If you’re one of the many homeowners thinking about taking your house off the market for the holidays, hang on. You definitely don’t want to miss the great selling opportunity you have right now. Here’s why this month is the optimal time to make sure your house is available for holiday buyers.

The latest Existing Home Sales Report from The National Association of Realtors (NAR) shows the inventory of houses for sale has dropped to an astonishing all-time low. It now sits at a 2.5-month supply at the current sales pace.

Historically, a 6-month supply is necessary for a ‘normal’ or ‘neutral’ market, in which there are enough homes available for active buyers (See graph below):When the supply of houses for sale is as low as it is today, it’s much harder for buyers to find homes to purchase. This means competition among purchasers rises and more bidding wars take place, making it essential for buyers to submit very attractive offers.

As this happens, prices rise and sellers are in the best position to negotiate deals that meet their ideal terms. So, if your neighbors decide to remove their listings this season, your house may quickly rise to the top of a holiday buyer’s wish list if you stay on the market.

Today, there are many buyers who are ready, willing, and able to purchase. Record-low mortgage rates and a year filled with unique changes have prompted buyers to think differently about where they live and to take action. The supply of homes for sale is not keeping up with this high demand, making now the optimal time to sell your house.

Bottom Line

Home prices are appreciating in today’s sellers’ market. Making your home available over the next few weeks will give you the most exposure to buyers who will be actively competing against each other to purchase it.

Talk of a housing bubble is beginning to crop up as home prices have appreciated at a rapid pace this year. This is understandable since the appreciation of residential real estate is well above historic annual averages. According to the Federal Housing Finance Agency (FHFA), annual appreciation since 1991 has averaged 3.8%. Here are the latest 2020 appreciation numbers from three reliable sources:

It’s easy to jump to the conclusion that house appreciation is out of control in today’s market. However, we need to put these numbers into context first.

Inflation and the Comeback from the Housing Crash

Following the housing crash, home values depreciated dramatically from 2007-2011. Values are still recovering from that unusually long period of falling prices. We must also realize that normal inflation has had an impact.

Bill McBride, the founder of the well-respected Calculated Risk blog, recently summed it up this way:

“It has been over fourteen years since the bubble peak. In the Case-Shiller release today, the seasonally adjusted National Index, was reported as being 22.2% above the previous bubble peak. However, in real terms (adjusted for inflation), the National index is still about 2% below the bubble peak…As an example, if a house price was $200,000 in January 2000, the price would be close to $291,000 today adjusted for inflation.”

The COVID Impact on Home Prices

The pandemic caused many households to reconsider whether their current home still fulfills their lifestyle. Many homeowners now want larger yards that are both separate and private.

Their needs on the inside of the home have changed too. People now want home offices, gyms, and living rooms well-suited for video conferencing. Barbara Ballinger, a freelance writer and the author of several books on real estate, recently wrote:

“While homeowners continue to want their outdoor spaces that offer a safe retreat, that appeal has shifted into other parts of the home, coupling comfort with function. In other words, homeowners want amenities for work and leisure, and they plan to enjoy them long after the pandemic.”

At the same time, concerns about the pandemic have caused many homeowners to put their plans to sell on hold. Realtor.com just released their November Monthly Housing Market Trends Report. It explains:

“Nationally, the inventory of homes for sale decreased 39.2% over the past year in November…This amounted to 490,000 fewer homes for sale compared to November of last year.”

More people buying and fewer people selling has caused home prices to escalate. However, with a vaccine on the horizon, more homeowners will be putting their houses on the market. This will better balance supply with demand and slow down the rapid appreciation.

That’s why major organizations in the housing industry are calling for much more moderate home appreciation next year. Here are the most recent forecasts for 2021:

Finally, let’s put to rest some of the concerns that today’s scenario is anything like what led up to the last housing crash. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains why this is nothing like 2006:

“Such a frenzy of activity, reminiscent of 2006, raises questions about a bubble and the potential for a painful crash. The answer: There’s no comparison. Back in 2006, dubious adjustable-rate mortgages taxed many buyers’ budgets. Some loans didn’t even require income documentation. Today, buyers are taking out 30-year fixed-rate mortgages. Fourteen years ago, there were 3.8 million homes listed for sale, and home builders were putting up about 2 million new units. Now, inventory is only about 1.5 million homes, and home builders are underproducing relative to historical averages.”

Bottom Line

Most aspects of life have been anything but normal in 2020. That includes buying and selling real estate. High demand coupled with restricted supply has caused home prices to appreciate above historic levels. With the end of the health crisis in sight, we will see price appreciation return to more normal levels next year.

Last Friday, the Bureau of Labor Statistics released the November Jobs Report. It revealed that, though headed in the right direction, the nation’s job recovery has slowed. The consensus reaction is best exemplified by a quote from GlassdoorSenior Economist, Daniel Zhao:

“We saw positive job gains, but I think the sentiment is largely negative because we know that we’re heading into a dark winter.”

There’s no doubt that millions of households have been – and continue to be -devastated by the economic downturn caused by the pandemic.

We should, however, put the current situation into perspective. Where we currently stand is much better than where most experts thought we would be at this time. Jed Kolko, Chief Economist of Indeed, explained in his State of the Labor Market that, though the situation is not good, we’re doing better than original expectations:

“Though the labor market rebound is incomplete, it has nevertheless surpassed expectations. In May, after payrolls plunged and unemployment spiked, the Wall Street Journal panel of economic forecasters projected unemployment would be over 11% in December 2020 and not fall below 7% until the first half of 2022 — a milestone already passed in October.”

With the announcement that vaccines should be available soon, we’re not far from the most damaged segments of the economy gaining momentum again.

Jeff Sparshott of the Wall Street Journal recently wrote:

“Even with signs of a recent slowdown, the labor-market recovery since this spring has been stronger than most economists expected. Many now project widespread vaccine distribution will eventually help lift the economy further as businesses are allowed to reopen and consumers feel more comfortable traveling, going to the movies.”

Bottom Line

Though millions of Americans are still out of work, the situation was forecasted to be even direr than it is today. Once a vaccine becomes available, the economy should complete its comeback, and so should the labor market.

Selling a home during the winter can be a challenge with freezing temperatures and snow working against you. On the flip side, there can be benefits to selling in the winter that can work in your favor. Buyers may be more motivated because of the inclement weather and less competition from other sellers. There are a few things you can do to make your home more attractive to potential buyers. Here are three tips for selling your home easier during the winter.

Keep Out the Cold

Winter weather can expose major flaws like poor insulation and furnace problems. Before showing your home, make sure you have the HVAC system inspected and make any necessary repairs. Check to make sure there are no drafts from windows or doors. Warm up rooms by adding rugs on hardwood floors.

Emphasize the Season to Sell Your Home

The winter holidays can be used to help sell your home faster. Emphasize the season by incorporating holiday fun, and decor. Build a snowman outdoors and plant seasonal foliage. Add cozy elements indoors like cable knit pillows and plush throw blankets. Use winter scents and aromas to make your home more inviting to buyers. During showings, provide a list of local family fun activities people can enjoy during the winter.

Address Winter Safety Hazards

Before trying to sell your home, make sure to address any winter safety hazards. Shovel and salt the driveway and sidewalks. Slippery or blocked walkways can cause injuries to potential buyers and turn them away from purchasing your home.

Sell Your Home This Winter

By using the winter season wisely, you can sell your home faster and boost your property value. If you want to make selling your house as simple as possible, reach out to one of our Voila real estate savvy fanatics. We’ll help you get the best offers for your home. Schedule a consultation today!

This year, the opportunity to work remotely has increased the demand for vacation homes. Gay Cororaton, Senior Economist and Director of Housing and Commercial Research at the National Association of Realtors (NAR), notes:

“Working from home is a positive factor in demand for vacation homes.”

Buyers are taking advantage of the fact that working from home might be someplace other than their primary residence – at the beach, in the mountains, or somewhere in between. NAR explains:

“Sales in vacation-home counties increased 48% on average year over year in the third quarter; overall, 81% of vacation-home counties saw a year-over-year sales increase.”

Is it Time to Sell Your Vacation Home?

If you’ve been thinking about selling your vacation home, putting it on the market now while demand is high might be your best move. Here are two reasons why.

1. Vacation Homes Are Selling Quickly

These homes are not staying in the market for very long. NAR also notes:

“In September, 68% of vacation homes sold in less than a month. Historically, about 30% sell that quickly…It’s a pretty amazing uptick compared to past years.”

2. Home Prices Are Rising

With an increase in demand, prices go up. NAR continues:

“In the third quarter, prices in vacation-home counties rose by about 32% year over year. Seventy-nine percent of these counties experienced year-over-year price gains. NAR defines a vacation-home county as one in which seasonal housing accounts for at least 20% of stock.”

If your vacation home is sitting idle, maybe not attracting as many renters as you usually see, or if you simply want to sell it so you can trade up or take it off your worry list, now may be the time. Demand is high, so you’re in the ideal spot to get a stronger return on your investment today.

Bottom Line

Demand is on the rise, so let’s discuss your next steps when it comes to selling your vacation home.

In a year when we’re learning to do so much remotely, homebuying is no exception. From going to work to attending school, grocery shopping, and even seeing our doctors online, digital practices have changed the way we live.

This year, rather than delaying their home purchases, buyers – alongside their trusted real estate professionals – turned to the Internet to do more than just a typical home search. In some cases, they bought homes without even stepping foot inside. Jessica Lautz, Vice President of Demographics and Behavioral Insights at the National Association of Realtors (NAR), says:

“People really didn’t buy houses sight-unseen, traditionally. It’s still not a huge number, but it has gone up, and we have definitely seen that trend accelerate.”

According to NAR, throughout the coronavirus pandemic, one in every 20 homebuyers purchased a house sight-unseen.

How Your Real Estate Agent Will Pave the Way

Today, real estate professionals are using digital practices to help homebuyers and sellers walk through many steps in the process virtually. While following the regulations set forth by the CDC and all local guidelines, this year, agents quickly empowered buyers and sellers with virtual tours, 3D floor plans, high-quality photos, videos, online open houses, and more. For those who had homebuying and selling needs in 2020, trusted advisors made it possible in many markets.

Here’s a graph showing some of the digital options buyers found most helpful in their searches this year, as noted by NAR in the 2020 Profile of Home Buyers and Sellers:The report also mentions that buyers this year generally searched for eight weeks. Throughout that search, they viewed a median of 9 homes, but not all of them were seen in-person. Yahoo Finance notes:

“Buyers viewed five homes online and four homes in-person during the pandemic, compared to nine homes in-person in 2019, according to NAR.This was the first year NAR asked buyers to specify the number of homes toured virtually.”

In true 2020 fashion, virtual practices helped buyers safely narrow down their top choices, so they didn’t have to unnecessarily walk into more homes than they needed to see throughout the process. Here’s the breakdown by region:At a time when health and safety are top priorities, current technology is making it possible for buyers and sellers to move their real estate plans forward at their own comfort levels, even through a worldwide pandemic. For many, this means buyers no longer have to physically tour every home they want to see, and sellers don’t need to open their doors over and over again throughout the process. Safety can come first, and trusted real estate professionals are here to help.

Bottom Line

If you’re ready to make a move, you may not have to press pause on your plans this season. Let’s connect to determine the safe and effective options to buy or sell a home in our area or wherever you’re looking to move.

Housing inventory is at an all-time low. Realtor.com just reported that there are 39% fewer homes for sale today than there were last year. At the same time, buyer demand remains strong. In a recent newsletter, research analyst Ivy Zelman explained:

“Although the headwind of severe supply constraints in most markets has contributed to slight moderation in seasonally-adjusted and year-over-year new pending contract growth for two consecutive months (albeit still growing strongly), the underlying strength of buyer demand, particularly for this time of year, remains apparent.”

Whenever there’s a shortage in the supply of an item that’s in high demand, the price of that item increases. That’s exactly what’s happening in the real estate market right now. As a result, home values are surging.

This is great news if you’re planning to sell your house. On the other hand, as either a first-time or repeat buyer, this may instead seem like troubling news. Purchasers, however, should realize that the price of a house is not as important as the monthly cost. Here’s how it breaks down.

There are several factors that influence the cost of a home. Two of the major ones are:

The price of the home

The mortgage rate at which a buyer can borrow the funds necessary to purchase the home

How do these factors impact affordability?

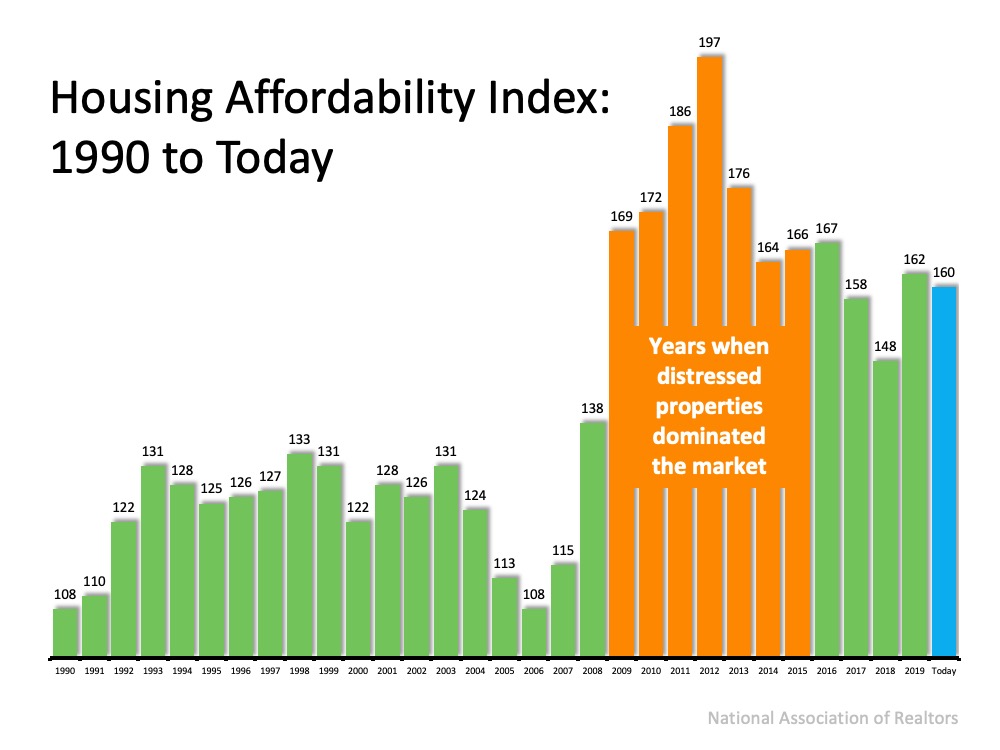

The National Association of Realtors (NAR) produces a Housing Affordability Index which takes these factors into account and determines an overall affordability score for housing. According to NAR, the index:

“…measures whether or not a typical family earns enough income to qualify for a mortgage loan on a typical home at the national and regional levels based on the most recent price and income data.”

Their methodology states:

“To interpret the indices, a value of 100 means that a family with the median income has exactly enough income to qualify for a mortgage on a median-priced home. An index above 100 signifies that family earning the median income has more than enough income to qualify for a mortgage loan on a median-priced home, assuming a 20 percent down payment.”

So, the higher the index, the more affordable it is to purchase a home. Here’s a graph of the index going back to 1990:The blue bar represents today’s affordability. We can see that homes are more affordable now than they were from:

1990 to 2008

2017 to 2018

Buying a home today is just a little less affordable than it was last year, but still very affordable compared to historical housing market trends.

Note: During the housing crash from 2009 to 2015, distressed properties (foreclosures and short sales) dominated the market. Those properties were sold at large discounts not seen before in the housing market.

Why are homes still affordable today?

The number one factor impacting today’s homebuying affordability is record-low mortgage rates. There’s no doubt that prices are on the rise. However, mortgage rates have fallen dramatically. Last week, Freddie Mac announced that the average interest rate for a 30-year fixed-rate mortgage was 2.72%. Last year at this time, the average rate was 3.68%.

If you’re considering purchasing your first home or moving up to the one you’ve always hoped for, it’s important to understand how affordability plays into the overall cost of your home. With that in mind, buying while mortgage rates are as low as they are now may save you quite a bit of money over the life of your home loan.

Bottom Line

At this point, home purchase affordability is still in a historically good place. However, we need to watch price increases going forward. As Mark Fleming, Chief Economist at First American, noted in a recent post:

“Faster nominal house price appreciation can erode, or even eliminate, the boost in affordability from lower mortgage rates, especially if household income growth doesn’t keep up.”

You listed your home for sale, and the transaction did not go as you planned. The buyer may have been unable to secure a mortgage or had to back out for personal reasons. If your home sits on the market too long, potential buyers may wonder why it has not sold yet, and you could lose some property value. Here are three tips for relisting a home after a buyer backs out to get it sold fast.

Fix Glaring Issues

One main issue that can cause a buyer to back out is glaring issues discovered during a home inspection. Before you relist your home, tackle any home repairs listed on the inspection checklist. This step will help future buyers from wanting to back out and can sell your home faster.

Consider Your Listing Price

When putting your home on the market, you want to get the best price you can. However, you may want to consider lowering your home’s price if you have experienced a buyer backing out. When you relist your home, the new pricing can help it appear more competitive on the market. Take into consideration why the buyer backed out before making any tweaks to your pricing.

Get the Timing Right for Relisting Your Home

There are specific periods throughout the year where home sales can be sluggish. If you had a buyer or two back out during winter, try relisting your home in the spring. The right timing can make all the difference.

Relist Your Home Today

Losing a buyer does not have to be a heartbreaking experience. Bounce back quickly by relisting your home right away. Our team of professionals at Voila will help you get your home sold quickly with no fuss. Take back control by contacting us today to relist your home and get it sold!

Around this time each year, many homeowners decide to wait until after the holidays to sell their houses. Similarly, others who already have their homes on the market remove their listings until the spring. Let’s unpack the top reasons why selling your house now, or keeping it on the market this season, is the best choice you can make. This year, buyers want to purchase homes for the holidays, and your house might be the perfect match.

Here are seven great reasons not to wait to sell your house this holiday season:

1. Buyers are active now. Mortgage rates are historically low, providing motivation for those who are ready to get more for their money over the life of their home loan.

2. Purchasers who look for homes during the holidays are serious ones, and they’re ready to buy.

3. You can restrict the showings in your house to days and times that are most convenient for you, or even select virtual options. You’ll remain in control, especially in today’s sellers’ market.

4. Homes decorated for the holidays appeal to many buyers.

5. Today, there’s minimal competition for you as a seller. There just aren’t enough houses on the market to satisfy buyer demand, meaning sellers are in the driver’s seat. Over the past year, inventory has declined to record lows, making it the opportune time to sell your house (See graph below): 6. The desire to own a home doesn’t stop during the holidays. Buyers who have been searching throughout the fall and have been running into more and more bidding wars are still on the lookout. Your home may be the answer.

7. This season is the sweet spot for sellers, and the number of listings will increase after the holidays. In many parts of the country, more new construction will also be available for sale in 2021, which will lessen the demand for your house next year.

Bottom Line

More than ever, this may be the year it makes the most sense to list your house during the holiday season. Let’s connect today to determine if selling now is your best move.

There seems to be some concern that the 2020 economic downturn will lead to another foreclosure crisis like the one we experienced after the housing crash a little over a decade ago. However, there’s one major difference this time: a robust forbearance program.

During the housing crash of 2006-2008, many felt homeowners should be forced to pay their mortgages despite the economic hardships they were experiencing. There was no empathy for the challenges those households were facing. In a 2009 Wall Street Journal article titled Is Walking Away From Your Mortgage Immoral?, John Courson, Chief Executive of the Mortgage Bankers Association, was asked to comment on those not paying their mortgage. He famously said:

“What about the message they will send to their family and their kids?”

Courson suggested that people unable to pay their mortgage were bad parents.

What resulted from that lack of empathy? Foreclosures mounted.

This time is different. There was an immediate understanding that homeowners were faced with a challenge not of their own making. The government quickly jumped in with a mortgage forbearance program that relieved the financial burden placed on many households. The program allowed many borrowers to suspend their monthly mortgage payments until their economic condition improved. It was the right thing to do.

What happens when forbearance programs expire?

Some analysts are concerned many homeowners will not be able to make up the back payments once their forbearance plans expire. They’re concerned the situation will lead to an onslaught of foreclosures.

The banks and the government learned from the challenges the country experienced during the housing crash. They don’t want a surge of foreclosures again. For that reason, they’ve put in place alternative ways homeowners can pay back the money owed over an extended period of time.

Another major difference is that, unlike 2006-2008, today’s homeowners are sitting on a record amount of equity. That equity will enable them to sell their houses and walk away with cash instead of going through foreclosure.

Bottom Line

The differences mentioned above will be the reason we’ll avert a surge of foreclosures. As Ivy Zelman, a highly respected thought leader for housing and CEO of Zelman & Associates, said:

“The likelihood of us having a foreclosure crisis again is about zero percent.”

My name is John Bendele and these are words to live by.

“What is the biggest challenge you are facing in life right now and how can I help?”

I believe when you are able to help others in their struggles, it will always bring a since of joy and accomplishment that is like no other. I enjoy bringing opportunities to people in real estate and in life. To be a lifting hand and a beacon of knowledge. It brings me great joy to guide and support others when making exciting and difficult choices. I have been a licensed realtor for over 7 years in Minnesota. Coming from a construction background, I will provide a wealth of knowledge about homes. Knowing homes allows me to a better negotiator with facts and details some may not. I enjoy working with sellers, investors and buyers.

I grew up in Southwest Texas and moved to Minnesota in 2015. I have lived in the White Bear Lake area until making a move over the lake to Willernie, MN where I now reside. I love spending quality time with my teenage boys who nicknamed me “JoJo”. My favorite things to do are being outdoors on or in the water, BBQing (TX style) and going on any adventure.

I want to bring knowledge, growth, excitement and wealth to the clients I encounter through being a realtor. I look forward to assisting you in your amazing journey in real estate.

Thank you,

John A Bendele

Meet Brittany

Brittany is a mama of three kiddos, a wife of a firefighter and added more love to her home with three dogs and two cats. Outside of the fun she has as an agent and her roles at home she enjoys doing any DIY projects she can get her hands on!

Brittany fell in love with the Real Estate gig in 2019. She grew up in Apple Valley, and now owns her childhood home. I guess you could say she is a south metro pro!

You!

Hey! If you’re looking for your next role as an agent let us know! This could be you!

Meet Shea Amundson

Hey, I’m Shea and I love helping people find a beautiful home that sets their soul on fire!

Meet Katie

Katie comes from the busy world of entertainment and being a Traveling Operations Manager. She transitioned to Real Estate back in 2018 and has been hooked ever since! Katie thrives on training, developing new systems, and helping agents grow! Katie joins Voila with the determination to help every agent and client make their dream a reality whether it be building their business or finding that dream home!

When Katie isn’t working, she is a full-time student at Metropolitan University. She enjoys cooking foods from all over the world, traveling, and has a habit of getting a new tattoo wherever she goes. She is huge into animal conservation and spending time with her dog Sawyer who often joins her on travels!

Meet Sarah Beth Lindstrom

Sarah wants to live in a world filled with innovative businesses daring enough to break the mold…monthly auto-shipments of Laffy Taffy’s, and lots and lots of laughter!!!

Having been in the real estate industry since 2005, her go to role has always been supporting her teams in any way that she can! She has gone from Listing and Transaction Management, to Team Manager, and now Director of Support! She is an ‘introverted extrovert’ that finds the, ‘behind the scenes’ with a hint of showing homes – to be a perfect blend.

When she’s not supporting her Voila Family, she is out getting one more rep in at the gym, finding new healthy recipes to attempt (and then trick her teenager into eating somehow), and enjoying quick road trips to…well, anywhere! She also plays on a competitive volleyball team in the winter, sand volleyball in the summer and softball in the spring and fall.

“Two things define you. The patience you have when you have nothing and the attitude when you have everything.”

Meet Jessi Andersen

In June of 2020 Jessi joined team of Voila…and…it’s that easy!

Ha! No really, it did all begin in June. New to this side of Real Estate, Jessi joined in hopes to take her chatty, outgoing self and bring some good of it! Her natural tendencies of networking and love of growth and goals, have been set in direction – expanding Voila!

Where is Jess when she isn’t nurturing the growth of Voila? Adventuring with her family outside in nature. Or perhaps baking up a new recipe while dancing the day away – and of course cheering for her little athletes at home, as well as the MN Vikings/Twins!

“In the end it is not the years in your life that count. It’s the life in your years” ~ Abe Lincoln

Meet Wyatt Lemon

Wyatt is a Real Estate Extraordinaire, and a Loving Husband, and a Lover of Life and a PAW-rent to 3 awesome dogs. Huge believer in the idea that life is what you make of it, so with that being said I guess you could say the glass is half full! Things I enjoy outside of work are Yoga, being a big time Foodie, and spending time with my family. I grew up in Hugo MN and have been a local resident my whole life. I studied Marketing at Century College as well as St. Cloud State University. I got into Real Estate in October of 2018 and have loved every minute of it!

Meet James Andersen

James Andersen is a human being who believes that the best in others is a reflection of the energy we bring.

Magnanimous behavior is the standard not the exception.

10+ years Army Career

5+ years Married

5+ years Father of Calendar Crushers

5+ years Real Estate Career

30+ years Life Experience

Let’s learn and grow together.

Meet Joey Torkildson

You are writing your own story in life! Is what you are doing right now supposed to be in that story? I hope so!

That’s why my goal is to always sign up, get uncomfortable, inspire through doing, shoot, then aim. We don’t have enough time on this planet to stay mundane and there are too many experiences to be doing one thing for too long! It’s all about the short term experiments!

Quick background: 19+ year US Army Master Sergeant vet; 10+ year transformer of lives through ownership (AKA: Realtor) ; 2+ year CEO of an Expansion Team with Hergenrother Realty Group ; Director of Agent Training with that same organization; Self employed for 12+ years; starting in late 2019 CoFounded a new disruptive real estate brokerage, Voila; Contagiously energetic teacher who loves helping people discover they can accomplish anything; Dad of two extremely crazy and loving boys; Husband of an amazingly supportive and ultimate gardener wife.

Let’s be curious explorers together! I love connecting with people and helping them achieve their goals and I’m a firm believer in the fact that you are one introduction away from your entire life changing!

Two quotes I live by: Amazing things rarely happen in your comfort zone and only those who attempt the absurd achieve the impossible!

When the supply of houses for sale is as low as it is today, it’s much harder for buyers to find homes to purchase. This means competition among purchasers rises and more bidding wars take place, making it essential for buyers to submit very attractive offers.

When the supply of houses for sale is as low as it is today, it’s much harder for buyers to find homes to purchase. This means competition among purchasers rises and more bidding wars take place, making it essential for buyers to submit very attractive offers.