s a big factor to consider when you’re thinking about moving. According to the Homeowner Equity Insights Report from CoreLogic:

“In the third quarter of 2020, the average homeowner gained approximately $17,000 in equity during the past year. This marks the largest average equity gain since the first quarter of 2014.”

Growing equity can be the driver you’re looking for to fund your next move, especially if what you need in a home is changing right now. As equity builds over time, it can be put toward the down payment on your next home.

In addition to equity gains, today’s housing market affordability is powered by record-low mortgage rates, so moving at a time when you can get more for your money may be more realistic than you think.

Bottom Line

If you’re a millennial thinking about moving this year, you’re not alone. Let’s connect to shed light on the equity you have in your current home and the opportunities it can create.

My name is John Bendele and these are words to live by.

“What is the biggest challenge you are facing in life right now and how can I help?”

I believe when you are able to help others in their struggles, it will always bring a since of joy and accomplishment that is like no other. I enjoy bringing opportunities to people in real estate and in life. To be a lifting hand and a beacon of knowledge. It brings me great joy to guide and support others when making exciting and difficult choices. I have been a licensed realtor for over 7 years in Minnesota. Coming from a construction background, I will provide a wealth of knowledge about homes. Knowing homes allows me to a better negotiator with facts and details some may not. I enjoy working with sellers, investors and buyers.

I grew up in Southwest Texas and moved to Minnesota in 2015. I have lived in the White Bear Lake area until making a move over the lake to Willernie, MN where I now reside. I love spending quality time with my teenage boys who nicknamed me “JoJo”. My favorite things to do are being outdoors on or in the water, BBQing (TX style) and going on any adventure.

I want to bring knowledge, growth, excitement and wealth to the clients I encounter through being a realtor. I look forward to assisting you in your amazing journey in real estate.

Thank you,

John A Bendele

Meet Brittany

Brittany is a mama of three kiddos, a wife of a firefighter and added more love to her home with three dogs and two cats. Outside of the fun she has as an agent and her roles at home she enjoys doing any DIY projects she can get her hands on!

Brittany fell in love with the Real Estate gig in 2019. She grew up in Apple Valley, and now owns her childhood home. I guess you could say she is a south metro pro!

You!

Hey! If you’re looking for your next role as an agent let us know! This could be you!

Meet Shea Amundson

Hey, I’m Shea and I love helping people find a beautiful home that sets their soul on fire!

Meet Katie

Katie comes from the busy world of entertainment and being a Traveling Operations Manager. She transitioned to Real Estate back in 2018 and has been hooked ever since! Katie thrives on training, developing new systems, and helping agents grow! Katie joins Voila with the determination to help every agent and client make their dream a reality whether it be building their business or finding that dream home!

When Katie isn’t working, she is a full-time student at Metropolitan University. She enjoys cooking foods from all over the world, traveling, and has a habit of getting a new tattoo wherever she goes. She is huge into animal conservation and spending time with her dog Sawyer who often joins her on travels!

Meet Sarah Beth Lindstrom

Sarah wants to live in a world filled with innovative businesses daring enough to break the mold…monthly auto-shipments of Laffy Taffy’s, and lots and lots of laughter!!!

Having been in the real estate industry since 2005, her go to role has always been supporting her teams in any way that she can! She has gone from Listing and Transaction Management, to Team Manager, and now Director of Support! She is an ‘introverted extrovert’ that finds the, ‘behind the scenes’ with a hint of showing homes – to be a perfect blend.

When she’s not supporting her Voila Family, she is out getting one more rep in at the gym, finding new healthy recipes to attempt (and then trick her teenager into eating somehow), and enjoying quick road trips to…well, anywhere! She also plays on a competitive volleyball team in the winter, sand volleyball in the summer and softball in the spring and fall.

“Two things define you. The patience you have when you have nothing and the attitude when you have everything.”

Meet Jessi Andersen

In June of 2020 Jessi joined team of Voila…and…it’s that easy!

Ha! No really, it did all begin in June. New to this side of Real Estate, Jessi joined in hopes to take her chatty, outgoing self and bring some good of it! Her natural tendencies of networking and love of growth and goals, have been set in direction – expanding Voila!

Where is Jess when she isn’t nurturing the growth of Voila? Adventuring with her family outside in nature. Or perhaps baking up a new recipe while dancing the day away – and of course cheering for her little athletes at home, as well as the MN Vikings/Twins!

“In the end it is not the years in your life that count. It’s the life in your years” ~ Abe Lincoln

Meet Wyatt Lemon

Wyatt is a Real Estate Extraordinaire, and a Loving Husband, and a Lover of Life and a PAW-rent to 3 awesome dogs. Huge believer in the idea that life is what you make of it, so with that being said I guess you could say the glass is half full! Things I enjoy outside of work are Yoga, being a big time Foodie, and spending time with my family. I grew up in Hugo MN and have been a local resident my whole life. I studied Marketing at Century College as well as St. Cloud State University. I got into Real Estate in October of 2018 and have loved every minute of it!

Meet James Andersen

James Andersen is a human being who believes that the best in others is a reflection of the energy we bring.

Magnanimous behavior is the standard not the exception.

10+ years Army Career

5+ years Married

5+ years Father of Calendar Crushers

5+ years Real Estate Career

30+ years Life Experience

Let’s learn and grow together.

Meet Joey Torkildson

You are writing your own story in life! Is what you are doing right now supposed to be in that story? I hope so!

That’s why my goal is to always sign up, get uncomfortable, inspire through doing, shoot, then aim. We don’t have enough time on this planet to stay mundane and there are too many experiences to be doing one thing for too long! It’s all about the short term experiments!

Quick background: 19+ year US Army Master Sergeant vet; 10+ year transformer of lives through ownership (AKA: Realtor) ; 2+ year CEO of an Expansion Team with Hergenrother Realty Group ; Director of Agent Training with that same organization; Self employed for 12+ years; starting in late 2019 CoFounded a new disruptive real estate brokerage, Voila; Contagiously energetic teacher who loves helping people discover they can accomplish anything; Dad of two extremely crazy and loving boys; Husband of an amazingly supportive and ultimate gardener wife.

Let’s be curious explorers together! I love connecting with people and helping them achieve their goals and I’m a firm believer in the fact that you are one introduction away from your entire life changing!

Two quotes I live by: Amazing things rarely happen in your comfort zone and only those who attempt the absurd achieve the impossible!